如果你也在 怎样代写金融中的随机方法Stochastic Methods in Finance这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

随机建模是金融模型的一种形式,用于帮助做出投资决策。这种类型的模型使用随机变量预测不同条件下各种结果的概率。随着现代经济学、金融学实证研究的发展,金融中的随机方法Stochastic Methods in Finance作为一种数学工具具有越来越重要的应用价值。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融中的随机方法Stochastic Methods in Finance方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融中的随机方法Stochastic Methods in Finance方面经验极为丰富,各种代写金融中的随机方法Stochastic Methods in Finance相关的作业也就用不着说。

我们提供的金融中的随机方法Stochastic Methods in Finance及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等楖率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|A Simulated Example – Equity Versus Cash

In our experiment based on a similar example in Bicksler and Thorp (1973), there are two assets: US equities and US T-bills. 1 According to Siegel (2002), during $1926-2001$ US equities returned $10.2 \%$ with a yearly standard deviation of $20.3 \%$, and the mean return was $3.9 \%$ for short-term government T-bills with zero standard deviation. We assume the choice is between these two assets in each period. The Kelly strategy is to invest a proportion of wealth $x=1.5288$ in equities and sell short the T-bill at $1-x=-0.5228$ of current wealth. With the short selling and levered strategies, there is a chance of substantial losses. For the simulations, the proportion $\lambda$ of wealth invested in equities ${ }^{2}$ and the corresponding Kelly fraction $f$ are

Bicksler and Thorp used 10 and 20 yearly decision periods, and 50 simulated scenarios. MacLean et al. used 40 yearly decision periods, with 3000 scenarios.

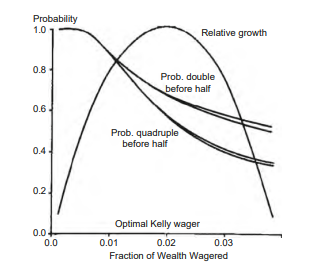

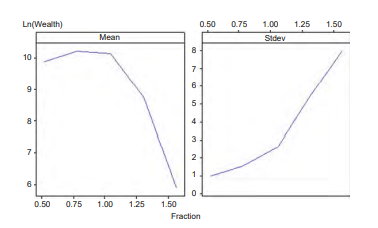

The results from the simulations appear in Table $1.3$ and Figs. 1.7, 1.8 and 1.9. The striking aspects of the statistics in Table $1.3$ are the sizable gains and losses. In his lectures, Ziemba always says when in doubt bet less – that is certainly borne out in these simulations. For the most aggressive strategy ( $1.57 \mathrm{k}$ ), it is possible to lose 10,000 times the initial wealth. This assumes that the shortselling is permissible through the decision period at the horizon $T=40$.

The highest and lowest final wealth trajectories are presented in Fig. 1.7. In the worst case, the trajectory is terminated to indicate the timing of vanishing wealth. There is quick bankruptcy for the aggressive overbet strategies.

The substantial downside is further illustrated in the distribution of final wealth plot in Fig. 1.8. The normal probability plots are almost linear on the upside.

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Final Comments

The Kelly optimal capital growth investment strategy is an attractive approach to wealth creation. In addition to maximizing the asymptotic rate of long-term growth of capital, it avoids bankruptcy and overwhelms any essentially different investment strategy in the long run. See MacLean, Thorp, and Ziemba (2010a) for a discussion of the good and bad properties of these strategies. However, automatic use of the Kelly strategy in any investment situation is risky and can be very dangerous. It requires some adaptation to the investment environment: rates of return, volatilities, correlation of alternative assets, estimation error, risk aversion preferences, and planning horizon are all important aspects of the investment process. Chopra and Ziemba (1993) show that in typical investment modeling, errors in the means average about 20 times in importance in objective value than errors in co-variances with errors in variances about double the co-variance errors. This is dangerous enough but they also show that the relative importance of the errors is risk aversion dependent with the errors compounding more and more for lower risk aversion investors and for the extreme log investors with essentially zero risk aversion the errors are worth about $100: 3: 1$. So log investors must estimate means well if they are to survive. This is compounded even more by the observation that when times move suddenly from normal to bad the correlations/co-variances approach 1 and it is hard to predict the transition from good times to bad. Poundstone’s (2005) book, while a very good read with lots of useful discussions, does not explain these important investment aspects and the use of Kelly strategies by advisory firms such as Morningstar and Motley Fools is flawed; see, for example, Fuller $(2006)$ and Lee $(2006)$. The experiments in Bicksler and Thorp (1973). Ziemba and Hausch (1986). and MacLean. Thorp. Zhao, and Ziemba $(2011)$ and that described here represent some of the diversity in the investment environment. By considering the Kelly and its variants we get

a concrete look at the plusses and minuses of the capital growth model. We can conclude that

- The wealth accumulated from the full Kelly strategy does not stochastically dominate fractional Kelly wealth. The downside is often much more favorable with a fraction less than $1 .$

- There is a trade-off of risk and return with the fraction invested in the Kelly portfolio. In cases of large uncertainty, from either intrinsic volatility or estimation error, security is gained by reducing the Kelly investment fraction.

