如果你也在 怎样代写金融风险管理Financial Risk Management这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

金融风险管理是识别风险、分析风险并在接受或减轻风险的基础上做出投资决策的过程。这些风险可以是定量的,也可以是定性的,财务管理人员的工作就是利用现有的金融工具来对冲企业的风险。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融风险管理Financial Risk Management方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融风险管理Financial Risk Management方面经验极为丰富,各种代写金融风险管理Financial Risk Management相关的作业也就用不着说。

我们提供的金融风险管理Financial Risk Management及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等楖率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

金融代写|金融风险管理代写Financial Risk Management代考|BRIEF LITERATURE REVIEW ON FINANCIAL RISK

FR includes several types of risk, such as market risk, model risk, credit risk, liquidity risk, operational risk, and risk of disclosure compose the financial risk, and some of these types of FR are also divided into various classes of risk. For example, market risk (Schroeck, 2002) is composed of four kinds of risk: the equity risk, the interest rate risk, the currency risk, and commodity risk (Salomons \& Grootveld, 2003). From the different types of FR, risk disclosure is related to good CG practices, making companies more transparent in disclosing risks, helping investors to make a better decision in their portfolio investment, creating benefits to firms and shareholders, and, consequently, improving the competitiveness of companies (Solomon et al., 2000). Thus, we can see that it is expected an influence of CG on firms FR.

The CG practices are determinant to protect investors’ and other stakeholders’ interests (Soltani \& Maupetit, 2015). Indeed, CG proposes a set of practices to reduce the conflicts between managers and shareholders (Vieira \& Neiva, 2019). The most concise definition of CG was provided by the Cadbury Report in 1992, “Corporate governance is the system by which companies are directed and controlled”, and all the responsibility is placed over their leaders. For most companies, those leaders are the directors, responsible for the decision of the long-term strategy of the company, to serve the best interests of all the stakeholders.

The CG rules and practices present different stages of development, according to the economic characteristics of countries. For example, the Western Continental European firms present higher levels of ownership concentration and the dominance of family owners (Aganin \& Volpin, 2002; Högfeldt, 2003). Developing countries characterize Central Europe, being now consolidating their $\mathrm{CG}$ systems to improve investor protection and transparency (Svejnar, 2002). Eastern Europe exposes diverse CG characteristics, with strong ownership concentration and poor investor protection. For example, the United Kingdom (UK) is characterized by dispersed ownership, liquid capital market, transparency, and high investors’ protection, while France, Germany, and Italy are making efforts to improve the stock market efficiency, the investor protection. as well as best practice codes (Aluchna, 2016). Consequently, we expect that different $\mathrm{CG}$ practices will influence differently the firm’s financial risk.

The economic failures oyer the past, as well as the current economic changes, show the need for efficient CG practices and financial risk disclosure approaches (Luo, 2016). Indeed, various studies analyze how CG affects the level of FR disclosure, such as the ones of Alnabsha et al. (2018), Elamer and Benyazid (2018), Solomon et al. (2000), Ettredge et al. (2011), Ntim et al. (2013), Bufarwa et al. (2020) and Putri et al. (2021).

Bufarwa et al. (2020) analyze the impact of CG mechanisms on FR reporting in the UK, considering a sample of 50 non-financial firms listed on the London Stock Exchange in the period between 2011 and 2015. The authors find that $\mathrm{CG}$ has a significant influence on FR disclosure. Board gender diversity has a positive effect on the level of corporate financial risk disclosure, which adds to the results of previous studies, such as the ones of Barako and Brown (2008), Ntim et al. (2012), and Ntim et al. (2013). Block ownership has also a positive impact on FR disclosure, suggesting that the UK firms will engage in a high level of financial disclosure, including voluntary disclosures. This result is in agreement with the findings of Abraham and $\operatorname{Cox}$ (2007) and Oliveira et al. (2011). However, the authors find no significant relationship between board size and corporate FR disclosure, which is consistent with the results of Elzahar and Hussainey (2012), but inconsistent with the findings of Ntim et al. (2013), who find a positive relationship between these variables.

