会计代写|金融会计代写Financial Accounting代考|ACC337

如果你也在 怎样代写金融会计Financial Accounting这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

金融会计是会计的一个具体分支,涉及记录、总结和报告一段时期内企业经营产生的无数交易的过程。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融会计Financial Accounting方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融会计Financial Accounting代写方面经验极为丰富,各种代写金融会计Financial Accounting相关的作业也就用不着说。

我们提供的金融会计Financial Accounting及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

会计代写|金融会计代写Financial Accounting代考|Re-measurements and other comprehensive income

As noted earlier, if a company owns listed equities that rise in value, it seems relevant and verifiable to record the assets in the balance sheet at the higher values. Are such gains to be treated as income? The IASB concludes that they should indeed be. They meet the definition of income (see Section 8.4.1). As noted in Chapter 6 , two income statements are now to be found under the rules of the IASB, the United Kingdom and the United States. The gains or losses on any revaluations of some financial assets (see Chapter 11) are shown in the first income statement, i.e. treated as profit or loss. The same applies to gains or losses on investment properties (see Chapter 9).

However, if a company’s other land and buildings are revalued (see Chapter 9), the resulting gains are not treated as ‘profit or loss’ but go to the second income statement (called ‘other comprehensive income’). An example of 2018 is shown as Figure 8.7, which relates again to the BASF Group. Some of the issues raised by this are too complex to consider at this stage, and you should not try to understand all the detail. We show extracts relating to both 2017 and 2018 . All companies will have their own individual characteristics, and no example should be regarded as ‘typical’. But, in relation to this particular illustration, you should note several conclusions. As presented here, the figure starts with the end result of ‘profit or loss’, called ‘Income after taxes’ by BASF. A number of adjustments are shown, all of which increase or decrease the closing net assets and therefore the closing net equity, but none of which, according to the ‘theory’, relate to the operating activities or to the interest costs of the business during the year. Secondly, the numbers involved may be significant, so an understanding of ‘performance’ over the year is seriously affected. Thirdly, the changes over time are often unpredictable. This example illustrates this particularly well. Note that the effect of the ‘remeasurement of defined benefit (pension) plans’ moves from a gain of over $€ 1$ billion in 2017 to a loss of almost $€ 1$ billion in 2018, a change over the two years of over $€ 2$ billion in apparent performance. Conversely the ‘unrealised gains/losses from currency translation’ move from a loss of over $€ 2$ billion in 2017 to a small gain of almost $€ 200,000$ in 2018, again a net movement of over $€ 2$ billion, but in the opposite direction to the pension-related movement. So what should an investor predict for 2019 ?

Unfortunately, there is no clear rationale for the distinction between the gains in one statement and those in the other. For example, most of the items in Figure $8.7$ are unrealised, in the sense that no sale has yet occurred. At first sight, the opening ‘income after taxes’ figure is concerned with operations. However, if the head office were sold after 50 years, any gains would be recorded in profit or loss even though they are not to do with operations. The 2018 framework (Chapter 7) briefly deals with this issue, suggesting that ‘profit or loss’ relates to performance of the period, but this does not solve these problems.

会计代写|金融会计代写Financial Accounting代考|Capital maintenance

One of the functions served by accounting for centuries is the calculation of distributable profit. A sole trader likes to calculate how much cash can reasonably be taken from the business as a result of a year’s successful operations. This becomes a vital issue when there are several owners. In the context of companies, the issue becomes one of determining the size of dividend payments.

A long-standing tradition of accountants is that dividends should only be paid to the extent that profit has been made. Otherwise, the business will be run down. This principle can be found in the laws of many countries, including EU laws based on the Second company law Directive. Adherence to the principle is said to protect the creditors of a company by restraining the cash outflows to shareholders.

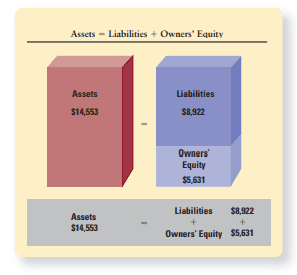

From the accounting equation introduced in Chapter 2 and discussed again in Section 8.2, it is clear that an increase in equity is caused by an increase in net assets. For example, suppose that a retail company buys inventory for $€ 10 \mathrm{~m}$ cash and sells it for $€ 12 \mathrm{~m}$ cash in the same year. The net assets rise by $€ 2 \mathrm{~m}$, and the corresponding increase in equity appears to suggest that a dividend payment of $€ 2 \mathrm{~m}$ would be reasonable. However, the retailer perhaps used shops and delivery vans as part of the process of making the profit, so some account should be taken of the need to preserve those assets before any ‘profit’ is identified. This leads to the recognition of the expense called depreciation, as discussed in Chapter 9.