- The full Kelly strategy can be highly levered. While the use of borrowing can be effective in generating large retums on investment, increased leveraging beyond the full Kelly is not warranted as it is growth-security dominated. The returns from over-levered investment are offset by a growing probability of bankruptcy.

- The Kelly strategy is not merely a long-term approach. Proper use in the short and medium run can achieve wealth goals while protecting against drawdowns. MacLean, Sanegre, Zhao, and Ziemba (2004) and MacLean, Zhao, and Ziemba (2009) discuss a strategy to reduce the Kelly fraction to stay above a prespecified wealth path with high probability and to be penalized for being below the path.

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|References

Aase, K. K. (2001). On the St. Petersburg Paradox. Scandinavian Actuarial Journal $3(1)$, 69-78. Bell, R. M. and T. M. Cover (1980). Competitive optimality of logarithmic irvestment. Math of Operations Reseanch 5, 161-166.

Bertocchi, M., S. L. Schwartz, and W. T. Zicmba (2010). Optimizing the Aging, Retirement, Pensions Dilemma. Wiley, Hoboken, NJ.

Bicksler, J. L. and E. O. Thorp (1973). The capital growth model: an empirical investigation. Sournal of Financial and Quantirative Analysis \& (2), 273-287.

Breiman, L. (1960). Investment policies for expanding businesses optimal in a long run sense. Naval Research Logistics Ouarterly 4 (4), 647-651.

Breiman, L. (1961). Optimal gambling system for favorable games. Proceedings of the 4th Berkeley Symposium on Mathematical Statistics and Probability l, 63-68.

Chopra, V. K. and W. T. Ziemba (1993). The effect of crrors in mean, variance and co-variance estimates on optimal portfolio choice. Joumal of Portfolio Management $19,6-11$.

Cover, T. M. and J. Thomas (2006). Elements of Information Theory (2nd cd.). Wiley, New York, NY.

Fuller, J. (2006). Optimize your portfolio with the Kelly formula. morningstar.com, October $6 .$ Hakansson, N. H. and W. T. Zicmba (1995). Capital growth theory. In R. A. Jarrow, V. Maksimovic, and W. T. Zicmba (Eds.), Funance, Handbooks in $O R$ \& $M S$, Pp. 65-86. North Holland, Amstcrdam.

Harville, D. A. (1973). Assigning probabilitics to the outcome of multi-cntry competitions. /ournal of the American Statistical Association 68,312-316.

Hausch, D. B., V. Lo, and W. T. Ziemba (Eds.) (1994). Efficiency of Racetrack Berting Markets. Academic, San Diego.

Hausch, D. B., V. Lo, and W. T. Ziemba (Eds.) (2008). Efficiency of Racetrack Benting Markets ( 2 cd.). World Scientific, Singapore.

Hausch, D. B. and W. T. Ziemba (1985). Transactions costs, extent of inefficiencies, entries and multiple wagcrs in a racetrack betting model. Management Sclence 31, 381-394.

Hausch, D. B., W. T. Zicmba, and M. E. Rubinstein (1981). Efficiency of the market for racetrack betting. Management Science XXYII, 1435-1452.

Kelly, Jr., J. R. (1956). A new interpretation of the information rate. Bell System Techuical .lournal 35, 917-926.

Latané, H. (1978). The geometric-mean principle revisited – a reply. Journal of Banking and Finance 2 (4), 395-398.

Lec, E. (2006). How to calculate the Kelly formula. fool.com, October 31 .

Luenberger, D. G. (1993). A preference foundation for log mean-variance criteria in portfolio choice problems. Journal of Economuc Dynamics and Control 17, 887-906.

MacLean, L. C., R. Sancgre, Y. Zhao, and W. T. Zicmba (2004). Capital growth with security. Sournal of Economic Dynamics and Control 28 (4), 937-954.

MacLean, L. C., E. O. Thorp, Y. Zhao, and W. T. Zicmba (2011). How does the Fortunes FormulaKelly capital growth model perform? Joumal of Portfolio Management 37 (4).

