金融代写|利率建模代写Interest Rate Modeling代考| A Binomial Tree for the Ho–Lee Model

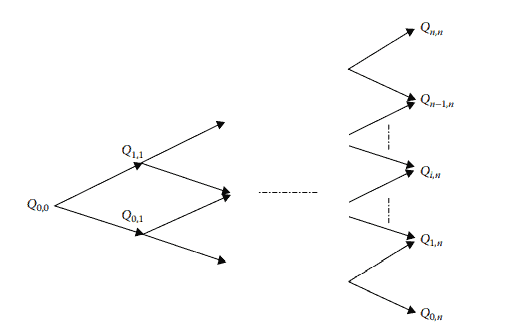

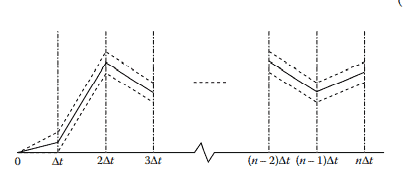

The IIo-Lee model was first presented with a binomial tree. For a Gaussian short-rate model with mean and variance of change over $(t, t+\Delta t)$ given by $$ \begin{aligned} E^{\mathbb{Q}}\left[\Delta r_t\right] &=\theta_t \Delta t \ \operatorname{VaR}\left(\Delta r_t\right) &=\sigma^2 \Delta t \end{aligned} $$ we consider a rather natural binomial tree approximation as illustrated in Figure 5.1, where, without loss of generality, the branching probabilities are uniformly one half. For notational efficiency, we let $$ r_{i, n}=r_{0,0}+\Delta t \sum_{k=1}^{n-1} \theta_k+(2 i-n) \sigma \sqrt{\Delta t}, \quad i=0,1, \ldots, n $$

Then we have a multi-period tree as shown in Figure 5.2. Before being applied to derivatives pricing, such a tree must first be calibrated to the current term structure of the interest rate. For the Ho-Lee model, we need to determine the drift, $\theta_t$, by reproducing the prices of zero-coupon bonds of all maturities. This task can be efficiently achieved with the help of the so-called Arrow-Debreu prices.

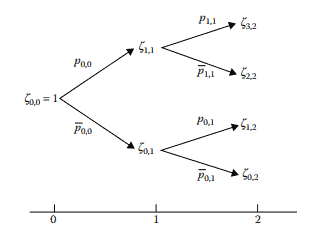

An Arrow-Debreu (1954) security is a canonical asset that has a cash flow of $\$ 1$ if a particular state (of interest rate) is realized, or nothing otherwise. The pattern of payment is shown in Figure $5.3$, where we let $Q_{i, j}$ denote the price of the security at time 0 that would pay $\$ 1$ at time $j$ if the state $i$ is realized, or nothing if otherwise.

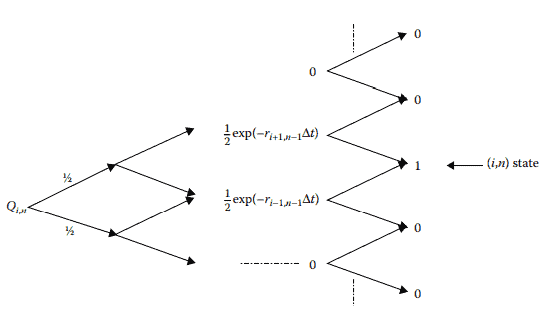

Note that a zero-coupon bond can be regarded as a portfolio of ArrowDebreu securities. By linearity, the price of the zero-coupon bond maturing in time $j$ is equal to $$ P(0, j)=\sum_{i=0}^j Q_{i, j} . $$ Given an interest-rate tree as in Figure 5.2, we can construct the ArrowDebreu tree through a forward induction process. We begin with $$ Q_{0,0}=1 . $$ The calculations of $Q_{1,1}$ and $Q_{0,1}$ are done by “expectation pricing” using the trees in Figure $5.4$, where $r_{0,0}$ is the discount rate at node $(0,0)$. Intuitively, the prices of the two Arrow-Debreu securities are given by $$ Q_{1,1}=Q_{0,1}=\frac{1}{2} \mathrm{e}^{-r_{0,0} \Delta t} $$

金融代写|利率建模代写Interest Rate Modeling代考| GENERAL MARKOVIAN MODELS

Existing short-rate models are Markovian models. A no-arbitrage shortrate model should also be derived from the HJM framework. However, this can be quite difficult. In this section, we address the opposite question: under what kind of forward-rate volatility specifications should the resulting short-rate model be a Markovian random variable? Answering this question will help us to calibrate and implement a short-rate model more efficiently. According to Equation 4.21, the short rate can be expressed as $$ r_t=f(t, t)=f(0, t)+\int_0^t\left[-\boldsymbol{\sigma}^{\mathrm{T}}(s, t) \mathbf{\Sigma}(s, t) \mathrm{d} s+\boldsymbol{\sigma}^{\mathrm{T}}(s, t) \mathrm{d} \mathbf{W}_s\right] $$

where $\mathbf{W}t$ is the $n$-dimensional Brownian motion under the risk-neutral measure, $\sigma(t, T)$ the forward-rate volatility, and $\boldsymbol{\Sigma}(t, T)$ the volatility of the $T$-maturity zero-coupon bond, given by $\boldsymbol{\Sigma}(t, T)=-\int_t^T \boldsymbol{\sigma}(t, u) \mathrm{d} u$. The stochastic differentiation of the short rate is $$ \begin{aligned} \mathrm{d} r_t=& {\left[f_t(0, t)+\int_0^t\left(-\frac{\partial}{\partial t}\left(\boldsymbol{\sigma}^{\mathrm{T}}(s, t) \boldsymbol{\Sigma}(s, t)\right) \mathrm{d} s+\frac{\partial \boldsymbol{\sigma}^{\mathrm{T}}(s, t)}{\partial t} \mathrm{~d} \mathbf{W}_s\right)\right] \mathrm{d} t } \ &+\boldsymbol{\sigma}^{\mathrm{T}}(t, t) \mathrm{d} \mathbf{W}_t \ =& {\left[f_t(t, T)\right]{T=t} \mathrm{~d} t+\boldsymbol{\sigma}^{\mathrm{T}}(t, t) \mathrm{d}t . } \end{aligned} $$ Based on Equation $5.17$ we can make the following judgment: for the shortrate model to be a Markovian process, we need the drift term, $\left[f_t(t, T)\right]{T=t}$, to be a function of a finite set of state variables that are jointly Markovian in their evolution.

To write the short rate as a function of several state variables, we introduce auxiliary functions $$ b_i(t, T)=\sigma_i(t, T) \int_t^T \sigma_i(t, s) \mathrm{d} s, \quad i=1,2, \ldots, n . $$

