统计代写|金融统计代写Financial Statistics代考|GRA6518

如果你也在 怎样代写金融统计Financial Statistics这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

金融统计是将经济物理学应用于金融市场。它没有采用金融学的规范性根源,而是采用实证主义框架。它包括统计物理学的典范,强调金融市场的突发或集体属性。经验观察到的风格化事实是这种理解金融市场的方法的出发点。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融统计Financial Statistics方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融统计Financial Statistics代写方面经验极为丰富,各种代写金融统计Financial Statistics相关的作业也就用不着说。

我们提供的金融统计Financial Statistics及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

统计代写|金融统计代写Financial Statistics代考|A compromise between simulation and analytical methods

For further treatment, in particular in Chapter 11 , it is important to develop a right attitude to the balance between simulation and analytical methods. It is a compromise between them, when one reinforces the other.

On one hand (see [152], p. 45 ), the analytical study, even in a highly simplified situation, may suggest useful ideas for simulation analysis. For example, it helps to keep singularities of the model in check. These may be overlooked when simulation is performed, whence errors. Besides, an analytical study of the main variables involved in the model done in advance may advance simulation by choosing the most appropriate distributions. Overall, a preliminary acquaintance with the model by means of analytical investigation may help to develop a reasonable simulation strategy, and may be useful for computational optimization.

On the other hand, simulation can help us to rehabilitate the analytical methods in the opinion of practitioners. Although some practitioners feel that a majority of analytical methods are derived using unnatural assumptions, they may still be used for verification of numerical results obtained by simulation. This can be done by comparing them with theoretical results, albeit in those conditions in which the latter were obtained.

Let us summarize. The traditional analytical methods and methods of simulation should under no circumstances be considered as competing methods. The general rule (see [53], p. 154) is that analytical investigations should be carried out whenever possible. However, one should resist the temptation to manipulate the

premises of the model, simplifying it to make such analytical investigation possible, if it leads to a violation of the model’s applicability in real-world conditions.

If this simplification is nevertheless done, as is often the case in classical risk theory, then a clear warning should be made regarding the existence of limitations in the applicability, or even the inapplicability of the model. After that, when other opportunities are exhausted and all warnings are made, simulation techniques may be applied.

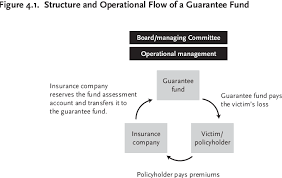

统计代写|金融统计代写Financial Statistics代考|The insurance system

Let us start with a brief summary of the insurance system’s fundamentals which have already been presented in detail in Chapter 1. This system is commonly regarded as a mechanism designed to reduce the adverse financial impact of random events that prevent fulfillment of reasonable expectations. Insurers issue contracts called policies, according to which an amount equal to or less than the value of financial losses will be paid, if the property is damaged or destroyed in an accident occurring during the term of the contract.

For the insureds, this practice provides protection against accidental loss in the sense that they will pay much less in premiums than they probably would otherwise have to pay in the case of an accident. Additionally, in contrast to the losses that are a random variable, the premium payment is a fixed, non-random sum of money.

Normally, the insurer seeks to spread the risk and costs of random losses among all the contracts in the portfolio, and over time. In this endeavor, it faces many constraints, and significant, unavoidable uncertainty. In essence, the insurer is a buffer set to dampen variations in claim amounts not only in a single year, but over a number of consecutive years. The insurer divides the total variation in claims between the premiums and the financial resources previously received.

The insurance system is regulated in accordance with two fundamental principles. One of these has its origins lying in insurance ethics, and is called the principle of equity ${ }^{2}$. According to this principle, the value of premiums should be “fair”. Conceptually, this means that all insurers should not pay more than the cost of the risk they bring into the insurer’s portfolio.

We have already mentioned (see Section 1.1.2) that ethical considerations are supported by quite pragmatic reasons: no insurance manager wants to entice its customers to switch to a competing company, or complain about it to the court. The systematic underpayment is also unacceptable, since this could lead to the ruin of the insurer and to the loss of insurance protection by all of its customers.

统计代写|金融统计代写Financial Statistics代考|Short-term and long-term regulations

The main purpose of this chapter is to outline the long-term ${ }^{7}$ integral model of the insurance business for a company operating on a competitive, but effectively regulated market. Under such regulation, each company on the market complies with mandatory annual minimum requirements for its solvency. This compliance is watched by the regulator. It removes from the market those companies that fail to meet these minimum solvency requirements, which is usually checked at the beginning of each insurance year.

