如果你也在 怎样代写量化风险管理Quantitative Risk Management这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

项目管理中的定量风险管理是将风险对项目的影响转换为数字的过程。这种数字信息经常被用来确定项目的成本和时间应急措施。

statistics-lab™ 为您的留学生涯保驾护航 在代写量化风险管理Quantitative Risk Management方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写量化风险管理Quantitative Risk Management代写方面经验极为丰富,各种代写量化风险管理Quantitative Risk Management相关的作业也就用不着说。

我们提供的量化风险管理Quantitative Risk Management及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

金融代写|量化风险管理代写Quantitative Risk Management代考|Solvency II Directives

EU insurance legislation aims to unify a single EU insurance market and enhance consumer protection. The third-generation Insurance Directives established an “EU passport” (i.e. a single licence, similar to the financial passport banks need to operate in the European Union) for insurers to operate in all member states if EU conditions are met. Several member states concluded the EU minima were not sufficient, and enhance the requirements with their own reforms, which unfortunately led to differing regulations, hampering the harmonisation goal.

Since the initial Solvency I Directive 73/239/EEC was introduced in 1973 , more elaborate risk management systems developed. While the “Solvency $\Gamma$ ” Directive aimed at revising and updating the current EU Solvency regime, Solvency II has a much wider scope. The Solvency II Directive (2009/138/EC (Eling et al. 2007)) is a Directive in European Union law that codifies and harmonises EU insurance regulations. This directive primary concerns the amount of capital that EU insurance companies must hold to reduce the risk of insolvency. Following an EU Parliament vote on the Omnibus II Directive on 11 March 2014, Solvency II came into effect on 1 January 2016. Solvency II reflects new risk management practices to define required capital and manage risk. A solvency capital requirement has the following purposes:

- To reduce the risk that an insurer would be unable to meet claims;

- To reduce the losses suffered by policyholders in the event that a firm is unable to meet all claims fully;

- To provide early warning to supervisors so that they can intervene promptly if capital falls below the required level; and

- To promote confidence in the financial stability of the insurance sector

Solvency II is somewhat similar to the banking regulations of Basel II. For example, the proposed Solvency II framework has three main areas (pillars): - Pillar 1 consists of the quantitative requirements (for example, the amount of capital an insurer should hold).

- Pillar 2 sets out requirements for the governance and risk management of insurers, as well as for the effective supervision of insurers.

- Pillar 3 focuses on disclosure and transparency requirements.

The pillar 1 framework sets out qualitative and quantitative requirements for calculation of technical provisions and solvency capital requirement (SCR) using either a standard formula given by the regulators or an internal model developed by the (re)insurance company. Technical provisions comprise two components: the best estimate of the liabilities (i.e. the central actuarial estimate) plus a risk margin. Technical provisions are intended to represent the current amount the (re)insurance company would have to pay for an immediate transfer of its obligations to a third party.

金融代写|量化风险管理代写Quantitative Risk Management代考|Credit Risk

Credit risk is the risk that counterparties default on their obligations, i.e., the risk that a debtor cannot fulfill his repayment obligations. Credit events include the loss of the principal, the default on interest, some cash flows disruption, or cost escalation. The losses related to credit events vary in amounts and causes. For example, a company which fails to pay one of its employees on the due date for special reason is mechanically considered as default. Therefore, the occurrence of a credit event is not necessarily an evidence of the risk of the investment. In order to limit the risk of losing the money lent to borrowers, sovereigns, companies, etc., a bank undertakes various verifications and evaluates the potential loss engendered by potential credit events.

Losses can arise in a number of circumstances, for example:

- A consumer fails to make a payment on a mortgage loan, a credit card, or any other loan.

- A company is unable to repay asset-secured fixed or floating charge debt.

- A company does not pay one of its invoices when due.

- A government bond issuer does not make a payment on a coupon or principal payment when due.

- An insolvent insurance company does not pay a policy obligation.

- A bank becoming insolvent will not pay back funds to a depositor.

- Bankruptcy protection to an insolvent consumer or business is granted by a government (Chapter 11 of Title 11 of the United States Bankruptcy Code).

It is noteworthy to mention that these may happen due to the materialisation of natural, economical, and human risks.

Credit risk arises when borrowers are unable to pay back their debt either willingly or unwillingly. Therefore, as mentioned before, to reduce the lender’s credit risk exposure, lenders usually perform a credit check on the prospective borrower, besides may require borrowers to take out the appropriate insurance, such as mortgage insurance, or may seek security over some assets of the borrower or a guarantee from a third party. The lender can also either securitise the debt or sell the created assets to other companies. In general, the higher the risk, the higher the interest rate associated with the debt. From a capital charge point of view the exposure is modelled and measured as described in the following.

