金融代写|量化风险管理代写Quantitative Risk Management代考| Market Risk

如果你也在 怎样代写量化风险管理Quantitative Risk Management这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

项目管理中的定量风险管理是将风险对项目的影响转换为数字的过程。这种数字信息经常被用来确定项目的成本和时间应急措施。

statistics-lab™ 为您的留学生涯保驾护航 在代写量化风险管理Quantitative Risk Management方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写量化风险管理Quantitative Risk Management代写方面经验极为丰富,各种代写量化风险管理Quantitative Risk Management相关的作业也就用不着说。

我们提供的量化风险管理Quantitative Risk Management及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

金融代写|量化风险管理代写Quantitative Risk Management代考|The Fundamental Review of the Trading Book

The fundamental review of the trading book or FRTB regulations (BCBS 2014) is a response to a pre-crisis framework that has been deemed inadequate and weak in many areas. This is particularly true for the definition of the boundary of the trading book. Indeed, internal model approach was not sufficient and many issues were to be dealt with for a better regulatory capital framework.

For instance, tail risk was something that the VaR approach did not capture adequately along with illiquidity. Most IMA-based approaches also allow for generous diversification effects as they are based on historic parameters which definitely do not hold in a crisis situation (correlation largely become relevant in very stressed markets).

The current standardised approach is highly inadequate as the linkage between the internal model and the standardised approach is inappropriate. Besides, the current standardised approach lacks risk sensitivity. This issue needs to be dealt with along with constraining the diversification benefits and hedging.

The FRTB addresses the boundary issue between the banking and the trading book in order to reduce regulatory arbitrage between the two books limiting the will to transfer from one book to the other and introducing reporting guidelines and regulatory oversight that should allow for a much better framework that governs the boundary between the two books.

The FRTB also aims at capturing the effect of tail risk more effectively as well as capturing liquidity effects. Tail risk is captured moving from a VaR to an expected shortfall approach for various horizon depending on asset/risk classes.

Under FRTB internal models have to be approved at the desk level. If desks are not approved, these will be moved back to the standardised approach. Trading desks will have to show that their models are compliant by showing that they have adequate $P \& L$ attribution and backtesting procedures in place. It is important to note that $P \& L$ attribution (i.e. model-based $P \& L$ by opposition to risk-based theoretical $\mathrm{P} \& \mathrm{~L}$ ) will be under scrutiny to ensure that risk models properly capture the risk associated with the models themselves. Besides, hedging and diversification benefits will be constrained and an additional charge will come to cover non-modellable risk factors.

The revised standardised approach (RSA) will be considered for banks willing to use simple approaches. This approach will also be the fallback for banks not gaining approval for there internal models. The main methodological modification is that the approach is now based on risk sensitivities across asset classes. The RSA aims at providing a consistent way to measure risks across geographic areas, giving authorities a better way to compare IMA and SA banks as the two approaches are sharing a common framework. Furthermore, a standardised default risk charge will be added along an add-on for residual risk, clearly harder to model. Therefore, following the FRTB and from a capital calculations standpoint, two possibilities are offered to banks to perform them. These are presented in the following.

金融代写|量化风险管理代写Quantitative Risk Management代考|Standardised Approach

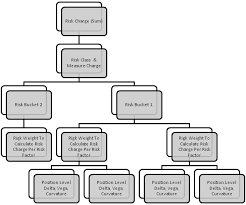

As presented in the standardised approach capital requirement (BCBS 2016a) is the simple sum of three components: the risk charges under the sensitivities-based method, the default risk charge, and the residual risk add-on.

The risk charge under the sensitivities-based method must be calculated by aggregating the following risk measures:

- Delta: A risk measure based on sensitivities of a bank’s trading book to regulatory delta risk factors. Delta sensitivities are to be used as inputs into the aggregation formula which delivers the capital requirement for the sensitivities-based method.

- Vega: A risk measure that is also based on sensitivities to regulatory vega risk factors to be used as inputs to a similar aggregation formula as for delta risks.

- Curvature: A risk measure which captures the incremental risk not captured by the delta risk of price changes in the value of an option. Curvature risk is based on two stress scenarii involving an upward shock and a downward shock to a given risk factor. The worst loss of the two scenarii is the risk position to be used as an input into the aggregation formula which delivers the capital charge.

In order to address the risk that correlations may increase or decrease in periods of financial stress, three risk charge figures must be calculated for each risk class defined under the sensitivities-based method, based on three different scenarios on the specified values for the correlation parameter $\rho_{k l}$ (i.e. correlation between risk factors within a bucket) and $\gamma_{b c}$ (i.e. correlation across buckets within a risk class). There must be no diversification benefit recognised between individual risk classes. We refer to BCBS (2016a) for more details on the parameters.

The bank must determine each delta and vega sensitivity and curvature scenario based on instrument prices or pricing models that an independent risk control unit within a bank uses to report market risks or actual profits and losses to senior management.

