如果你也在 怎样代写金融中的随机方法Stochastic Methods in Finance这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

随机建模是金融模型的一种形式,用于帮助做出投资决策。这种类型的模型使用随机变量预测不同条件下各种结果的概率。随着现代经济学、金融学实证研究的发展,金融中的随机方法Stochastic Methods in Finance作为一种数学工具具有越来越重要的应用价值。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融中的随机方法Stochastic Methods in Finance方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融中的随机方法Stochastic Methods in Finance方面经验极为丰富,各种代写金融中的随机方法Stochastic Methods in Finance相关的作业也就用不着说。

我们提供的金融中的随机方法Stochastic Methods in Finance及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等楖率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Introduction

In recent years there has been a significant growth of inyestment products aimed at attracting investors who are worried about the downside potential of the financial markets for pension investments. The main feature of these products is a minimum guaranteed return together with exposure to the upside movements of the market.

There are several different guarantees available in the market. The one most commonly used is the nominal guarantee which guarantees a fixed percentage of the initial investment. However there also exist funds with a guarantee in real terms which is linked to an inflation index. Another distinction can be made between fixed and flexible guarantees, with the fixed guarantee linked to a particular rate and the flexible to for instance a capital market index. Real guarantees are a special case of flexible guarantees. Sometimes the guarantee of a minimum rate of return is even set relative to the performance of other pension funds.

Return guarantees typically involve hedging or insuring. Hedging involves eliminating the risk by sacrificing some or all of the potential for gain, whereas insuring involves paying an insurance premium to eliminate the risk of losing a large amount.

Many government and private pension schemes consist of defined benefit plans. The task of the pension fund is to guarantee benefit payments to retiring clients by investing part of their current wealth in the financial markets. The responsibility of the pension fund is to hedge the client’s risk, while meeting the solvency requirements in such a way that all benefit payments are met. However at present there are significant gaps between fund values, contributions made by employees, and pension obligations to retirees.

One way in which the guarantee can be achieved is by investing in zero-coupon Treasury bonds with a maturity equal to the time horizon of the investment product in question. However using this option foregoes all upside potential. Even though the aim is protect the investor from the downside, a reasonable expectation of returns higher than guaranteed needs to remain.

In this paper we will consider long-term nominal minimum guaranteed return plans with a fixed time horizon. They will be closed end guarantee funds; after the initial contribution there is no possibility of making any contributions during the lifetime of the product. The main focus will be on how to optimally hedge the risks involved in order to avoid having to buy costly insurance.

However this task is not straightforward, as it requires long-term forecasting for all investment classes and dealing with a stochastic liability. Dynamic stochastic programming is the technique of choice to solve this kind of problem as such a model will automatically hedge current portfolio allocations against the future uncertainties in asset returns and liabilities over a long horizon (see e.g. Dempster et $a l, 2003$ ). This will lead to more robust decisions and previews of possible future benefits and problems contrary to, for instance, static portfolio optimization models such as the Markowitz (1959) mean-variance allocation model.

Consiglio et al. (2007) have studied fund guarantees over single investment periods and Hertzog et al. $(2007)$ treat dynamic problems with a deterministic risk barnier. However a practical method should have the flexibility to take into account multiple time periods, portfolio constraints such as prohibition of short selling and varying degrees of risk aversion. In addition, it should be based on a realistic representation of the dynamics of the relevant factors such as asset prices or returns and should model the changing market dynamics of risk management. All these factors have been carefully addressed here and are explained further in the sequel.

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Stochastic Optimization Framework

This chapter looks at several methods to optimally allocate assets for a minimum guaranteed return fund using expected average and expected maximum shortfall risk measures relative to the current value of the guarantee. The models will be applied to eight different assets: coupon bonds with maturity equal to $1,2,3,4,5$, 10 and 30 years and an equity index, and the home currency is the euro. Extensions incorporated into these models are the presence of coupon rates directly dependent on the term structure of bond returns and the annual rolling of the coupon-bearing bonds.

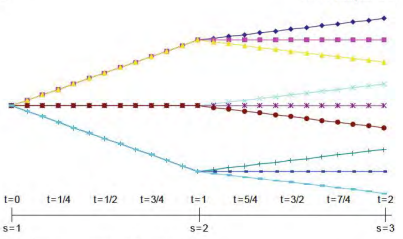

We consider a discrete time and space setting. The time interval considered is given by $\left{0, \frac{1}{12}, \frac{2}{12}, \ldots, T\right}$, where the times indexed by $t=0,1, \ldots, T-1$ correspond to decision times at which the fund will trade and $T$ to the planning horizon at which no decision is made, see Figure 1. We will be looking at a five-year horizon.