In reality, it is not easy for supervisory and regulatory authorities to instil such discipline among the market participants. However, we will assume that this is achieved, and that regulation is efficient in this sense. We will be focussed on the strategic danger posed by overly aggressive competition. Of course, effective short-term regulation does not guarantee long-term business prosperity. A fall in the company’s prices on the profitable market is usually accompanied by a rise in its attractiveness to investors, together with the profit growth shown in its annual reports. In an effort to please the shareholders, who are the employers of the company’s management, and who want to see growing profit on a regular basis, insurance managers can neglect the strategic considerations and act to the detriment of long-term solvency; this will not be detected by short-term regulation, at least not during the initial stages.

金融统计代考

统计代写|金融统计代写Financial Statistics代考|A compromise between simulation and analytical methods

对于进一步的处理,特别是在第 11 章中,重要的是要对模拟和分析方法之间的平衡形成正确的态度。当一个人加强另一个人时,这是他们之间的妥协。

一方面(参见 [152],第 45 页),即使在高度简化的情况下,分析研究也可能为模拟分析提出有用的想法。例如,它有助于控制模型的奇异性。在执行模拟时,这些可能会被忽略,从而导致错误。此外,预先对模型中涉及的主要变量进行分析研究,可以通过选择最合适的分布来推进模拟。总体而言,通过分析调查初步了解模型可能有助于制定合理的模拟策略,并可能有助于计算优化。

另一方面,模拟可以帮助我们恢复从业者看来的分析方法。尽管一些从业者认为大多数分析方法是使用不自然的假设得出的,但它们仍可用于验证通过模拟获得的数值结果。这可以通过将它们与理论结果进行比较来完成,尽管在获得后者的条件下。

让我们总结一下。传统的分析方法和模拟方法在任何情况下都不应被视为竞争方法。一般规则(参见 [53],第 154 页)是应尽可能进行分析调查。然而,人们应该抵制操纵

模型的前提,如果它导致违反模型在现实条件下的适用性,则对其进行简化以使此类分析调查成为可能。

如果仍然进行了这种简化,就像经典风险理论中经常发生的情况一样,那么就应该明确警告存在适用性限制,甚至模型不适用。之后,当其他机会用尽并发出所有警告时,可以应用模拟技术。

统计代写|金融统计代写Financial Statistics代考|The insurance system

让我们从第 1 章详细介绍的保险系统基本原理的简要总结开始。该系统通常被认为是一种旨在减少阻碍实现合理预期的随机事件的不利财务影响的机制。保险公司签发称为保单的合同,根据该合同,如果财产在合同期限内发生意外损坏或毁坏,将支付等于或低于经济损失价值的金额。

对于受保人来说,这种做法可以防止意外损失,因为他们支付的保费将比他们在发生事故时可能需要支付的保费少得多。此外,与作为随机变量的损失相比,保费支付是固定的、非随机的金额。

通常,保险公司会寻求在投资组合中的所有合约之间以及随着时间的推移分散随机损失的风险和成本。在这一努力中,它面临着许多制约因素和重大的、不可避免的不确定性。从本质上讲,保险公司是一个缓冲装置,可以抑制索赔金额的变化,不仅在一年内,而且在连续几年内。保险公司将索赔的总变化在保费和之前收到的财务资源之间进行划分。

保险制度根据两个基本原则进行监管。其中之一起源于保险伦理,被称为公平原则2. 根据这个原则,保费的价值应该是“公道的”。从概念上讲,这意味着所有保险公司所支付的费用不应超过他们为保险公司投资组合带来的风险成本。

我们已经提到(参见第 1.1.2 节),道德考虑得到了非常务实的理由的支持:没有保险经理愿意诱使其客户转向竞争公司,或向法院投诉。系统性的少付也是不可接受的,因为这可能导致保险公司破产,并导致其所有客户失去保险保障。

统计代写|金融统计代写Financial Statistics代考|Short-term and long-term regulations

本章的主要目的是概述长期7对于在竞争激烈但受到有效监管的市场上运营的公司而言,其保险业务的整体模型。根据此类法规,市场上的每家公司都遵守强制性的年度偿付能力最低要求。这种合规性受到监管机构的监督。它将那些未能满足这些最低偿付能力要求的公司从市场上剔除,这些要求通常在每个保险年度开始时进行检查。

实际上,监管部门要向市场参与者灌输这样的纪律并不容易。然而,我们将假设这已经实现,并且从这个意义上说监管是有效的。我们将专注于过度激进的竞争所带来的战略危险。当然,有效的短期监管并不能保证长期的商业繁荣。公司在盈利市场上的价格下跌通常伴随着其对投资者的吸引力的增加,以及其年度报告中显示的利润增长。为了取悦股东,他们是公司管理层的雇主,他们希望看到定期增长的利润,保险经理可以忽略战略考虑,采取损害长期偿付能力的行为;

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。