The default risk charge captures the jump-to -default risk in three independent capital charge computations for default risk of non-securitisations, securitisations (non-correlation trading portfolio), and securitisation correlation trading portfolio. It is calibrated based on the credit risk treatment in the banking book in order to reduce the potential discrepancy in capital requirements for similar risk exposures across the bank. Some hedging recognition is allowed within a risk weight bucket. There must be no diversification benefit recognised between different buckets.

Additionally, the Committee acknowledges that not all market risks can be captured in the standardised approach, as this might necessitate an unduly complex regime. A residual risk add-on is thus introduced to ensure sufficient coverage of market risks.

Supervisory authorities will be able to insist on a period of initial monitoring and live testing of a bank’s internal model before it is used for supervisory capital purposes. In addition to these general criteria, banks using internal models for capital purposes will be subject to the additional requirements detailed below.

金融代写|量化风险管理代写Quantitative Risk Management代考|Internal Models Approach

The use of an internal model for the purposes of regulatory capital determination will be conditional upon the explicit approval of the bank’s supervisory authority. Home and host country supervisory authorities of banks that carry out material trading activities in multiple jurisdictions intend to work cooperatively to ensure an efficient approval process.

- It is satisfied that the bank’s risk management system is conceptually sound and is implemented with integrity;

- The bank has, in the supervisory authority’s view, sufficient numbers of staff skilled in the use of sophisticated models not only in the trading area but also in the risk control, audit and, if necessary, back office areas;

- The bank’s models have, in the supervisory authority’s judgement, a proven track record of reasonable accuracy in measuring risk;

- The bank regularly conducts stress tests along the lines discussed in BCBS (2016a); and

- The positions included in the internal model for regulatory capital determination are held in approved trading desks that have passed the required tests.

From a quantitative standpoint, the document states the following: Banks will have flexibility in devising the precise nature of their models, but the following minimum standards will apply for the purpose of calculating their capital charge. Individual banks or their supervisory authorities will have discretion to apply stricter standards. “Expected shortfall” must be computed on a daily basis for the bankwide internal model for regulatory capital purposes. Expected shortfall must also be computed on a daily basis for each trading desk that a bank wishes to include within the scope for the internal model for regulatory capital purposes.

In calculating the expected shortfall, a $97.5$ th percentile, one-tailed confidence level is to be used. In calculating the expected shortfall, the liquidity horizons described in BCBS (2016a) (see Table 2.2) must be reflected by scaling an expected shortfall calculated on a base horizon. The expected shortfall for a liquidity horizon must be calculated from an expected shortfall at a base liquidity horizon of 10 days with scaling applied to this base horizon result as follows:

$$

E S=\sqrt{\left(E S_{T}(P)\right)^{2}+\sum_{j \leq 2}\left(E S_{T}(P, j) \sqrt{\frac{\left(L H_{j}-L H_{j-1}\right)}{T}}\right)^{2}}

$$

where,

- $E S$ is the regulatory liquidity-adjusted expected shortfall;

- $T$ is the length of the base horizon, i.e., 10 days;

量化风险管理代考

金融代写|量化风险管理代写Quantitative Risk Management代考|The Fundamental Review of the Trading Book

对交易账簿或 FRTB 法规(BCBS 2014)的基本审查是对危机前框架的回应,该框架在许多领域被认为是不充分和薄弱的。对于交易账簿边界的定义尤其如此。事实上,内部模型方法是不够的,许多问题需要处理以建立更好的监管资本框架。

例如,尾部风险是 VaR 方法并没有充分捕捉到流动性不足的东西。大多数基于 IMA 的方法还允许广泛的多样化效应,因为它们基于在危机情况下绝对不成立的历史参数(相关性在非常紧张的市场中很大程度上变得相关)。

由于内部模型与标准化方法之间的联系不合适,因此当前的标准化方法非常不充分。此外,目前的标准化方法缺乏风险敏感性。这个问题需要与限制多元化收益和对冲一起处理。

FRTB 解决了银行业务和交易账簿之间的边界问题,以减少两账簿之间的监管套利,限制从一账簿转移到另一账簿的意愿,并引入报告指南和监管监督,以建立一个更好的框架,支配着两本书之间的界限。

FRTB 还旨在更有效地捕捉尾部风险的影响以及捕捉流动性效应。尾部风险是根据资产/风险类别从 VaR 转移到不同期限的预期缺口方法来捕获的。

在 FRTB 下,内部模型必须在桌面级别获得批准。如果课桌未获批准,这些课桌将移回标准化方法。交易台必须通过证明他们有足够的模型来证明他们的模型是合规的磷&大号归因和回溯测试程序到位。需要注意的是磷&大号归因(即基于模型的磷&大号反对基于风险的理论磷& 大号) 将受到审查,以确保风险模型正确捕捉与模型本身相关的风险。此外,套期保值和多元化收益将受到限制,并且将收取额外费用以涵盖不可建模的风险因素。