金融代写|利率建模代写Interest Rate Modeling代考|Monte Carlo Simulations for Options Pricing

Owing to the Markovian property of short-rate models, path simulations by Monte Carlo methods can be carried out efficiently, which is important for pricing exotic and path-dependent options. Take the pricing of the option on a zero-coupon for example. The value can be expressed as $$ V_t=E_t^{\mathbb{Q}}\left[\mathrm{e}^{-\int_t^T r_s \mathrm{~d} s}(P(T, \tau)-K)^{+}\right], \quad t<T<\tau $$ where $\mathbb{Q}$ stands for the risk-neutral measure, $r_t$ is given by Equation $5.20$, and the bond price is given by Equation 5.39. Both variables are expressed in terms of $\chi_i(t)$ and $\varphi_i(t), i=1, \ldots, n$, which evolve according to Equation 5.23. The corresponding simulation scheme for $\chi_i(t)$ and $\varphi_i(t)$ is $$ \begin{aligned} &\varphi_i(t+\Delta t)-\varphi_i(t)+\left(\sigma_i^2(t, t)-2 \kappa_i(t) \varphi_i(t)\right) \Delta t \ &\chi_i(t+\Delta t)=\chi_i(t)+\left(\varphi_i(t)-\kappa_i(t) \chi_i(t)\right) \mathrm{d} t+\sigma_i(t, t) \Delta W_i(t) \end{aligned} $$ which is simply the so-called Euler scheme. The bond option is priced by simulating many payoffs before taking an average. In Inui and Kijima (1998), the following example is considered: $$ \boldsymbol{\sigma}(t, T)=\left(\begin{array}{c} c_1 r_t^\alpha \ c_2 r_t^\beta \mathrm{e}^{-\kappa(T-t)} \end{array}\right) $$ where $c_i, i=1,2, \alpha, \beta$, and $\kappa$ are non-negative constants. It can be verified that the components of the volatility vector satisfy $$ \frac{\partial \sigma_1(t, T)}{\partial T}=0, \quad \frac{\partial \sigma_2(t, T)}{\partial T}=-\kappa \sigma_2(t, T) . $$

金融代写|利率建模代写Interest Rate Modeling代考| ON THE LOGNORMAL SPECIFICATION OF FORWARD RATES

We now explore the possibility of using the state-dependent volatility function in the HJM model. Without loss of generality, we consider the forward-rate volatility function of the form $$ \sigma(t, T)=\sigma_0(t, T) f^\alpha(t, T), $$

where $\sigma_0(t, T)$ is a deterministic function and $\alpha$ a positive exponent. In the special case, $\alpha=0$, we obtain a Gaussian model.

Similar to Avellaneda and Laurence (1999), we show that the “lognormal” model, corresponding to $\alpha=1$, blows up in finite time in the sense that a forward rate reaches infinity. This result was first obtained by Morton (1988). One can imagine that similar results may apply to the case of $\alpha>0$. Hence, volatility specification in the form of Equation $4.136$ is denied.

It suffices to show the result with a one-factor model. The no-arbitrage condition dictates that the drift must be $$ \mu(t, T)=f(t, T) \sigma_0(t, T) \int_t^T f(t, s) \sigma_0(t, s) \mathrm{d} s, $$ which depends on the entire curve of $f(t, s), t \leq s \leq T$. Consider the simplest specification of $\sigma_0(t, T)$ : $\sigma_0(t, T)=\sigma_0=$ constant. The HJM equation then becomes $$ \frac{\mathrm{d} f(t, T)}{f(t, T)}=\sigma_0 \mathrm{~d} \tilde{W}_t+\left(\sigma_0^2 \int_t^T f(t, s) \mathrm{d} s\right) \mathrm{d} t . $$ The formal solution to the above equation is $$ \begin{aligned} f(t, T) &=f(0, T) \exp \left(\sigma_0 \tilde{W}_t-\frac{\sigma_0^2}{2} t+\sigma_0^2 \int_0^t\left(\int_s^T f(s, u) \mathrm{d} u\right) \mathrm{d} s\right) \ &=f(0, T) M(t) \exp \left(\sigma_0^2 \int_0^t\left(\int_s^T f(s, u) \mathrm{d} u\right) \mathrm{d} s\right) \end{aligned} $$ where $M(t)=\exp \left(\sigma_0 \tilde{W}_t-\left(\sigma_0^2 / 2\right) t\right)$. Assume for simplicity that the initial term structure is flat, that is, $f(0, T)=f_0=$ constant.

金融代写|利率建模代写Interest Rate Modeling代考|FROM SHORT-RATE MODELS TO FORWARD-RATE MODELS

Short-rate models dominated fixed-income modeling before the emergence of the no-arbitrage framework of Heath, Jarrow, and Morton (1992), which is based on forward rates. Short-rate models can be made arbitrage free by taking appropriate drift terms, such as the Ho-Lee model and the I Iull-White model. But this is not always easy. One way to derive the correct drift term is to identify the corresponding forward-rate volatility and then to solve for the expression of the forward rates, which include the short rate as an extreme case, from the HJM equation. The focus in this section is on how to derive the corresponding forward-rate volatility in order to identify the model as a special case of the HJM framework.

Consider in general an Ito’s process for the short rate under the riskneutral measure, $\mathbb{Q}$, $$ \mathrm{d} r_t=v\left(r_t, t\right) \mathrm{d} t+\rho\left(r_t, t\right) \mathrm{d} W_t, $$ where the drift, $v\left(r_t, t\right)$, and volatility, $\rho\left(r_t, t\right)$, are deterministic functions of their arguments. Note that, for notational simplicity, we hereafter drop ” $\sim$ ” over the $\mathbb{Q}$-Brownian motion, $W_t$. Define an auxiliary function $$ g(x, t, T)=-\ln E^{\mathbb{Q}}\left[\exp \left(-\int_t^T r_s \mathrm{~d} s\right) \mid r_t=x\right] $$ We have the following result (Baxter and Rennie, 1996).

金融代写|利率建模代写Interest Rate Modeling代考|CHANGE OF MEASURES UNDER BROWNIAN FILTRATION

2.2.1 The Radon-Nikodym Derivative of a Brownian Path Consider a path of $\mathbb{P}$-Brownian motion over $(0, t)$ with discrete time stepping, $$ {W(0)=0, W(\Delta t), W(2 \Delta t), \ldots, W(n \Delta t)} $$ where $\Delta t=t / n$. With the probability ratio in mind, our immediate question is what the path probability is. The answer, unfortunately, is zero.

The implication that we cannot define the notion of the probability ratio given that the same path is realized under two different probability measures. To circumvent this problem, we first seek to calculate the probability for the Brownian motion to travel in a corridor (the so-called corridor probability), as is shown in Figure 2.5, and then we define the ratio of the corridor probabilities. The ratio of the path probabilities is finally defined through a limiting procedure. The corridor can be represented by the intervals $A_{i}=\left(x_{i}-(\Delta x / 2), x_{i}+(\Delta x / 2)\right), i=1,2, \ldots, n$, where $x_{i}=W(i \Delta t)$ and $\Delta x>0$ is a small number.

For a Brownian motion, the marginal distribution at $t_{i}=i \Delta t$ is known to be $$ f_{\mathrm{P}}(x)=\frac{1}{\sqrt{2 \pi \Delta t}} \mathrm{e}^{-(1 / 2)\left[\left(x-x_{i}\right)^{2} / \Delta t\right]} \sim N\left(x_{i}, \Delta t\right) . $$ Hence, the probability for the next step to fall in $A_{i+1}$ is $$ \begin{aligned} \operatorname{Prob}{\mathbb{P}}\left(A{i+1}\right) &=\int_{x_{i+1}-\Delta x / 2}^{x_{i+1}+\Delta x / 2} f_{\mathrm{P}}(x) \mathrm{d} x \ & \approx f_{\mathrm{P}}\left(x_{i+1}\right) \Delta x=\frac{\Delta x}{\sqrt{2 \pi \Delta t}} \mathrm{e}^{-(1 / 2)\left[\left(x_{i+1}-x_{i}\right)^{2} / \Delta t\right]} . \end{aligned} $$ Approximately, we can define the corridor probability to be $$ \prod_{i=1}^{n} \operatorname{Prob}{\mathbb{P}}\left(A{i}\right)=\left(\frac{\Delta x}{\sqrt{2 \pi \Delta t}}\right)^{n} \mathrm{e}^{-(1 / 2 \Delta t) \sum_{i=0}^{n-1}\left(x_{i+1}-x_{i}\right)^{2}} $$ Next, suppose that the same path is realized under a different marginal probability, $$ f_{\mathbb{Q}}(x)=\frac{1}{\sqrt{2 \pi \Delta t}} \mathrm{e}^{-(1 / 2)\left[\left(x-x_{i}+\gamma \Delta t\right)^{2} / \Delta t\right]} \sim N\left(x_{i}-\gamma \Delta t, \Delta t\right), \quad \forall i $$

where $\gamma$ is taken to be constant for simplicity. Then the corresponding corridor probability can be similarly obtained to be $$ \prod_{i=1}^{n} \operatorname{Prob}{\mathrm{Q}}\left(A{i}\right)=\left(\frac{\Delta x}{\sqrt{2 \pi \Delta t}}\right)^{n} \mathrm{e}^{-(1 / 2 \Delta t) \sum_{i=0}^{n-1}\left(x_{i+1}-x_{i}+\gamma \Delta t\right)^{2}} $$