金融中的随机方法代写

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|A Simulated Example – Equity Versus Cash

在我们基于 Bicksler 和 Thorp (1973) 中类似示例的实验中,有两种资产:美国股票和美国国库券。1 根据 Siegel (2002),在1926−2001美股回归10.2%年标准差为20.3%,平均回报为3.9%用于标准偏差为零的短期政府国库券。我们假设每个时期都在这两种资产之间进行选择。凯利策略是投资一部分财富X=1.5288在股票和卖空国库券1−X=−0.5228目前的财富。使用卖空和杠杆策略,有可能遭受重大损失。对于模拟,比例λ的财富投资于股票2和相应的凯利分数F是

Bicksler 和 Thorp 使用了 10 和 20 年的决策周期,以及 50 个模拟场景。麦克莱恩等人。使用 40 个年度决策周期,包含 3000 个场景。

模拟结果见表1.3和无花果。1.7、1.8 和 1.9。表中统计数据的显着方面1.3是可观的收益和损失。在他的讲座中,Ziemba 总是说当有疑问时少下注——这在这些模拟中肯定得到了证实。对于最激进的策略(1.57到),有可能损失10000倍的初始财富。这假设卖空是允许在地平线上的决策期间吨=40.

最高和最低的最终财富轨迹如图 1.7 所示。在最坏的情况下,轨迹终止以指示财富消失的时间。激进的超额下注策略很快就会破产。

图 1.8 中的最终财富分布图进一步说明了重大不利因素。正态概率图向上几乎是线性的。

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Final Comments

凯利最优资本增长投资策略是一种有吸引力的财富创造方法。除了最大化资本长期增长的渐近率外,它还避免了破产,并在长期内压倒了任何本质上不同的投资策略。参见 MacLean、Thorp 和 Ziemba (2010a) 对这些策略的优劣特性的讨论。然而,在任何投资情况下自动使用凯利策略都是有风险的,而且可能非常危险。它需要对投资环境进行一些调整:回报率、波动性、另类资产的相关性、估计误差、风险规避偏好和规划期限都是投资过程的重要方面。Chopra 和 Ziemba (1993) 表明,在典型的投资模型中,均值误差在客观值中的重要性是协方差误差的平均约 20 倍,方差误差约为协方差误差的两倍。这已经足够危险了,但它们也表明,错误的相对重要性取决于风险厌恶程度,对于风险厌恶程度较低的投资者和风险厌恶程度基本为零的极端对数投资者来说,错误的价值越来越大100:3:1. 因此,日志投资者要想生存,就必须很好地估计手段。观察到当时间突然从正常变为坏时,相关性/协方差接近 1,并且很难预测从好到坏的过渡,这使情况更加复杂。Poundstone (2005) 的书虽然很好读,有很多有用的讨论,但并没有解释这些重要的投资方面,而且晨星和 Motley Fools 等咨询公司使用凯利策略是有缺陷的;参见,例如,富勒(2006)和李(2006). Bicksler 和 Thorp (1973) 中的实验。津巴和豪施 (1986)。和麦克莱恩。索普。赵和津巴(2011)这里所描述的代表了投资环境的一些多样性。通过考虑凯利及其变体,我们得到

具体看一下资本增长模型的优缺点。我们可以得出结论

- 完全凯利策略积累的财富不会随机支配部分凯利财富。不利的一面往往是更有利的一小部分1.

- 投资于凯利投资组合的部分需要权衡风险和回报。在存在较大不确定性的情况下,无论是内在波动性还是估计误差,都可以通过减少凯利投资分数来获得安全性。

- 完整的凯利策略可以高度利用。虽然使用借贷可以有效地产生大量投资回报,但没有理由增加杠杆率超过全部凯利,因为它是增长型证券主导的。过度杠杆投资的回报被越来越大的破产可能性所抵消。

- 凯利策略不仅仅是一种长期的方法。在短期和中期适当使用可以实现财富目标,同时防止回撤。MacLean、Sanegre、Zhao 和 Ziemba(2004 年)以及 MacLean、Zhao 和 Ziemba(2009 年)讨论了一种降低凯利分数以高概率保持在预定财富路径之上并因低于路径而受到惩罚的策略。

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|References

Aase, KK (2001)。关于圣彼得堡悖论。斯堪的纳维亚精算杂志3(1), 69-78。贝尔、RM 和 TM 封面(1980 年)。对数投资的竞争最优性。运维数学研究 5, 161-166。

Bertocchi, M., SL Schwartz 和 WT Zicmba (2010)。优化老龄化、退休、养老金困境。威利,霍博肯,新泽西州。

比克斯勒、JL 和 EO 索普 (1973)。资本增长模型:实证调查。财务和定量分析的 Sournal \& (2), 273-287。

Breiman, L. (1960)。从长远来看,扩大业务的投资政策是最优的。海军研究后勤 Oarterly 4 (4), 647-651。

Breiman, L. (1961)。有利游戏的最佳赌博系统。第四届伯克利数理统计和概率研讨会论文集,63-68。

Chopra、VK 和 WT Ziemba (1993)。均值、方差和协方差估计中的误差对最优投资组合选择的影响。投资组合管理杂志19,6−11.