愿意使用简单方法的银行将考虑修订后的标准化方法 (RSA)。这种方法也将是银行未获得内部模型批准的后备方案。主要的方法修改是该方法现在基于跨资产类别的风险敏感性。RSA 旨在提供一种一致的方法来衡量跨地理区域的风险,为当局提供一种更好的方法来比较 IMA 和 SA 银行,因为这两种方法共享一个共同的框架。此外,标准化的违约风险费用将与剩余风险的附加项一起添加,这显然更难以建模。因此,遵循 FRTB 并从资本计算的角度来看,银行提供了两种执行它们的可能性。这些将在下文中介绍。

金融代写|量化风险管理代写Quantitative Risk Management代考|Standardised Approach

正如标准化方法资本要求 (BCBS 2016a) 中所述,是三个组成部分的简单总和:基于敏感性的方法下的风险费用、违约风险费用和剩余风险附加值。

基于敏感性的方法下的风险费用必须通过汇总以下风险度量来计算:

- Delta:基于银行交易账户对监管 delta 风险因素的敏感性的风险度量。Delta 敏感度将用作聚合公式的输入,该公式为基于敏感度的方法提供资本要求。

- Vega:一种风险度量,也基于对监管 vega 风险因素的敏感性,用作与 delta 风险类似的聚合公式的输入。

- 曲率:一种风险度量,它捕捉期权价值的价格变化的增量风险未捕捉到的增量风险。曲率风险基于两种压力情景,包括对给定风险因素的向上冲击和向下冲击。这两种情况中最严重的损失是风险头寸被用作提供资本费用的聚合公式的输入。

为了解决财务压力期间相关性可能增加或减少的风险,必须根据相关参数指定值的三种不同情景,为基于敏感性的方法定义的每个风险类别计算三个风险费用数字ρķl(即桶内风险因素之间的相关性)和CbC(即风险类别内的桶之间的相关性)。各个风险类别之间不得承认多样化收益。有关参数的更多详细信息,我们参考 BCBS (2016a)。

银行必须根据银行内部独立风险控制部门用于向高级管理层报告市场风险或实际损益的工具价格或定价模型来确定每个 delta 和 vega 敏感性和曲率情景。

违约风险费用在针对非证券化、证券化(非相关交易组合)和证券化相关交易组合的违约风险的三个独立资本费用计算中捕获跳至违约风险。它是根据银行账簿中的信用风险处理进行校准的,以减少全行类似风险敞口的资本要求的潜在差异。在风险权重范围内允许进行一些套期保值确认。在不同的桶之间不得承认多样化的好处。

此外,委员会承认,并非所有市场风险都可以用标准化方法捕捉,因为这可能需要一个过度复杂的制度。因此引入了剩余风险附加项,以确保充分覆盖市场风险。

监管机构将能够坚持对银行内部模型进行一段时间的初始监控和实时测试,然后再将其用于监管资本目的。除了这些一般标准外,使用内部模型作为资本目的的银行将受到下文详述的额外要求的约束。

金融代写|量化风险管理代写Quantitative Risk Management代考|Internal Models Approach

使用内部模型来确定监管资本将取决于银行监管机构的明确批准。在多个司法管辖区开展重大交易活动的银行的母国和东道国监管机构打算合作以确保有效的审批流程。

- 对本行风险管理体系概念健全、执行健全的情况感到满意;

- 监管机构认为,银行拥有足够数量的员工,他们不仅在交易领域,而且在风险控制、审计以及必要时的后台办公领域,都能够熟练使用复杂的模型;

- 根据监管机构的判断,银行的模型在衡量风险方面具有合理准确的可靠记录;

- 银行按照 BCBS (2016a) 中讨论的思路定期进行压力测试;和

- 包含在监管资本确定内部模型中的头寸在已通过所需测试的经批准的交易平台中持有。

从量化的角度来看,该文件规定如下: 银行可以灵活地设计其模型的精确性质,但以下最低标准将适用于计算其资本费用。个别银行或其监管机构将有权酌情采用更严格的标准。出于监管资本目的,必须每天为全银行内部模型计算“预期缺口”。对于银行希望将其纳入内部模型范围以用于监管资本目的的每个交易台,还必须每天计算预期短缺。

在计算预期缺口时,a97.5将使用第 th 个百分位的单尾置信水平。在计算预期缺口时,BCBS (2016a) 中描述的流动性范围(见表 2.2)必须通过缩放在基准范围上计算的预期缺口来反映。流动性范围的预期缺口必须根据 10 天基本流动性范围的预期缺口计算,并按如下方式应用于该基准范围结果:

和小号=(和小号吨(磷))2+∑j≤2(和小号吨(磷,j)(大号Hj−大号Hj−1)吨)2

在哪里,

- 和小号是监管流动性调整后的预期缺口;

- 吨是基准层的长度,即10天;

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。