The martingale representation theorem plays a critical role in the socalled martingale approach to derivatives pricing. This theorem has two important consequences. First, it leads to a general principle for derivatives pricing. Second, it implies a replication or hedging strategy of a derivative using its underlying security. We first present a simple version of the theorem based on a single Brownian filtration, $\mathcal{F}{t}=\sigma\left(W{s}, 0 \leq s \leq t\right)$. We begin with a martingale process, $M_{t}$, such that $$ \mathrm{d} M_{t}=\sigma_{t} \mathrm{~d} W_{t}, $$ and we call $\sigma_{t}$ the volatility of $M_{t}$. Theorem 2.2 (The Martingale Representation Theorem) Suppose that $N_{t}$ is a $\mathbb{Q}$-martingale process that is adaptive to $\mathcal{F}{t}$ and satisfies $E^{\mathbb{Q}}\left[N{T}^{2}\right]<$ $\infty$ for some $T$. If the volatility of $M_{t}$ is non-zero almost surely, then there exists a unique $\mathcal{F}{t}$-adaptive process, $\varphi{t}$, such that $\int_{0}^{T} \varphi_{t}^{2} \sigma_{t}^{2} \mathrm{~d} t<\infty$ almost surely, and $$ N_{t}=N_{0}+\int_{0}^{t} \varphi_{s} \mathrm{~d} M_{s}, \quad t \leq T $$ or, in differential form, $$ \mathrm{d} N_{t}=\varphi_{t} \mathrm{~d} M_{t} . $$ A sketchy proof along the lines of Steele (2000) is provided at the end of this chapter. A different proof can be found in Korn and Korn (2000).

金融代写|利率建模代写Interest Rate Modeling代考|A COMPLETE MARKET WITH TWO SECURITIES

We consider the first “complete market” in continuous time, which consists of a money market account and a risky security. The price processes for the two securities, $B_{t}$ and $S_{t}$, are assumed to be $$ \begin{aligned} \mathrm{d} B_{t} &=r_{t} B_{t} \mathrm{~d} t, & B_{0} &=1, \ \mathrm{~d} S_{t} &=S_{t}\left(\mu_{t} \mathrm{~d} t+\sigma_{t} \mathrm{~d} W_{t}\right), & S_{0} &=S_{0} . \end{aligned} $$ Here, the volatility of the risky asset is $\sigma_{t} \neq 0$ almost surely, and the short rate, $r_{t}$, can be stochastic. Denote the discounted price of the risky asset as $Z_{t}=B_{t}^{-1} S_{t}$, which can be shown to follow the process $$ \begin{aligned} \mathrm{d} Z_{t} &=Z_{t}\left(\left(\mu_{t}-r_{t}\right) \mathrm{d} t+\sigma_{t} \mathrm{~d} W_{t}\right) \ &=Z_{t} \sigma_{t} \mathrm{~d}\left(W_{t}+\int_{0}^{t} \frac{\left(\mu_{s}-r_{s}\right)}{\sigma_{s}} \mathrm{~d} s\right) \end{aligned} $$ By introducing $$ \gamma_{t}=\frac{\mu_{t}-r_{t}}{\sigma_{t}} $$ which is $\mathcal{F}{t}$-adaptive, and by defining a new measure, $\mathbb{Q}$, according to Equation 2.36, we have $$ \tilde{W}{t}=W_{t}+\int_{0}^{t} \gamma_{s} \mathrm{~d} s $$ which is a $\mathbb{Q}$-Brownian motion. In terms of $\tilde{W}{t}, Z{t}$ satisfies $$ \mathrm{d} Z_{t}=\sigma_{t} Z_{t} \mathrm{~d} \tilde{W}_{t} $$ which is a lognormal $\mathbb{Q}$-martingale. Recall that in the binomial model for option pricing, we also derived the martingale measure for the underlying security.

$E^{\mathbb{P}}\left[M_{t} \mid \mathcal{F}{s}\right]=M{s}, \quad \forall s \leq t$. The martingale properties are associated with fair games in investments or speculations. Let us think of $M_{t}-M_{s}$ as the profit or loss (P\&L) of a gamble between two parties over the time period $(s, t)$. Then the game is considered fair if the expected P\&L is zero. Daily life examples of fair games include the coin tossing game and futures investments in financial markets. In mathematics, there are plenty of examples as well. In fact, we have already seen several of them so far, of which we remind readers below. Example $1.4$

The simple random walk, $X_{n}$, is a martingale because $E\left[\left|X_{n}\right|\right]<$ $n \sqrt{\Delta t}$ and $E\left[X_{n} \mid \mathcal{F}{m}\right]=X{m}, m \leq n$

A $\mathbb{P}$-Brownian motion, $W_{t}$, is a martingale by definition.

The stochastic integral $X_{t}=\int_{0}^{t} f(u) \mathrm{d} W_{u}$ is a martingale, since $$ \begin{aligned} E^{\mathbb{P}}\left[X_{t} \mid \mathcal{F}{s}\right] &=E^{\mathbb{P}}\left[\int{0}^{s}+\int_{s}^{t} f(u) \mathrm{d} W_{u} \mid \mathcal{F}{s}\right] \ &=\int{0}^{s} f(u) \mathrm{d} W_{u}=X_{s}, \quad \forall s \leq t \end{aligned} $$ Here, we have applied the first property of stochastic integrals (see page 11).

The process $M_{t}=\exp \left(\int_{0}^{t} \sigma_{s} \mathrm{~d} W_{s}-\frac{1}{2} \sigma_{s}^{2} \mathrm{~d} s\right)$ is an exponential martingale. In fact, using the Ito’s lemma, we can show that $$ \mathrm{d} M_{t}=\sigma_{t} M_{t} \mathrm{~d} W_{t} $$ which is an Ito’s process without drift. It follows that $$ M_{t}=M_{s}+\int_{s}^{t} M_{u} \sigma_{u} \mathrm{~d} W_{u} $$ Based on the conclusion of the last example, we know that $M_{t}$ is a martingale.

We emphasize here that an Ito’s process is a martingale process if and only if its drift term is zero. Finally, we present two additional examples.