Uncertainty $\Omega$ is represented by a scenario tree, in which each path through the tree corresponds to a scenario $\omega$ in $\Omega$ and each node in the tree corresponds to a time along one or more scenarios. An example scenario tree is given in Figure 2 . The probability $p(\omega)$ of scenario $\omega$ in $\Omega$ is the reciprocal of the total number of scenarios as the scenarios are generated by Monte Carlo simulation and are hence equiprobable.

The stock price process $\mathbf{S}$ is (initially) assumed to follow a geometric Brownian motion, i.e.

$$

\frac{d \mathbf{S}{t}}{\mathbf{S}{t}}=\mu_{S} d t+\sigma_{S} d \mathbf{W}{t}^{S} $$ where $d \mathbf{W}{t}^{S}$ is correlated with the $d \mathbf{W}_{t}$ terms driving the three term structure factors discussed in Section $3 .$

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Model Constraints

Let (see Table 1)

- $h_{t}(\omega)$ denote the shortfall at time tand scenario $\omega$, i.e.

$$

h_{t}(\omega):=\max \left(0, L_{t}(\omega)-W_{t}(\omega)\right) \quad \forall \omega \in \Omega \quad t \in T^{\text {total }}

$$ - $H(\omega):=\max {t \in T^{\text {total }}} h{t}(\omega)$ denote the maximum shortfall over time for scenario $\omega$.

The constraints considered for the minimum guaranteed return problem are: - cash balance constraints. These constraints ensure that the net cash flow at each time and at each scenario is equal to zero

$$

\sum_{a \in A} f P_{0, a}^{b u y}(\omega) x_{0, a}^{+}(\omega)=W_{0} \quad \omega \in \Omega

$$

Designing Minimum Guaranteed Return Funds

25

$$

\sum_{a \in A \backslash{S}} \frac{1}{2} \delta_{t-1}^{a}(\omega) F^{a} x_{t, a}^{-}(\omega)+\sum_{a \in A} g P_{t, a}^{s e l l}(\omega) x_{t, a}^{-}(\omega)=\sum_{a \in A} f P_{t, a}^{b u y}(\omega) x_{t, a}^{+}(\omega)

$$

$\omega \in \Omega \quad 1 \in T^{d} \backslash{0} .$

In (4) the left-hand side represents the cash freed up to be reinvested at time $t \in T^{d} \backslash{0}$ and consists of two distinct components. The first term represents the semi-annual coupons received on the coupon-bearing Treasury bonds held between time $t-1$ and $t$, the second term represents the cash obtained from selling part of the portfolio. This must equal the value of the new assets bought given by the right hand side of (4).

金融中的随机方法代写

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Introduction

近年来,旨在吸引担心金融市场对养老金投资的下行潜力的投资者的投资产品显着增长。这些产品的主要特点是最低保证回报以及对市场上行趋势的敞口。

市场上有几种不同的保证。最常用的一种是名义担保,它保证初始投资的固定百分比。然而,也存在与通胀指数挂钩的实际担保基金。另一个区别是固定担保和灵活担保,固定担保与特定利率挂钩,而灵活担保与资本市场指数挂钩。实物担保是灵活担保的一种特殊情况。有时,最低回报率的保证甚至是相对于其他养老基金的表现而设定的。

退货保证通常涉及对冲或保险。对冲涉及通过牺牲部分或全部潜在收益来消除风险,而保险涉及支付保险费以消除大量损失的风险。

许多政府和私人养老金计划由固定福利计划组成。养老基金的任务是通过将部分现有财富投资于金融市场来保证向退休客户支付福利。养老基金的职责是对冲客户的风险,同时满足偿付能力要求,从而满足所有福利支付。然而,目前基金价值、员工缴款和退休人员的养老金义务之间存在显着差距。

实现担保的一种方式是投资于期限与相关投资产品的期限相同的零息国债。但是,使用此选项会放弃所有上行潜力。尽管目标是保护投资者免受不利影响,但仍需要保持对高于保证的回报的合理预期。

在本文中,我们将考虑具有固定时间范围的长期名义最低保证回报计划。它们将是封闭式担保基金;在初始贡献之后,在产品的生命周期内不可能做出任何贡献。主要关注点是如何以最佳方式对冲所涉及的风险,以避免购买昂贵的保险。

然而,这项任务并不简单,因为它需要对所有投资类别进行长期预测并处理随机负债。动态随机规划是解决此类问题的首选技术,因为这样的模型将自动对冲当前的投资组合配置,以应对长期资产回报和负债的未来不确定性(参见例如 Dempster 等一种一世,2003)。与诸如 Markowitz (1959) 均值方差分配模型之类的静态投资组合优化模型相反,这将导致更稳健的决策和对未来可能的收益和问题的预测。

Consiglio 等人。(2007) 研究了单一投资期间的基金担保,Hertzog 等人。(2007)用确定性风险边界处理动态问题。然而,一种实用的方法应该能够灵活地考虑多个时间段、投资组合限制,例如禁止卖空和不同程度的风险规避。此外,它应基于对资产价格或收益等相关因素动态的真实表示,并应模拟风险管理的不断变化的市场动态。所有这些因素都在这里得到了仔细的解决,并在续集中进行了进一步的解释。