Further, suppose that the retailer’s shop has nearly doubled in market value from $€ 80 \mathrm{~m}$ to $€ 150 \mathrm{~m}$. The shop had been bought many years ago with cash contributed by the shareholders. If the retailer sells the shop for $€ 150 \mathrm{~m}$ cash, is the profit sensibly available for distribution as dividends? The company has cash and profit. However, in order to stay in business at the same level of operations, it will probably need to buy a new shop for at least $€ 150 \mathrm{~m}$. If the capital of the company is viewed as including one shop, then the gain cannot be paid out without drastically reducing the company’s capital. Taking account of this can be called ‘physical, or operating, capital maintenance’. On the other hand, if the capital is seen as the original money amount of $€ 80 \mathrm{~m}$ contributed by the shareholders, then the excess could be regarded as distributable (called ‘financial capital maintenance’), as the full amount of $€ 80 \mathrm{~m}$ would still remain within the company.

金融会计代考

会计代写|金融会计代写Financial Accounting代考|Re-measurements and other comprehensive income

如前所述,如果一家公司拥有价值上升的上市股票,那么在资产负债表中以更高的价值记录资产似乎是相关且可验证的。这些收益是否应视为收入?IASB 的结论是它们确实应该如此。它们符合收入的定义(参见第 8.4.1 节)。如第 6 章所述,现在可以根据 IASB、英国和美国的规则找到两份损益表。某些金融资产(见第 11 章)的任何重估产生的利得或损失显示在第一份损益表中,即作为损益处理。这同样适用于投资性房地产的收益或损失(见第 9 章)。

但是,如果对公司的其他土地和建筑物进行重估(见第 9 章),由此产生的收益不会作为“损益”处理,而是计入第二份损益表(称为“其他综合收益”)。2018 年的示例如图 8.7 所示,它再次与巴斯夫集团相关。由此提出的一些问题过于复杂,现阶段无法考虑,您不应该试图了解所有细节。我们展示了与 2017 年和 2018 年相关的摘录。所有的公司都会有自己的个性,没有一个例子应该被视为“典型”。但是,关于这个特定的例子,你应该注意几个结论。如此处所示,该图以“利润或亏损”的最终结果开始,巴斯夫将其称为“税后收入”。显示了一些调整,所有这些都增加或减少了期末净资产,因此增加或减少了期末净权益,但根据“理论”,这些都与当年的经营活动或业务的利息成本无关。其次,涉及的数字可能很大,严重影响对全年“业绩”的理解。第三,时间的变化往往是不可预测的。这个例子特别好地说明了这一点。请注意,“重新衡量固定收益(养老金)计划”的影响从超过 因此,对一年来“绩效”的理解受到严重影响。第三,时间的变化往往是不可预测的。这个例子特别好地说明了这一点。请注意,“重新衡量固定收益(养老金)计划”的影响从超过 因此,对一年来“绩效”的理解受到严重影响。第三,时间的变化往往是不可预测的。这个例子特别好地说明了这一点。请注意,“重新衡量固定收益(养老金)计划”的影响从超过€€1亿 2017 年亏损近€€12018 年 10 亿,两年多的变化€€2亿元的表观表现。相反,“货币换算的未实现收益/损失”从超过€€2亿在 2017 年几乎小幅增长€€200,0002018 年,再次净移动超过€€2亿,但与养老金相关运动的方向相反。那么投资者应该如何预测 2019 年呢?

不幸的是,对于一种陈述中的收益与另一种陈述中的收益之间的区别没有明确的理由。例如,图中的大部分项目8.7未实现,即尚未发生销售。乍一看,开头的“税后收入”数字与运营有关。但是,如果总部在 50 年后被出售,即使与运营无关,任何收益也会计入损益。2018 年框架(第 7 章)简要处理了这个问题,表明“损益”与该期间的业绩有关,但这并没有解决这些问题。

会计代写|金融会计代写Financial Accounting代考|Capital maintenance

几个世纪以来会计服务的功能之一是计算可分配利润。个体经营者喜欢计算由于一年的成功经营,可以合理地从企业中获取多少现金。当有多个所有者时,这将成为一个至关重要的问题。在公司的背景下,问题变成了确定股息支付规模的问题之一。

会计师的一个长期传统是,只应在盈利的范围内支付股息。否则,生意就会倒闭。这个原则可以在许多国家的法律中找到,包括基于第二公司法指令的欧盟法律。据说遵守该原则可以通过限制股东的现金流出来保护公司的债权人。

从第 2 章介绍并在第 8.2 节再次讨论的会计等式可以清楚地看出,权益的增加是由净资产的增加引起的。例如,假设一家零售公司为€€10 米现金并出售€€12 米同年现金。净资产增加€€2 米,相应的权益增加似乎表明股息支付€€2 米会是合理的。然而,零售商可能使用商店和送货车作为获利过程的一部分,因此在确定任何“利润”之前,应考虑到保护这些资产的必要性。这导致确认称为折旧的费用,如第 9 章所述。

此外,假设零售商商店的市场价值从€€80 米至€€150 米. 这家店是多年前股东用现金买下的。如果零售商以€€150 米现金,利润是否可以合理地作为股息分配?公司有现金和利润。但是,为了保持相同运营水平的业务,它可能至少需要购买一家新店€€150 米. 如果公司的资本被视为包括一家商店,那么如果不大幅减少公司的资本,就无法支付收益。考虑到这一点可以称为“物理或运营资本维护”。另一方面,如果资本被视为原始货币量€€80 米由股东出资,则超出部分可视为可分配(称为“财务资本维持”),因为€€80 米仍将留在公司。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。