金融代写|利率建模代写Interest Rate Modeling代考|A Motivating Example

Consider the simplest option-pricing model with an underlying asset following a one-period binomial process, as depicted in Figure 2.1. In Figure $2.1,0 \leq p \leq 1$ and $\bar{p}=1-p$. The option’s payoffs at time $1, f\left(S_{u}\right)$ and $f\left(S_{d}\right)$, are given explicitly, and we want to determine $f(S)$, the value of the option at time 0 . Without loss of generality, we assume that there is a zero interest rate in the model. To avoid arbitrage, we must impose the order $S_{d} \leq S \leq S_{u}$. We call $\mathbb{P}={p, \bar{p}}$ the objective measure of the underlying process. It may be tempting to price the option by expectation under $\mathbb{P}$ : $$ \begin{aligned} f(S) &=E^{\mathbb{P}}\left[f\left(S_{1}\right)\right] \ &=p f\left(S_{u}\right)+\bar{p} f\left(S_{d}\right) \end{aligned} $$ However, except for a special $p$, the above price generates arbitrage and thus is wrong. To see that, we replicate the payoff of the option at time $l$ using a portfolio of the underlying asset and a cash bond, with respective numbers of units, $\alpha$ and $\beta$, such that, at time 1 , $$ \begin{aligned} &\alpha S_{u}+\beta=f\left(S_{u}\right) \ &\alpha S_{d}+\beta=f\left(S_{d}\right) \end{aligned} $$

Solving for $\alpha$ and $\beta$, we obtain $$ \begin{aligned} \alpha &=\frac{f\left(S_{u}\right)-f\left(S_{d}\right)}{S_{u}-S_{d}}, \ \beta &=\frac{S_{u} f\left(S_{d}\right)-S_{d} f\left(S_{u}\right)}{S_{u}-S_{d}} . \end{aligned} $$ Equation $2.2$ implies that the time-1 values of the portfolio and option are identical. To avoid arbitrage, their values at time 0 must be identical as well, ${ }^{*}$ which yields the arbitrage price of the option at time 0 : $$ \begin{aligned} f(S) &=\alpha S+\beta \ &=q f\left(S_{u}\right)+\bar{q} f\left(S_{d}\right) \ &=E^{\mathbb{Q}}\left[f\left(S_{1}\right)\right], \end{aligned} $$ where $\mathbb{Q}={q, \bar{q}}$, and $$ q=\frac{S-S_{d}}{S_{u}-S_{d}}, \quad \bar{q}=1-q $$ is a different set of probabilities. Note that Equation $2.4$ gives the noarbitrage price of the option. Any other price will induce arbitrage to the market. Hence, the expectation price, in Equation 2.1, is correct only if $p=q$. In fact, ${q, \bar{q}}$ is the only set of probabilities that satisfies $$ S=q S_{u}+\bar{q} S_{d}=E^{\mathbb{Q}}\left(S_{1}\right) . $$

金融代写|利率建模代写Interest Rate Modeling代考|Binomial Trees and Path Probabilities

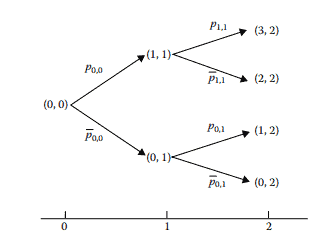

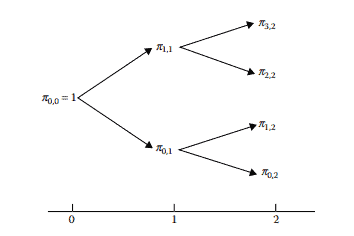

Let us move one step further and consider the binomial tree model up to two time steps, as shown in Figure 2.2, where each pair of numbers represents a state (which can be associated with the price of an asset if necessary). Out of each state at time $j$, two possible states are generated at time $j+1$. Hence, we have $2^{j}$ states at time $j$, starting with a single state at time 0 . The branching probabilities for reaching the next two states from one state, $(i, j)$, are $p_{i, j} \in[0,1]$ and $\bar{p}{i, j}=1-p{i, j}$, respectively. The collection of branching probabilities, $\mathbb{P}=\left{p_{i, j}, \bar{p}{i, j}\right}$, is again called a measure. As is shown in Figure 2.2, there are two paths over the time horizon from 0 to 1 , whereas there are four paths over the time horizon from 0 to 2 . The corresponding path probabilities for the horizon from 0 to 1 are $$ \pi{0,1}=\bar{p}{0,0} \quad \text { and } \quad \pi{1,1}=p_{0,0}, $$

whereas for the horizon from 0 to 2 , they are $$ \pi_{0,2}=\bar{p}{0,0} \bar{p}{0,1}, \pi_{1,2}=\bar{p}{0,0} p{0,1}, \pi_{2,2}=p_{0,0} \bar{p}{1,1} \text {, and } \pi{3,2}=p_{0,0} p_{1,1} \text {. } $$ The path probabilities can also be marked in a binomial tree as is shown in Figure 2.3.

Consider now another set of branching probabilities, $\mathbb{Q}=\left{q_{i, j}, \bar{q}{i, j}=\right.$ $\left.1-q{i, j}\right}$, for the same tree. The corresponding path probabilities are $$ \pi_{0,1}^{\prime}=\bar{q}{0,0} \quad \text { and } \quad \pi{1,1}^{\prime}=q_{0,0} $$ up to time 1 , and $$ \pi_{0,2}^{\prime}=\bar{q}{0,0} \bar{q}{0,1}, \pi_{1,2}^{\prime}=\bar{q}{0,0} q{0,1}, \pi_{2,2}^{\prime}=q_{0,0} \bar{q}{1,1} \text {, and } \pi{3,2}^{\prime}=q_{0,0} q_{1,1} $$ up to time 2. Suppose that the $\mathbb{P}$-probability of paths $\pi_{i, j} \neq 0$ for all $i, j$. We then can define the ratio of path probabilities as follows: $$ \zeta_{i, j}=\frac{\pi_{i, j}^{\prime}}{\pi_{i, j}} . $$

金融代写|利率建模代写Interest Rate Modeling代考|Simple Random Walks

Simple random walks are discrete time series, $\left{X_{i}\right}$, defined as $$ \begin{aligned} X_{0} &=0, \ X_{n+1} &= \begin{cases}X_{n}-\sqrt{\Delta t}, & p=\frac{1}{2} \ X_{n}+\sqrt{\Delta t}, & 1-p=\frac{1}{2}\end{cases} \end{aligned} $$ where $\Delta t>0$ stands for the interval of time for stepping forward. One can verify that $\left{X_{i}\right}$ have the following properties:

The increment of $X_{n+1}-X_{n}$ is independent of $\left{X_{i}\right}, \forall i \leq n$.

$E\left[X_{n} \mid X_{m}\right]=X_{m}, m \leq n$.

$\operatorname{Var}\left[X_{n} \mid X_{m}\right]=(n-m) \Delta t, m \leq n$. An interesting feature of the simple random walk is the linearity of $X_{i}$ ‘s variance in time: given $X_{0}$, the variance of $X_{i}$ is equal to $i \Delta t$, the time it takes the time series to evolve from $X_{0}$ to $X_{i}$.

Out of the simple Brownian random walk, we can construct a continuous-time process through linear interpolation: $$ \bar{X}(t)=X_{i}+\frac{t-i \Delta t}{\Delta t}\left(X_{i+1}-X_{i}\right), \quad t \in[i \Delta t,(i+1) \Delta t] $$ We are interested in the limiting process of $\bar{X}(t)$ as $\Delta t \rightarrow 0$, in the hope that the limit remains a meaningful stochastic process. The next theorem confirms just that.

A continuous stochastic process is a collection of real-valued random variables, ${X(t, \omega), 0 \leq t \leq T}$ or $\left{X_{t}(\omega), 0 \leq t \leq T\right}$, that are defined on a probability space $(\Omega, \mathcal{F}, \mathbb{P})$. Here $\Omega$ is the collection of all $\omega$ s, which are so-called sample points, $\mathcal{F}$ the smallest $\sigma$-algebra that contains $\Omega$, and $\mathbb{P}$ a probability measure on $\Omega$. Each random outcome, $\omega \in \Omega$, corresponds to an entire time series $$ t \rightarrow X_{t}(\omega), \quad t \in T $$ which is called a path of $X_{t}$. In view of Equation 1.7, we can regard $X_{t}(\omega)$ as a function of two variables, $\omega$ and $t$. For notational simplicity, however, we often suppress the $\omega$ variable when its explicit appearance is not necessary.