封面,TM 和 J. Thomas(2006 年)。信息论要素(第 2 版)。威利,纽约,纽约。

富勒,J. (2006)。使用凯利公式优化您的投资组合。晨星网,十月6.Hakansson, NH 和 WT Zicmba (1995)。资本增长理论。在 RA Jarrow、V. Maksimovic 和 WT Zicmba (Eds.), Funance, Handbooks in这R\&米小号,页。65-86。北荷兰,阿姆斯特丹。

DA 哈维尔 (1973)。为多国竞争的结果分配概率。/美国统计协会杂志 68,312-316。

Hausch、DB、V. Lo 和 WT Ziemba (Eds.) (1994)。Racetrack Berting 市场的效率。学术,圣地亚哥。

Hausch、DB、V. Lo 和 WT Ziemba (Eds.) (2008)。赛马场弯曲市场的效率 (2 cd.)。世界科学,新加坡。

Hausch、DB 和 WT Ziemba (1985)。赛道投注模型中的交易成本、低效率程度、条目和多个 wagcr。管理学 31, 381-394。

Hausch、DB、WT Zicmba 和 ME 鲁宾斯坦 (1981)。赛道博彩市场的效率。管理科学 XXYII,1435-1452。

小凯利,JR (1956)。信息速率的新解释。贝尔系统技术 .lournal 35, 917-926。

拉塔内,H.(1978 年)。重新审视几何平均原理——一个答复。银行与金融杂志 2 (4), 395-398。

Lec, E. (2006)。如何计算凯利公式。傻瓜网,10 月 31 日。

Luenberger, DG (1993)。投资组合选择问题中对数均值方差标准的偏好基础。经济动力学与控制杂志 17, 887-906。

MacLean, LC, R. Sancgre, Y. Zhao 和 WT Zicmba (2004)。安全的资本增长。经济动态与控制杂志 28 (4), 937-954。

MacLean、LC、EO Thorp、Y. Zhao 和 WT Zicmba (2011)。Fortunes FormulaKelly 资本增长模型的表现如何?投资组合管理杂志 37 (4)。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。统计代写|python代写代考

随机过程代考

在概率论概念中,随机过程是随机变量的集合。 若一随机系统的样本点是随机函数,则称此函数为样本函数,这一随机系统全部样本函数的集合是一个随机过程。 实际应用中,样本函数的一般定义在时间域或者空间域。 随机过程的实例如股票和汇率的波动、语音信号、视频信号、体温的变化,随机运动如布朗运动、随机徘徊等等。

贝叶斯方法代考

贝叶斯统计概念及数据分析表示使用概率陈述回答有关未知参数的研究问题以及统计范式。后验分布包括关于参数的先验分布,和基于观测数据提供关于参数的信息似然模型。根据选择的先验分布和似然模型,后验分布可以解析或近似,例如,马尔科夫链蒙特卡罗 (MCMC) 方法之一。贝叶斯统计概念及数据分析使用后验分布来形成模型参数的各种摘要,包括点估计,如后验平均值、中位数、百分位数和称为可信区间的区间估计。此外,所有关于模型参数的统计检验都可以表示为基于估计后验分布的概率报表。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

statistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

机器学习代写

随着AI的大潮到来,Machine Learning逐渐成为一个新的学习热点。同时与传统CS相比,Machine Learning在其他领域也有着广泛的应用,因此这门学科成为不仅折磨CS专业同学的“小恶魔”,也是折磨生物、化学、统计等其他学科留学生的“大魔王”。学习Machine learning的一大绊脚石在于使用语言众多,跨学科范围广,所以学习起来尤其困难。但是不管你在学习Machine Learning时遇到任何难题,StudyGate专业导师团队都能为你轻松解决。

多元统计分析代考

基础数据: $N$ 个样本, $P$ 个变量数的单样本,组成的横列的数据表

变量定性: 分类和顺序;变量定量:数值

数学公式的角度分为: 因变量与自变量

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。