金融代写|金融风险管理代写Financial Risk Management代考|GENERAL BIBLIOMETRIC ANALYSIS ON FINANCIAL RISK

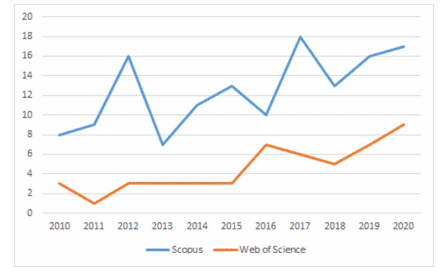

Bibliometric analysis is a method that turns easier the research of the relationship between research criteria and variables related to the research and environment of that research. During this research, it was applied the exploratory, descriptive, and bibliographic research methodology, performing a content analysis through the keywords “financial risk” and “corporate governance”. Provided the authors wanted a recent analysis period, they concentrate the chapter research during the period 2010-2020. Just by searching for the keyword earnings management in the Scopus database, it was found a total of 14,942 documents (from all types), while in the Web of Science database only 4,542 documents, also from all types. Regarding the analysis concentrated on the keywords “financial risk” and “corporate governance” for the 2010-2020 period, the authors end with a final sample of 138 documents in the Scopus database and 50 documents in the Web of Science database.

Another classification performed in our study is the kind of quantitative and qualitative research that takes on its basis a content analysis. The acquired data has on its basis several sources which are found in Scopus (https://www.scopus.com/search/), a database with a huge quantity of articles and Web of Science (https://www.webofscience.com/wos/woscc/basic-search). The process of data collection in this platform is divided into several parameters: the choice of the database, the definition of keywords, the identification of the article, the journal identification, and the classification of the articles. The study performed and presented next will follow over some of these parameters.

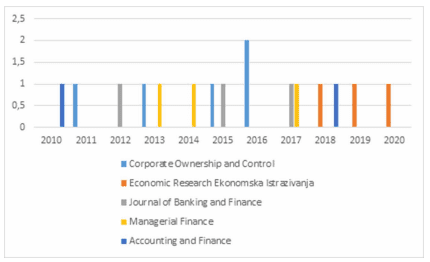

Figure 1 presents the evolution of the documents collected during 2010 and 2020 , after applying the parameters defined in the Scopus and Web of Science databases, leading us to a total database of 138 documents, and 50 documents, respectively.

金融风险管理代考

金融代写|金融风险管理代写Financial Risk Management代考|BRIEF LITERATURE REVIEW ON FINANCIAL RISK

FR包括几类风险,如市场风险、模型风险、信用风险、流动性风险、操作风险和披露风险等构成财务风险,其中部分FR又分为各种风险类别。例如,市场风险(Schroeck,2002)由四种风险组成:股权风险、利率风险、货币风险和商品风险(Salomons \& Grootveld,2003)。从不同类型的 FR 来看,风险披露与良好的 CG 实践相关,使公司在披露风险时更加透明,帮助投资者在组合投资中做出更好的决策,为公司和股东创造利益,从而提高竞争力公司(所罗门等人,2000 年)。因此,我们可以看到 CG 对公司 FR 的影响是预期的。

企业治理实践是保护投资者和其他利益相关者利益的决定性因素(Soltani \& Maupetit,2015)。事实上,CG 提出了一套实践来减少经理和股东之间的冲突(Vieira \& Neiva,2019)。1992年的吉百利报告对CG给出了最简洁的定义,“公司治理是指导和控制公司的制度”,一切责任都落在了领导者身上。对于大多数公司来说,这些领导者是董事,负责决定公司的长期战略,为所有利益相关者的最大利益服务。

CG 规则和实践根据各国的经济特点呈现出不同的发展阶段。例如,欧洲西部大陆的公司呈现出更高水平的所有权集中度和家族所有者的支配地位(Aganin \& Volpin,2002;Högfeldt,2003)。发展中国家是中欧的特征,现在正在巩固他们的CG提高投资者保护和透明度的系统(Svejnar,2002 年)。东欧展现出多元化的企业管治特征,所有权集中度高,投资者保护不力。例如,英国(UK)的特点是股权分散、资本市场流动性强、透明度高、投资者保护程度高,而法国、德国和意大利则在努力提高股市效率,提高投资者保护水平。以及最佳实践代码(Aluchna,2016)。因此,我们期望不同的CG实践将对公司的财务风险产生不同的影响。

过去的经济失败以及当前的经济变化表明,需要有效的 CG 实践和财务风险披露方法(Luo,2016 年)。事实上,各种研究分析了 CG 如何影响 FR 披露的水平,例如 Alnabsha 等人的研究。(2018), Elamer 和 Benyazid (2018), Solomon 等人。(2000 年),埃特雷奇等人。(2011), Ntim 等人。(2013), Bufarwa 等人。(2020)和普特里等人。(2021 年)。