In the context of financial modeling, we are particularly interested in the Brownian motion introduced earlier. Its formal definition is given below.

Definition 1.1 A Brownian motion or a Wiener process is a realvalued stochastic process, $W_{t}$ or $W(t), 0 \leq t \leq \infty$, that has the following properties:

$W(0)=0$.

$W(t+s)-W(t)$ is independent of ${W(u), 0 \leq u \leq t}$.

For $t \geq 0$ and $s>0$, the increment $W(t+s)-W(t) \sim N(0, s)$.

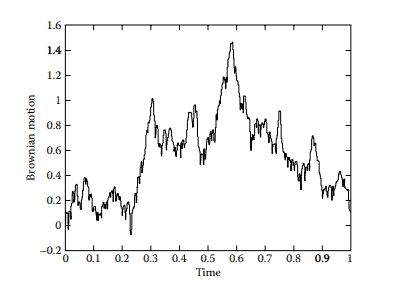

$W(t)$ is continuous almost surely (a.s.). Here $N(0, s)$ stands for a normal distribution with mean zero and variance s. Note that in some literature, property 4 is not part of the definition, as it can be proved to be implied by the first three properties (Varadhan, $1980 \mathrm{a}$ or Ikeda and Watanabe, 1989). A sample path of $W(t)$ is shown in Figure $1.1$, which is generated with a step size of $\Delta t=2^{-10}$.

Brownian motion plays a major role in continuous time stochastic modeling in physics, engineering and finance. In finance, it has been used to model the random behavior of asset returns. Several major properties of Brownian motion are listed below.

Stochastic calculus considers the integration and differentiation of general $\mathcal{F}{t}$-adaptive functions. The purpose of developing such a stochastic calculus is to model financial time series (with random dynamics) with either integral or differential equations. According to Lemma 1.1, a Brownian motion, $W(t)$, is nowhere differentiable in the usual sense of differentiation for deterministic functions. To define differentials of stochastic processes in a proper sense, we must first study the notion of stochastic integrals. Stochastic integrals can be defined for functions in the square-integrable space, $H^{2}[0, T]=L^{2}(\Omega \times[0, T], \mathrm{d} \mathbb{P} \times \mathrm{d} t)$, which is defined to be the collection of functions satisfying $$ E\left[\int{0}^{T}|f(t, \omega)|^{2} \mathrm{~d} t\right]<\infty $$ Note that, without indicated otherwise, $E[\cdot]$ means $E^{\mathbb{P}}[\cdot]$, the unconditional expectation under $\mathbb{P}$. The definition consists of a three-step procedure. First, we make the definition for elementary or piecewise constant functions in an intuitive way. Second, we define the integrals of a bounded continuous function as a limit of integrals of elementary functions. Finally, we define the integral of a general square-integrable function as a limit of integrals of bounded continuous functions. The key in this three-step procedure is of course to ensure the convergence of the limits in $L^{2}(\Omega, \mathcal{F}, \mathbb{P})$, the Hilbert space of random variables satisfying $$ E\left[X^{2}(\omega)\right]<\infty $$ This definition approach is taken by Oksendal (1992). Alternative treatments of course also exist; see, for example, Mikosch (1998).

金融代写|利率建模代写Interest Rate Modeling代考|Discretization of Forward Rate Process

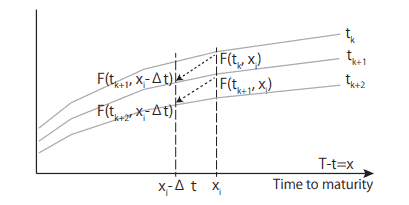

We recall the forward rate process in the H.JM model as $$ \begin{aligned} f(t, T)=& f(0, T)+\int_{0}^{t}\left{-\sigma(s, T) v(s, T)+\sigma(s, T) \varphi_{s}\right} d s \ &+\int_{0}^{t} \sigma(s, T) d W_{s} \end{aligned} $$ where $W_{t}$ is a $d$-dimensional P-Brownian motion. The HJM model is called Gaussian if $\sigma(t, T)$ is a deterministic function of $t$ and $T$. In this book, we always assume that volatility $\sigma(t, T)$ is deterministic and continuous with respect to $t$ and $T$. Then, $v(t, T)$ is also deterministic and continuous. In the following, the market price of risk is assumed to be constant. The validity of the constancy assumption will be examined in the context of risk management in Chapter $7 .$ Data observation Denoting the market price of risk as a constant $\varphi$, the above forward rate process is expressed by $$ \begin{aligned} f(t, T)=& f(0, T)+\int_{0}^{t}{-\sigma(s, T) v(s, T)+\sigma(s, T) \varphi} d s \ &+\int_{0}^{t} \sigma(s, T) d W_{s} . \end{aligned} $$ Next, we specify a historical dataset as follows. Let a time interval $\Delta t>0$ be fixed, and $\left{t_{k}\right}_{k=1, \cdots, J+1}$ be a sequence of observation dates such that $t_{1}=0$ and $t_{k+1}-t_{k}=\Delta t$, where $J+1$ is the number of observation times. We denote the time length to a maturity $T$ from $t$ by $x=T-t$. For an integer $n \geq d$, $x_{1}, \cdots, x_{n}$ denotes a sequence of time lengths to maturity.

Typically, we observe the instantaneous forward rate $F\left(t_{k}, x_{i}\right)$ with respect to fixed $x_{i}$. Fig. $6.1$ illustrates an example of forward rate curves observed at $t_{k}, t_{k+1}$, and $t_{k+2}$, showing $F\left(t_{k}, x_{i}\right), F\left(t_{k+1}, x_{i}-\Delta t\right)$, and so on. We assume that the dynamics of these observations follow equation (6.2).

金融代写|利率建模代写Interest Rate Modeling代考|Estimation of Market Price of Risk

We recall the volatility structure associated with PCA in Section 4.3. A sample covariance matrix $V$ is defined by $$ \begin{aligned} V_{i j}=& \frac{1}{\Delta t} \operatorname{Cov}\left(F\left(t_{k}+\Delta t, x_{i}-\Delta t\right)-F\left(t_{k}, x_{i}\right)\right.\ &\left.F\left(t_{k}+\Delta t, x_{j}-\Delta t\right)-F\left(t_{k}, x_{j}\right)\right) ; \quad i, j=1, \cdots, n . \end{aligned} $$ We assume that $V$ has rank $d \leq n$. By the argument in Appendix $\mathrm{B}$, the covariance matrix is decomposed into $V_{i j}=\sum_{l=1}^{d} e_{i}^{l} \rho_{l}^{2} e_{j}^{l}$ for $i, j \leq n$, where $\rho_{l}^{2}$ is the lth eigenvalue, and $e^{l}=\left(e_{1}^{l}, \cdots, e_{n}^{l}\right)^{T}$ is the $l$ th principal component of the covariance for $l=1, \cdots, d$. We always assume that $$ e_{1}^{l}>0, \quad \rho_{l}>0 ; \quad l=1, \cdots, d $$ This assumption is significant in the interpretation of the meaning of the market price of risk in Sections $6.4$ and 6.5. Recall the equation (B.4), that is, that the principal components $e^{1}, \cdots, e^{d}$ form an orthonormal set. Thus, $$ \sum_{i=1}^{n} e_{i}^{l} e_{i}^{h}=\delta_{l h} \quad ; \quad l, h=1, \cdots, d $$

金融代写|利率建模代写Interest Rate Modeling代考|Market Price of Risk: State Space Setup

This section introduces another method to estimate the market price of risk: working in a state space.

