会计代写|中级财务会计代写Intermediate Financial Accounting代考|ACF5956

如果你也在 怎样代写中级财务会计Intermediate Financial Accounting这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

财务会计是通过财务报表记录、总结和报告公司业务交易的过程。这些报表是:利润表、资产负债表、现金流量表和留存收益表。

statistics-lab™ 为您的留学生涯保驾护航 在代写中级财务会计Intermediate Financial Accounting方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写中级财务会计Intermediate Financial Accounting代写方面经验极为丰富,各种代写中级财务会计Intermediate Financial Accounting相关的作业也就用不着说。

我们提供的中级财务会计Intermediate Financial Accounting及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

会计代写|中级财务会计代写Intermediate Financial Accounting代考|The Financial Statements

Where is the happiest place on earth? Walt Disney World or Disneyland, of course! The Disney theme parks in Orlando, Florida, and Anaheim, California, are famous for providing the ultimate family entertainment experience. However, these two parks are only a small part of The Walt Disney Company’s worldwide entertainment empire. The company owns vacation resorts, theme and water parks, hotels, motion-picture and recording studios, and cable TV networks throughout the world. Disney also sells billions of dollars of branded merchandise through retail, online, and wholesale distribution channels. How does Disney decide what to invest in and how to operate its businesses so as to maximize its profits? One way to find out is by studying its financial accounting information.

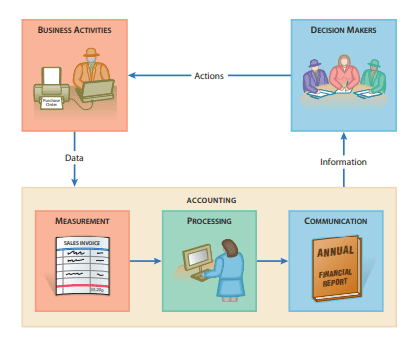

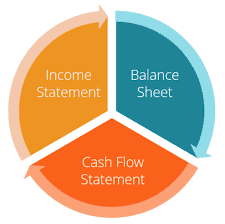

Most chapters of this book begin with an actual financial statement. Financial statements are the business documents companies use to report the results of their activities to people and groups that can include managers, investors, creditors, and regulatory agencies. These parties then use the reported information to make a variety of decisions, such as whether to invest in or loan money to the companies. The following four basic financial statements are used for these purposes:

- Income statement (sometimes known as the statement of operations)

- Statement of retained earnings (usually included in the statement of stockholders’ equity)

- Balance sheet (sometimes known as the statement of financial position)

- Statement of cash flows

In Chapters 1-3, we will look at the contents of these statements using The Walt Disney Company as an example. For instance, the following financial statement is Disney’s income statement for the year ended October 1 , 2016.

Chapter 1 also explains generally accepted accounting principles, their underlying assumptions and concepts, and the bodies responsible for issuing accounting standards. Last, but not least, we examine the judgment process needed to make good accounting decisions.

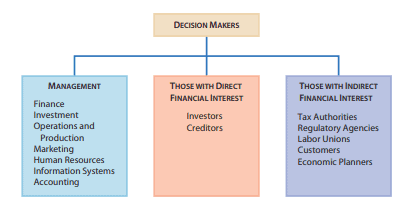

会计代写|中级财务会计代写Intermediate Financial Accounting代考|Describe the Decision Makers Who Use Accounting

Decision makers use many types of information. For example, a banker needs financial information from an applicant to decide whether to grant a loan request. Managers at Disney use revenue forecasts along with design-and-engineering plans to decide where to locate new theme parks and how large they will be. Let’s explore how decision makers use accounting information.

- Individuals. People like you manage their personal bank accounts, decide whether to rent an apartment or buy a house, and calculate the monthly income and expenditures of their businesses. Accounting provides the information people need to make these decisions.

- Investors and creditors. Investors and creditors provide the money to finance The Walt Disney Company. Investors want to know how much income they can expect to earn on an investment. Creditors want to know when and how the company is going to pay them back. These decisions also require accounting information.

- Regulatory bodies. All kinds of regulatory bodies use accounting information. For example, the Intemal Revenue Service (IRS) and various state and local governments require businesses, individuals, and other types of organizations to pay income, property, excise, and other taxes. The Securities and Exchange Commission (SEC) requires companies with publicly-traded stock to provide it with many kinds of periodic financial reports. All of these reports contain accounting information.

- Nonprofit organizations. Churches, hospitals, and charities such as Habitat for Humanity and the Red Cross base many of their operating decisions on accounting data. These nonprofit organizations also have to file periodic financial reports with the IRS and state governments, even though they will owe no income taxes.

财务会计代考

会计代写|中级财务会计代写中级财务会计代考|财务报表

世界上最快乐的地方是哪里?当然是沃尔特·迪士尼乐园了!位于佛罗里达州奥兰多和加利福尼亚州阿纳海姆的迪士尼主题公园以提供极致的家庭娱乐体验而闻名。然而,这两个公园只是华特迪士尼公司全球娱乐帝国的一小部分。该公司在全球拥有度假胜地、主题和水上公园、酒店、电影和录音棚以及有线电视网络。迪士尼还通过零售、在线和批发分销渠道销售了数十亿美元的品牌商品。迪士尼如何决定投资什么,如何经营其业务以实现利润最大化?一种方法是研究其财务会计信息。这本书的大部分章节都以一份实际的财务报表开始。财务报表是公司用来向包括经理、投资者、债权人和监管机构在内的个人和团体报告其活动结果的商业文件。然后,这些当事人利用所报告的信息做出各种决定,例如是否向这些公司投资或贷款。以下四种基本财务报表用于这些目的

损益表(有时称为营业利润表)留存收益表(通常包含在股东权益表中)资产负债表(有时称为财务状况表)现金流量表

在第1-3章中,我们将以华特迪士尼公司为例来研究这些报表的内容。例如,以下的财务报表是迪士尼截至2016年10月1日的年度损益表

第一章还解释了公认的会计原则,它们的基本假设和概念,以及负责发布会计准则的机构。最后,但并非最不重要的是,我们考察了做出良好会计决策所需的判断过程

会计代写|中级财务会计代写中级财务会计代考|描述使用会计的决策者

决策者使用多种类型的信息。例如,银行家需要申请人的财务信息来决定是否批准贷款请求。迪士尼的管理人员根据收入预测以及设计和工程计划来决定新主题公园的选址和规模。让我们来探讨决策者如何使用会计信息

- 个人。像你这样的人管理自己的个人银行账户,决定是租房还是买房,计算每月的收入和支出。会计为人们提供做出这些决定所需的信息。

- 投资者和债权人投资者和债权人提供资金来资助华特迪士尼公司。投资者想知道他们的投资预期能获得多少收益。债权人想知道该公司何时以及如何偿还债务。这些决策还需要会计信息。

- 监管机构。各种监管机构都在使用会计信息。例如,美国国税局(IRS)和各个州和地方政府要求企业、个人和其他类型的组织支付收入税、财产税、消费税和其他税。美国证券交易委员会(SEC)要求上市公司向其提供多种类型的定期财务报告。

- 非营利性组织。教堂、医院和慈善机构,如仁爱之家和红十字会,他们的许多运营决策都是基于会计数据。这些非营利组织还必须定期向美国国税局和州政府提交财务报告,尽管他们不需要缴纳所得税.

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。