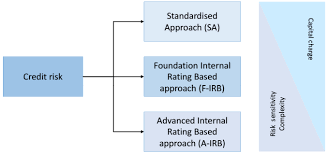

金融代写|量化风险管理代写Quantitative Risk Management代考|Standardised Approach

The standardised approach refers to a set of credit risk measurement techniques proposed under Basel II. Under this approach the banks are required to use ratings from External Credit Rating Agencies to quantify required capital for credit risk. The risk weights associated with these ratings are summarised below.Claims on retail products: This includes credit card, overdraft, auto loans, personal finance, and small business-Risk weight: 75

- Claims secured by residential property-Risk weight: $35 \%$

- Claims secured by commercial real estate-Risk weight: $100 \%$

- Overdue loans-more than 90 days other than residential mortgage loans-Risk weight:

- $150 \%$ for provisions that are less than $20 \%$ of the outstanding amount

- $100 \%$ for provisions that are between 20 and $49 \%$ of the outstanding amount

- $100 \%$ for provisions that are no less than $50 \%$ of the outstanding amount, but with supervisory discretion are reduced to $50 \%$ of the outstanding amount

- Other assets-Risk weight: $100 \%$

- Cash-Risk weight: $0 \%$

量化风险管理代考

金融代写|量化风险管理代写Quantitative Risk Management代考|Solvency II Directives

欧盟保险立法旨在统一欧盟单一保险市场并加强消费者保护。第三代保险指令建立了“欧盟护照”(即单一许可证,类似于银行在欧盟运营所需的金融护照),如果符合欧盟条件,保险公司可以在所有成员国开展业务。一些成员国认为欧盟最低标准是不够的,并通过自己的改革提高了要求,不幸的是,这导致了不同的法规,阻碍了协调目标。

自 1973 年引入最初的偿付能力 I 指令 73/239/EEC 以来,开发了更精细的风险管理系统。而“偿付能力Γ” 旨在修订和更新当前欧盟偿付能力制度的指令,偿付能力 II 具有更广泛的范围。Solvency II 指令 (2009/138/EC (Eling et al. 2007)) 是欧盟法律中的一项指令,用于编纂和协调欧盟保险法规。该指令主要涉及欧盟保险公司为降低破产风险而必须持有的资本数额。在欧盟议会于 2014 年 3 月 11 日对 Omnibus II 指令进行投票后,偿付能力 II 于 2016 年 1 月 1 日生效。偿付能力 II 反映了定义所需资本和管理风险的新风险管理实践。偿付能力资本要求具有以下目的:

- 降低保险公司无法满足索赔要求的风险;

- 在公司无法完全满足所有索赔要求的情况下,减少投保人遭受的损失;

- 向监管者提供预警,以便他们在资本低于规定水平时及时干预;和

- 为提高对保险业金融稳定性的信心,

Solvency II 与巴塞尔协议 II 的银行法规有些相似。例如,拟议的偿付能力 II 框架具有三个主要领域(支柱): - 支柱 1 包括数量要求(例如,保险公司应持有的资本金额)。

- 支柱 2 对保险公司的治理和风险管理以及对保险公司的有效监管提出了要求。

- 支柱 3 侧重于披露和透明度要求。

支柱 1 框架规定了使用监管机构给出的标准公式或(再)保险公司开发的内部模型计算技术准备金和偿付能力资本要求(SCR)的定性和定量要求。技术准备包括两个部分:负债的最佳估计(即中央精算估计)加上风险边际。技术条款旨在代表(再)保险公司为立即将其义务转移给第三方而必须支付的当前金额。

金融代写|量化风险管理代写Quantitative Risk Management代考|Credit Risk

信用风险是交易对手违约的风险,即债务人无法履行还款义务的风险。信用事件包括本金损失、利息违约、部分现金流中断或成本上升。与信用事件相关的损失金额和原因各不相同。例如,一家公司因特殊原因未能在到期日支付其一名员工的工资,机械地被视为违约。因此,信用事件的发生并不一定是投资风险的证据。为了限制借给借款人、主权国家、公司等的资金损失的风险,银行会进行各种验证并评估潜在信用事件造成的潜在损失。

损失可能在多种情况下出现,例如:

- 消费者未能支付抵押贷款、信用卡或任何其他贷款。

- 公司无法偿还资产担保的固定或浮动抵押债务。

- 公司在到期时不支付其中一张发票。

- 政府债券发行人在到期时不支付息票或本金。

- 资不抵债的保险公司不支付保单义务。

- 资不抵债的银行将不会向存款人偿还资金。

- 政府为无力偿债的消费者或企业提供破产保护(《美国破产法》第 11 篇第 11 章)。

值得注意的是,这些可能是由于自然、经济和人类风险的具体化而发生的。

当借款人无法自愿或不愿意偿还债务时,就会出现信用风险。因此,如前所述,为降低贷款人的信用风险敞口,贷款人通常会对潜在借款人进行信用检查,此外可能会要求借款人购买适当的保险,例如抵押保险,或者可能会为借款人的部分资产寻求担保。借款人或第三方的担保。贷方还可以将债务证券化或将创造的资产出售给其他公司。一般来说,风险越高,与债务相关的利率就越高。从资本支出的角度来看,风险敞口的建模和测量如下所述。

金融代写|量化风险管理代写Quantitative Risk Management代考|Standardised Approach

标准化方法是指巴塞尔协议 II 下提出的一套信用风险计量技术。在这种方法下,银行必须使用外部信用评级机构的评级来量化信用风险所需的资本。与这些评级相关的风险权重总结如下。 对零售产品的索赔:这包括信用卡、透支、汽车贷款、个人理财和小企业-风险权重:75

- 由住宅财产担保的索赔-风险权重:35%

- 商业地产担保的债权-风险权重:100%

- 逾期贷款 – 超过 90 天(住宅抵押贷款除外) – 风险权重:

- 150%对于低于20%未偿金额

- 100%对于介于 20 和49%未偿金额

- 100%对于不低于50%未偿金额,但具有监督酌处权的金额减少到50%未偿金额

- 其他资产-风险权重:100%

- 现金风险权重:0%

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。