Denoting the market price of risk by $\varphi^{\prime}=\left(\varphi_{1}^{\prime}, \cdots, \varphi_{d}^{\prime}\right)^{T}$, we return to the discretization as equation (6.13), which we reproduce below: $$ \Delta F_{i}\left(t_{k}\right)=-\sigma_{0 i} v_{0 i} \Delta t+\sigma_{0 i} \varphi^{\prime} \Delta t+\sqrt{\Delta t} \sigma_{0 i} W_{1} ; i=1, \cdots, n, k=1, \cdots, J $$ We remark that the volatility is assumed to be determined by a principal component. Our objective here is to directly obtain $\varphi^{\prime}$ from the above equations. We denote by $\epsilon\left(\varphi^{\prime}\right)$ the sum of the squared difference between each side of equation $(6.26)$ in the time series and cross sections, neglecting the random part, such that $$ \epsilon\left(\varphi^{\prime}\right)=\frac{1}{J} \sum_{k=1}^{J} \sum_{i=1}^{n}\left{\Delta F_{i}\left(t_{k}\right)+\left(\sigma_{0 i} v_{0 i}-\sigma_{0 i} \varphi^{\prime}\right) \Delta t\right}^{2} $$ Let $\varphi^{\prime}$ be the solution that minimizes $\epsilon\left(\varphi^{\prime}\right)$. We call this setting a state space setup, and call that used in the previous section a $P C A$ setup to distinguish between the two approaches. We note the implications of both definitions below.

$\varphi$ is the solution that minimizes $\theta_{l}\left(\varphi_{l}\right)$ in equation $(6.19)$ in the principal component space, and also is the maximum likelihood estimate.

$\varphi^{\prime}$ is the solution that minimizes $\epsilon\left(\varphi^{\prime}\right)$ of equation $(6.27)$ in the state space.

金融代写|利率建模代写Interest Rate Modeling代考|LIBOR Market Model

The LIBOR market model was introduced by Miltersen et al. (1997), Brace et al. (1997; hereinafter, BGM), Musiela and Rutkowski (1997), and Jamshidian $(1997)$. The notable points of this model are listed here:

The model has positive LIBOR.

The model admits an arbitrary deterministic volatility structure.

The price formulae of a caplet and a floorlet are derived so as to be consistent with the corresponding Black’s price.

An approximated price formula for a swaption is derived. From these, the LIBOR market model has a usability advantage in calibration, and so it is widely applied as a standard model for derivatives pricing. As a particular example, the BGM model is the most well-known type of LIBOR market model, and is built in the HJM framework. The BGM approach requires a kind of differentiability for LIBOR volatility. It is impossible to satisfy this smoothness in practice because the volatility cannot be constructed except as a piecewise continuous, but not necessarily smooth, function. Because of this, the BGM model is not strictly supported in the HJM framework. For more advanced study of this problem, see Yasuoka (2001, 2013b).

At one end of the spectrum of models, the approaches by Musiela and Rutkowski (1997) and Jamshidian (1997) stand on a martingale pricing theory, with no theoretical imperfections. However, their models are constructed under a risk-neutral measure without referring to the real-world measure.

In this section and the next, we introduce the LIBOR market model as described by Jamshidian (1997). Because the topic of this book is risk management, pricing of derivatives is not addressed here at length. For a more advanced treatment of pricing, readers are recommended to consult Brigo and Mercurio (2007) or Gatarek et al. (2007).

Similarly to the argument for the HJM model, when the LIBOR and bond prices are represented under a risk-neutral measure, we call the resulting system a risk-neutral model. When, instead, they are represented under $\mathbf{P}$, the resulting system is referred to as a real-world model. Strict definitions of these terms will be given later.

金融代写|利率建模代写Interest Rate Modeling代考|Existence of LIBOR Market Model

The existence of the LIBOR model is shown in the following theorem. Theorem 5.2.1 For arbitrary deterministic volatility $\lambda_{i}(t), i=1, \cdots, n-1$, the LIBOR market model exists.

The LIBOR model can be constructed under any of several risk-neutral measures. Applying this, we will show the existence of the LIBOR model under the real-world measure in the next section, and show how the models are implied under other measures in Sections $5.4$ and $5.5$ of this chapter. It is thought that this approach is the simplest method of constructing the LIBOR market model for practical use. Therefore, we here only sketch Jamshidian’s LIBOR market model under a forward measure, omitting the proof.

Let each of $\lambda_{i}(t)$ be an arbitrary deterministic function in $t$ for $i=1, \cdots, n-$

Consider the following equation: $$ \frac{d L_{i}(t)}{L_{i}(t)}=\sum_{j=i+1}^{n-1} \frac{\delta_{j} L_{j}(t) \lambda_{i}(t) \lambda_{j}(t)}{1+\delta_{j} L_{j}} d t+\lambda_{i}(t) d Z_{t} $$ Here, $Z_{t}$ is a $d$-dimensional Brownian motion with respect to a measure $\mathbf{Q}(\sim$ $\mathbf{P})$. With this setup, the following proposition is given in Jamshidian ( 1997 , Corollary 2.1).

Proposition 5.2.2 The equation (5.4) admits a unique positive solution for an arbitrary initial condition $L_{i}(0)>0$ for all i. Further, $Y_{i}(t)=(1+$ $\left.\delta_{i} L_{i}(t)\right) \cdots\left(1+\delta_{i} L_{n-1}(t)\right)$ is a $\mathbf{Q}$-martingale. Let $B_{n}(t)$ be an arbitrary bond price process such that $B_{n}\left(T_{n}\right)=1$ and $$ B_{n}\left(T_{i}\right)=\frac{1}{\prod_{j=i}^{n-1}\left(1+\delta_{j} L_{j}\left(T_{j}\right)\right)} $$ at each $T_{i}$. Accordingly, we define $B_{i}(t)$ for $i<n$ by $$ \frac{B_{i}(t)}{B_{n}(t)}=\prod_{j=i}^{n-1}\left(1+\delta_{j} L_{j}(t)\right) $$ From these, we see that $B_{i}\left(T_{i}\right)=1$ and the relation (5.2) is satisfied for all $i$. By Proposition 5.2.2, $\prod_{j=i}^{n-1}\left(1+\delta_{j} L_{j}(t)\right)$ is a Q-martingale for every $i$. Hence $B_{i}(t) / B_{n}(t)$ is a Q-martingale for all $i$.

Along these lines, $\mathbf{Q}$ is a $B_{n}$ numéraire measure and is referred to as a forward measure. As a result, the bond market $\mathcal{B}$ is arbitrage-free from Theorem $3.2 .2$

金融代写|利率建模代写Interest Rate Modeling代考|LIBOR Market Model under a Real-world Measure

Within the same setting as in Sections $5.1$ and 5.2, we give a definition of the LMRW and show the existence of the model, following Yasuoka (2013a).

Definition 5.3 The bond market $\mathcal{B}$ is called the $L M R W$ when the following conditions are satisfied.

The LIBOR processes $L_{i}, i=1, \cdots, n$, with $L_{i}(t)>0$, are represented under the real-world measure $\mathbf{P}$ such that each volatility $\lambda_{i}(t)$ and the market price of risk $\varphi_{t}$ are deterministic in $t$.

The bond market $\mathcal{B}$ is arbitrage-free; here this means that $B_{i}(t) \in \mathcal{B}, i=$ $1, \cdots, n$ and the state price deflator $\xi_{t}$ are positive Ito processes represented under $\mathbf{P}$.

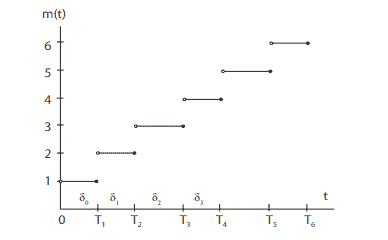

For this, we define a left-continuous function $m(t)$ by $m(t)=j$, while $t \in$ $\left(T_{j-1}, T_{j}\right]$. Succinctly, $m(t)$ represents the index of the next maturity date $.$ Examination of Fig. $5.1$ may help to see the features of $m(t)$.