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Stochastic Optimization Framework

本章着眼于几种方法,使用相对于担保当前价值的预期平均和预期最大缺口风险度量,为最低保证回报基金优化资产配置。该模型将应用于八种不同的资产:到期的息票债券1,2,3,4,5, 10 年和 30 年和一个股票指数,本国货币是欧元。纳入这些模型的扩展是票面利率的存在直接取决于债券回报的期限结构和附息债券的年度滚动。

我们考虑离散的时间和空间设置。考虑的时间间隔由下式给出\left{0, \frac{1}{12}, \frac{2}{12}, \ldots, T\right}\left{0, \frac{1}{12}, \frac{2}{12}, \ldots, T\right},其中时间索引为吨=0,1,…,吨−1对应于基金交易的决策时间和吨到没有做出决定的规划期限,请参见图 1。我们将着眼于 5 年的期限。

不确定Ω由场景树表示,其中通过树的每条路径对应一个场景ω在Ω树中的每个节点对应一个或多个场景的时间。图 2 给出了一个示例场景树。概率p(ω)情景的ω在Ω是场景总数的倒数,因为场景是由蒙特卡罗模拟生成的,因此是等概率的。

股价过程小号(最初)假设遵循几何布朗运动,即

d小号吨小号吨=μ小号d吨+σ小号d在吨小号在哪里d在吨小号与d在吨驱动本节讨论的三个期限结构因素的术语3.

统计代写|金融中的随机方法作业代写Stochastic Methods in Finance代考|Model Constraints

让(见表 1)

- H吨(ω)表示时间和情景的短缺ω, IE

H吨(ω):=最大限度(0,大号吨(ω)−在吨(ω))∀ω∈Ω吨∈吨全部的 - $H(\omega):=\max {t \in T^{\text {total }}} h {t}(\omega)d和n这吨和吨H和米一种X一世米你米sH这r吨F一种一世一世这v和r吨一世米和F这rsC和n一种r一世这\欧米茄$。

考虑最小保证回报问题的约束是: - 现金余额限制。这些约束确保在每个时间和每个场景下的净现金流等于零

∑一种∈一种F磷0,一种b你是(ω)X0,一种+(ω)=在0ω∈Ω

设计最低保证回报基金

25

∑一种∈一种∖小号12d吨−1一种(ω)F一种X吨,一种−(ω)+∑一种∈一种G磷吨,一种s和一世一世(ω)X吨,一种−(ω)=∑一种∈一种F磷吨,一种b你是(ω)X吨,一种+(ω)

ω∈Ω1∈吨d∖0.

在(4)中,左侧代表当时释放出来可用于再投资的现金吨∈吨d∖0并由两个不同的组件组成。第一项代表在不同时期持有的附息国债收到的半年度息票吨−1和吨,第二项代表出售部分投资组合获得的现金。这必须等于 (4) 右侧给出的购买的新资产的价值。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。统计代写|python代写代考

随机过程代考

在概率论概念中,随机过程是随机变量的集合。 若一随机系统的样本点是随机函数,则称此函数为样本函数,这一随机系统全部样本函数的集合是一个随机过程。 实际应用中,样本函数的一般定义在时间域或者空间域。 随机过程的实例如股票和汇率的波动、语音信号、视频信号、体温的变化,随机运动如布朗运动、随机徘徊等等。

贝叶斯方法代考

贝叶斯统计概念及数据分析表示使用概率陈述回答有关未知参数的研究问题以及统计范式。后验分布包括关于参数的先验分布,和基于观测数据提供关于参数的信息似然模型。根据选择的先验分布和似然模型,后验分布可以解析或近似,例如,马尔科夫链蒙特卡罗 (MCMC) 方法之一。贝叶斯统计概念及数据分析使用后验分布来形成模型参数的各种摘要,包括点估计,如后验平均值、中位数、百分位数和称为可信区间的区间估计。此外,所有关于模型参数的统计检验都可以表示为基于估计后验分布的概率报表。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

statistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

机器学习代写

随着AI的大潮到来,Machine Learning逐渐成为一个新的学习热点。同时与传统CS相比,Machine Learning在其他领域也有着广泛的应用,因此这门学科成为不仅折磨CS专业同学的“小恶魔”,也是折磨生物、化学、统计等其他学科留学生的“大魔王”。学习Machine learning的一大绊脚石在于使用语言众多,跨学科范围广,所以学习起来尤其困难。但是不管你在学习Machine Learning时遇到任何难题,StudyGate专业导师团队都能为你轻松解决。

多元统计分析代考

基础数据: $N$ 个样本, $P$ 个变量数的单样本,组成的横列的数据表

变量定性: 分类和顺序;变量定量:数值

数学公式的角度分为: 因变量与自变量

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。