布法瓦等人。(2020)分析了 CG 机制对英国 FR 报告的影响,以 2011 年至 2015 年期间在伦敦证券交易所上市的 50 家非金融公司为样本。作者发现CG对FR披露有重大影响。董事会性别多样性对公司财务风险披露水平有积极影响,这增加了先前研究的结果,例如 Barako 和 Brown (2008)、Ntim 等人的研究结果。(2012 年)和 Ntim 等人。(2013)。整体所有权对财务报告披露也有积极影响,这表明英国公司将进行高水平的财务披露,包括自愿披露。这一结果与亚伯拉罕和考克斯(2007)和奥利维拉等人。(2011)。然而,作者发现董事会规模与公司 FR 披露之间没有显着关系,这与 Elzahar 和 Hussainey (2012) 的结果一致,但与 Ntim 等人的研究结果不一致。(2013),他们发现这些变量之间存在正相关关系。

金融代写|金融风险管理代写Financial Risk Management代考|GENERAL BIBLIOMETRIC ANALYSIS ON FINANCIAL RISK

文献计量分析是一种更容易研究研究标准和与研究和研究环境相关的变量之间的关系的方法。本研究采用探索性、描述性和书目式研究方法,通过关键词“金融风险”和“公司治理”进行内容分析。如果作者想要一个最近的分析期,他们将把章节研究集中在 2010-2020 年期间。仅在 Scopus 数据库中搜索关键词收益管理,共找到 14,942 篇文献(来自所有类型),而在 Web of Science 数据库中只有 4,542 篇文献,也来自所有类型。关于 2010-2020 年期间集中在关键词“金融风险”和“公司治理”的分析,

在我们的研究中进行的另一种分类是基于内容分析的定量和定性研究。获取的数据基于 Scopus (https://www.scopus.com/search/) 中的多个来源,该数据库包含大量文章和 Web of Science (https://www.webofscience. com/wos/woscc/basic-search)。该平台的数据采集过程分为几个参数:数据库的选择、关键词的定义、文章的识别、期刊的识别、文章的分类。接下来进行和介绍的研究将遵循其中一些参数。

图 1 展示了 2010 年和 2020 年期间收集的文档的演变,在应用 Scopus 和 Web of Science 数据库中定义的参数后,我们的数据库分别包含 138 个文档和 50 个文档。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。统计代写|python代写代考

随机过程代考

在概率论概念中,随机过程是随机变量的集合。 若一随机系统的样本点是随机函数,则称此函数为样本函数,这一随机系统全部样本函数的集合是一个随机过程。 实际应用中,样本函数的一般定义在时间域或者空间域。 随机过程的实例如股票和汇率的波动、语音信号、视频信号、体温的变化,随机运动如布朗运动、随机徘徊等等。

贝叶斯方法代考

贝叶斯统计概念及数据分析表示使用概率陈述回答有关未知参数的研究问题以及统计范式。后验分布包括关于参数的先验分布,和基于观测数据提供关于参数的信息似然模型。根据选择的先验分布和似然模型,后验分布可以解析或近似,例如,马尔科夫链蒙特卡罗 (MCMC) 方法之一。贝叶斯统计概念及数据分析使用后验分布来形成模型参数的各种摘要,包括点估计,如后验平均值、中位数、百分位数和称为可信区间的区间估计。此外,所有关于模型参数的统计检验都可以表示为基于估计后验分布的概率报表。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

statistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

机器学习代写

随着AI的大潮到来,Machine Learning逐渐成为一个新的学习热点。同时与传统CS相比,Machine Learning在其他领域也有着广泛的应用,因此这门学科成为不仅折磨CS专业同学的“小恶魔”,也是折磨生物、化学、统计等其他学科留学生的“大魔王”。学习Machine learning的一大绊脚石在于使用语言众多,跨学科范围广,所以学习起来尤其困难。但是不管你在学习Machine Learning时遇到任何难题,StudyGate专业导师团队都能为你轻松解决。

多元统计分析代考

基础数据: $N$ 个样本, $P$ 个变量数的单样本,组成的横列的数据表

变量定性: 分类和顺序;变量定量:数值

数学公式的角度分为: 因变量与自变量

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。