To show the existence of the LMRW, it is sufficient to give the simplest example for arbitrarily given volatility $\lambda$ and market price of risk $\varphi$. For this, we define a process $\bar{\mu}(t)$ by $\bar{\mu}(t)=\bar{\mu}\left(T_{m(t)}\right)$ such that $$ \bar{\mu}\left(T_{i}\right)=\frac{1}{\delta_{i-1}} \log \left{1+\delta_{i-1} L_{i-1}\left(T_{i-1}\right)\right} $$ at each time $T_{i}$. Specifically, $\bar{\mu}(t)$ represents the yield for the shortest maturity bond, with the next maturity $T_{m(t)}$. As a consequence, $\bar{\mu}(t)$ is constant on each period $\left(T_{i-1}, T_{i}\right], i=1, \cdots, n$.

Let $\varphi_{t}$ be an arbitrarily given market price of risk such that $\varphi_{l}$ is an $\mathbf{R}^{d}-$ valued deterministic function with $$ \int_{0}^{T}\left|\varphi_{t}\right|^{2} d s<\infty $$ Let $\lambda_{i}(t), i=1, \cdots, n$ be deterministic volatilities. We set $\chi_{i}(t)$ as $$ \chi_{i}(t)=\frac{\lambda_{i}(t) \delta_{i} L_{i}(t)}{1+\delta_{i} L_{i}(t)} ; i=1, \cdots, n . $$ Consider the following equation with the initial LIBOR $L_{i}(0)>0$, $$ \frac{d L_{i}(t)}{L_{i}(t)}=\left{\lambda_{i}(t) \sum_{j=m(t)}^{i} \chi_{j}(t)+\lambda_{i}(t) \varphi_{t}\right} d t+\lambda_{i}(t) d W_{t} $$ for $i=1, \cdots, n$. It is known that the solution $L_{i}(t)$ exists uniquely and $L_{i}(t)>$ 0 . We assume that bond price processes $B_{i}(t), i=1, \cdots, n$ are Ito processes with initial values $B_{0}(0)=1$ and $$ B_{i}(0)=\prod_{j=0}^{i-1}\left(1+\delta_{j} L_{j}(0)\right)^{-1} $$ such that $$ \frac{d B_{i}(t)}{B_{i}(t)}=\left{\bar{\mu}(t)-\sum_{j=m(t)}^{i-1} \chi_{j}(t) \varphi_{t}\right} d t-\sum_{j=m(t)}^{i-1} \chi_{j}(t) d W_{t} . $$ Under this setup, we give the following theorem, which shows the existence of the LMRW.

\frac{d L_{i}(t)}{L_{i}(t)}=\left{\lambda_{i}(t) \sum_{j=m(t)}^{i} \chi_{ j}(t)+\lambda_{i}(t) \varphi_{t}\right} d t+\lambda_{i}(t) d W_{t}\frac{d L_{i}(t)}{L_{i}(t)}=\left{\lambda_{i}(t) \sum_{j=m(t)}^{i} \chi_{ j}(t)+\lambda_{i}(t) \varphi_{t}\right} d t+\lambda_{i}(t) d W_{t} 为了一世=1,⋯,n. 据了解,解决方案大号一世(吨)唯一存在并且大号一世(吨)>0 . 我们假设债券价格过程乙一世(吨),一世=1,⋯,n是具有初始值的 Ito 过程乙0(0)=1和

乙一世(0)=∏j=0一世−1(1+dj大号j(0))−1这样

\frac{d B_{i}(t)}{B_{i}(t)}=\left{\bar{\mu}(t)-\sum_{j=m(t)}^{i-1 } \chi_{j}(t) \varphi_{t}\right} d t-\sum_{j=m(t)}^{i-1} \chi_{j}(t) d W_{t} 。\frac{d B_{i}(t)}{B_{i}(t)}=\left{\bar{\mu}(t)-\sum_{j=m(t)}^{i-1 } \chi_{j}(t) \varphi_{t}\right} d t-\sum_{j=m(t)}^{i-1} \chi_{j}(t) d W_{t} 。 在这种设置下,我们给出了以下定理,它表明了 LMRW 的存在。

金融代写|利率建模代写Interest Rate Modeling代考|The Hull–White Model

In the early days, many stochastic models were introduced to describe the dynamics of the short rate. As examples, see Cox et al. (1985; hereinafter,CIR), Ho and Lee (1986), Hull and White (1990), and Vasicek (1977), among others. A strong point of these models is their parsimoniousness. Additionally, these models are described by affine term structures. For details of affine models, readers are recommended to consult Duffie and Kan (1996), Björk $(2004)$, or Munk (2011).

It is known that the Ho-Lee model and the Hull-White model are special cases of the Gaussian HJM model. The Hull-White model, in particular, is one of the most popular models in many financial institutions. Following along these lines, this section introduces the Hull-White model as a special case of the HJM model. Short rate process Let us consider a one-dimensional process of the short rate $r(t)$ represented by $$ d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t} $$ where $W_{t}$ is a one-dimensional Brownian motion under the real-world measure $\mathbf{P} ; \kappa$ and $\sigma$ are positive constants; $\theta(t)$ is a positive process; and $\varphi_{t}$ denotes the market price of risk.

It is empirically observed that the volatility of long-term interest rates is less than that of short term rates, reflecting a general phenomenon referred to as mean reversion. To model this feature, the rate at which $r(t)$ reverts to $\theta(t)$ is the speed $\kappa$, called the mean reversion rate.

The savings account $B_{t}=\exp \left{\int_{0}^{t} r(s) d s\right}$ is taken as a numéraire. We set $Z_{t}=\int_{0}^{t} \varphi_{s} d s+W_{t}$. By the Girsanov theorem, there exists a risk-neutral measure $\mathbf{Q}$ equivalent to $\mathbf{P}$ such that $Z_{t}$ is a Brownian motion under $\mathbf{Q}$. From these, the short rate $r(t)$ is represented under $\mathbf{Q}$ as $$ d r(t)=\kappa(\theta(t)-r(t)) d t+\sigma d Z_{t} $$ It is known that the price of a zero-coupon bond with maturity $T$ is given by $$ B(t, T)=\exp {-a(t, T)-b(T-t) r(t)} $$

金融代写|利率建模代写Interest Rate Modeling代考|VaR Computed in the Real-world

This section studies the reason that the VaR should be computed using a real-world model. For this purpose, the valuation of the VaR depends on the choice of measure. We use the following simple example to illustrate this. For simplicity, we assume a null discount rate in the following argument (i.e. the forward price is equal to the present price).

Suppose a binary bond with expiry at time $T$ and with payoff $X$ at $T$ is given as follows. $$ \left{\begin{array}{l} \text { If } L>5 \% \text { at } T, \text { then } X=0 \ \text { If } L \leq 5 \% \text { at } T, \text { then } X=1.01, \end{array}\right. $$ where $L$ indicates the 6 -month LIBOR at $T$. Succinctly, the payoff is determined by the level of the 6 -month LIBOR at the expiry date.

The price of this security is computed by using some interest rate model under some risk-neutral measure $\mathbf{Q}$. For the model, we assume the probability distribution of $L$ as $$ \left{\begin{array}{r} \mathrm{Q}(L>5 \%)=0.09 \% \ \mathbf{Q}(L \leq 5 \%)=99.01 \% \end{array}\right. $$ With this distribution, the arbitrage price of this bond at $t=0$ is calculated by $$ (1.01 \times 0.9901+0 \times 0.0009) \times 1=1.00 $$ because of the assumption of a null discount rate. We buy this bond at price $1.00$. Let us valuate the $99 \% \mathrm{VaR}$ of this bond for holding period $T$. We can sell this for the price $1.01$ at time $T$ at a probability of more than $99 \%$. The $99 \% \mathrm{VaR}$ is valuated as the profit of $-0.01(=1.00-1.01)$ under Q.

Next, we assume that historical observation estimates for the 6-month LIBOR are $$ \left{\begin{array}{l} \mathbf{P}(L>5 \%)=2 \% \ \mathbf{P}(L \leq 5 \%)=98 \% \end{array}\right. $$

金融代写|利率建模代写Interest Rate Modeling代考|Estimation of the Market Price of Risk

In empirical analysis concerning the term structure of interest rates, we are observing historical data under the real-world measure. To give an example, when we use the Hull-White model, the dynamics of the short rate is described from equation $(4.41)$ as $$ d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t} $$ To calibrate this model such that this equation explains the historical dynamics of the short rate, we must estimate the parameters $\sigma$ and $\kappa$ and the market price of risk $\varphi_{t}$. In this way, we inevitably estimate $\varphi_{t}$ as part of fitting any interest rate model with the historical dynamics of the interest rates.

Along these lines, there are many studies on estimating the market price of risk in the field of economics. Some papers in this vein are Ahn and Gao (1999), Cheridito et al. (2007), Cochrane and Piazzesi (2010), De Jong (2000), and Duffee (2002). However, there are few papers that explicitly describe the method used in estimating the market price of risk in short rate models. It is even more difficult to find such papers that work with forward rate models. In this section, we briefly describe three approaches to estimating the market price of risk in short rate models. For a more advanced treatment of this subject, we study theoretical methods for estimating the market price of risk in the forward rate model from Chapter $6 .$

d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t}d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t} 在哪里在吨是真实世界测量下的一维布朗运动磷;ķ和σ是正常数;θ(吨)是一个积极的过程;和披吨表示风险的市场价格。

d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t}d r(t)=\kappa\left{\theta(t)-r(t)+\frac{\sigma}{\kappa} \varphi_{t}\right} d t+\sigma d W_{t} 为了校准这个模型,使这个方程能够解释短期利率的历史动态,我们必须估计参数σ和ķ和风险的市场价格披吨. 这样,我们不可避免地估计披吨作为拟合任何利率模型与利率历史动态的一部分。

We introduced a bond market $\mathcal{B}$ in Chapter 3 that did not admit a term structure of interest rates. If, instead, we assume a term structure in the bond market, it becomes possible to relate the bond price to the interest rate. We represent the dynamics of bond price by a stochastic process and use this to specify the corresponding interest rates. Such a system is referred to as a term structure model of interest rates (or put simply, an interest rate model). A model specified by the dynamics of a short rate is referred to as a short rate model. A model specified by the dynamics of forward rates is referred to as a forward rate model. For management of interest rate risk, it is better to suppose various types of changes in the yield curve, and specifically to suppose changes in the forward rates. Because of this, the forward rate model is more useful in risk management than the short rate model is.

This section briefly introduces the HJM model, which is the most general forward rate model. For additional details, readers are recommended to consult Cairns (2004), Munk (2011), or Shreve (2004), among others. For details on calibration, readers are recommended to consult Wu (2009). Forward rate process Let $\left(\Omega, \mathcal{F}{t \in[0, \tau]}, \mathbf{P}\right)$ be a filtered probability space, where $\mathcal{F}{t \in[0, \tau]}$ is the augmented filtration and $\mathbf{P}$ denotes the real-world measure. The instantaneous forward rate with maturity $T$ observed at time $t$ is denoted by $f(t, T)$. When the usage is unambiguous, $f(t, T)$ will be called the forward rate. Typically $f(0, T)$ represents an initial forward rate.

We assume that the dynamics of $f(t, T)$ on $\left(\Omega, \mathcal{F}{t \in[0, \tau]}, \mathbf{P}\right)$ is represented by $$ d f(t, T)=\alpha(t, T) d t+\sigma(t, T) d W{t}, $$ where $W_{t}=\left(W_{t}^{1}, \cdots, W_{t}^{d}\right)^{T}$ is a $d$-dimensional P-Brownian motion, and $\alpha(t, T)$ and $\sigma(t, T)$ are predictable processes satisfying some technical conditions. Here, $\sigma(t, T)=\left(\sigma^{1}(t, T), \cdots, \sigma^{d}(t, T)\right)^{T}$ is a $d$-dimensional process. The second term, $\sigma(t, T) d W_{t}$ denotes the inner product of $\sigma(t, T)$ and $d W_{t}$ in $\mathbf{R}^{d}$, specifically $$ \sigma(t, T) d W_{t}=\sum_{l=1}^{d} \sigma^{l}(t, T) d W_{t}^{l} . $$

金融代写|利率建模代写Interest Rate Modeling代考|Arbitrage Pricing and Market Price of Risk

This section briefly studies some fundamental subjects in the HJM model, specifically, forward rate process, arbitrage pricing, the market price of risk, and state price deflator. Forward rate process Here let us represent the forward rate process under the risk-neutral measure Q. Differentiating equation (4.9) with respect to $T$, we have $$ -\alpha(s, T)-\sigma(s, T) \int_{s}^{T} \sigma(s, u) d u=\frac{\partial b(s, T)}{\partial T} . $$ From equations (4.10) and (4.12), it follows that $$ \begin{aligned} -\alpha(s, T)-\sigma(s, T) \int_{s}^{T} \sigma(s, u) d u &=\frac{\partial v(s, T)}{\partial T} \varphi_{t} \ &=-\sigma(s, T) \varphi_{t} \end{aligned} $$ Substituting the above into equation (4.1), we obtain $$ d f(t, T)={-\sigma(t, T) v(t, T)+\sigma(t, T) \varphi(t)} d t+\sigma(t, T) d W_{t} $$ Recall the Q-Brownian motion $Z_{t}=\int_{0}^{t} \varphi_{s} d s+W_{t}$. Substituting this into the above, we have $$ d f(t, T)=-\sigma(t, T) v(t, T) d t+\sigma(t, T) d Z_{t} $$ where the drift under $\mathbf{Q}$ is completely determined by the volatility $\sigma(t, T)$. This form is the well-known forward rate process in the HJM model. For pricing interest rate derivatives, the dynamics of the forward rates are typically simulated by equation (4.18), and the bond pricing is performed by using this form. This method is essentially the same as used with short rate models.

金融代写|利率建模代写Interest Rate Modeling代考|Volatility and Principal Components

This section introduces a method for constructing the volatility in the H.JM model. There are two major approaches to do so. One is a market approach; the other is a historical approach.

In the market approach, the volatility is estimated such that the model implies option prices consistent with their market prices. In the historical approach, the volatility is constructed to represent a historical dynamics of an interest rate, for example, the short rate or the forward rate. Experimentally, these two approaches result in quite different volatility structures.

When we calibrate the model for derivatives pricing, the market approach should be employed. In this, it is understood that historical volatility cannot explain market prices because the option prices are determined mostly by traders’ forecasts for the future market rather than by historical volatility. Therefore, adopting a historical approach will result in a model that misprices major derivatives. Such a model is not valid for derivatives trading.

However, when we intend to calibrate a model for interest-risk-management, the historical approach is recommended, rather than the market approach. In the historical approach, principal component analysis (PCA) is a standard technique for reducing the dimensionality of the model. PCA will be repeatedly used in this book, and we introduce the construction of volatility by applying PCA. The fundamentals of PCA and the relevant linear algebra are given in Appendix B.