金融代写|金融风险管理代写Financial Risk Management代考|MFIN6205

如果你也在 怎样代写金融风险管理Financial Risk Management这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

金融风险管理是识别风险、分析风险并在接受或减轻风险的基础上做出投资决策的过程。这些风险可以是定量的,也可以是定性的,财务管理人员的工作就是利用现有的金融工具来对冲企业的风险。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融风险管理Financial Risk Management方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融风险管理Financial Risk Management方面经验极为丰富,各种代写金融风险管理Financial Risk Management相关的作业也就用不着说。

我们提供的金融风险管理Financial Risk Management及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等楖率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

金融代写|金融风险管理代写Financial Risk Management代考|BRIEF LITERATURE REVIEW ON FINANCIAL RISK AND GENDER DIVERSITY

FR is normally referred to as the possibility that a firm’s cash flow will prove to be inadequate to meet its obligations, and is related to the odds of losing money, which can result in the loss of capital to interested parties. There are several types of FR, like financial distress risk (Altman, 1968), market risk (Salomons \& Grootveld, 2003), operational risk (Girling, 2013), disclosure risk (Linsley \& Shrives, 2006), model risk (Jokhadze \& Schmidt, 2020), and credit risk (Putri, Bunga \& Rochman, 2021). Many factors have been reported in the literature to explain firms’ risk. One of the reported factors, influencing management decisions, and, consequently, the firms’ risk, is GD. Other recently studied factors include economic policy uncertainty (Wen et al., 2021), policy and corporate financing (Lee et al., 2021), Knowledge management (Hock-Doepgen et al., 2021), cash reserves, and financial constraints (Lee and Wang, 2021), corporate social responsibility (Kuo et al., 2021), gender diversity (Cho et al., 2021), just to mention a few.

Indeed, previous studies find evidence that women have different characteristics in what concerns firms management decisions, because of their different understanding of market conditions, creativity and public image (Smith et al., 2006), communication and listening skills (Julizaerma \& Sori, 2012), and the decision-making process (Bart \& McQueen, 2013). In addition, Singh et al. (2008) argue that females are more likely to bring international diversity to the board of directors. Huse and Solberg (2006) posit that women are better prepared than men for board meetings and Adams and Ferreira (2007) conclude that they have better attendance records. From a psychological perspective, Barber and Odean (O001) held that men are more nverconfident than women and Olsen and Cox (On01) conclude that females are more risk-averse than men. The conclusions of Barber and Odean (2001) and Olsen and $\operatorname{Cox}$ (2001) suggest that men tend to make riskier financial decisions. However, Olsen and Cox (2001) also conclude that females are more prone to emotional conflicts than men. Consequently, we expect that GD influences a firm’s FR.

There is plenty of evidence on gender differences in management decisions that affect firms’ FR, such as Jianakoplos and Bernasek (1998), Byrnes et al. (1999), Croson and Gneezy (2009), Ahern and Dittmar (2012), Huang and Kisgen (2013), Berger et al. (2014), Lenard et al. (2014), Faccio et al. (2016), Filippin and Crosetto (2016), Sila et al. (2016), Jeong and Harrison (2017), Bernile et al. (2018), L’Haridon and Vieder (2019), Li and Zeng (2019), Bufarwa et al. (2020), Hurley and Choudhary (2020) and Saeed et al. (2021).

Within the U.S. context, Huang and Kisgen (2013) posit a negative association between executive women positions and leverage. In the same line, Faccio et al. (2016) report that firms with female CEOs present lower leverage levels. Concomitantly, Hurley and Choudhary (2020) show that the impact of female CFOs on firms’ financial risk is mixed, depending on risk measures used. However, the evidence shows that increasing the female percentage of board members reduces firms’ risk. Li and Zeng (2019) argue for an insignificant relationship between female CEO and stock price crash risk that turns negative for female CFOs.

金融代写|金融风险管理代写Financial Risk Management代考|GENERAL BIBLIOMETRIC ANALYSIS ON FINANCIAL RISK

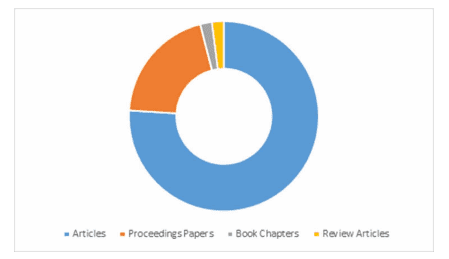

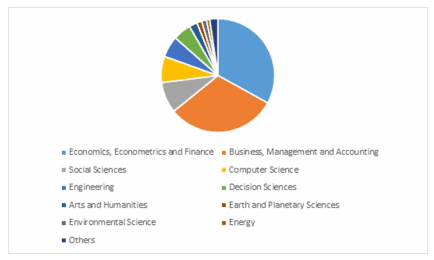

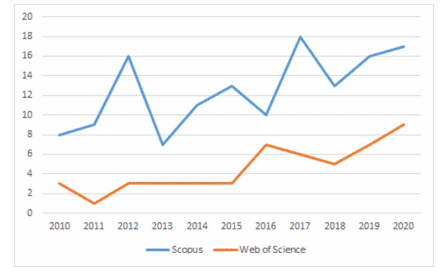

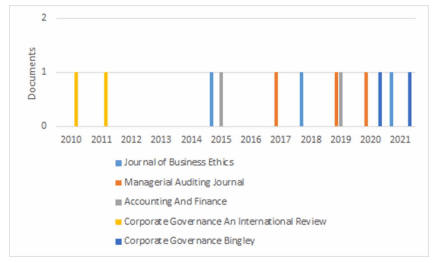

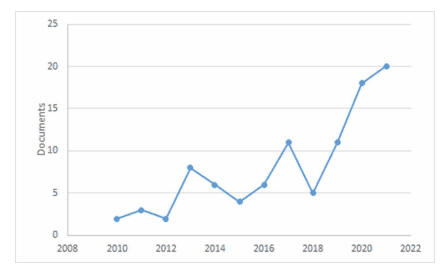

Bibliometric analysis is a method that turns easier the research of the relationship between research criteria and variables related to the research and environment of that research. During this research, it was applied the exploratory, descriptive, and bibliographic research methodology, performing a content analysis through the keyword “financial risk”. The search was performed at the end of June 2021. The authors consider the period between January and June 2021, since the research on the relationship between GD and FR is recent, and 2021 has a significant number of publications, compared with the other years. Provided the authors wanted a recent analysis period, they concentrate the chapter research during the period 2010-2021 (June). Even so, just by searching for the title/abstract/keywords “financial risk” in the Scopus database, it was found 15,979 documents (of all types) published from 2010 until June 2021. Regarding the analysis concentrated on the keywords “gender diversity” and “financial risk” for the analyzed period, the authors end with a final sample of 96 documents. The research was focused on Scopus since by crossing it with other sources like WoS findings were similar, as to the main documents available and published in indexed journals.

The six months of the last year of the sample (2021) was the period with more documents published (20), representing $20.8 \%$ of the articles published during the period in analysis. The period between 2010 and 2020 (11 years) represents $79.2 \%$ of the publications (76), which shows that it is a recent topic of research. Indeed, the first paper published that relates $G D$ and FR registered in Scopus is dated from 2001. The acquired data has on its basis several sources which are found in Scopus (https://www. scopus.com/search/), a database with a huge quantity of articles. The process of data collection in this platform is divided into several parameters: the choice of the database, the definition of keywords, the identification of the article, the journal identification, and the classification of the articles. The study performed and presented next will follow over some of these parameters.

Figure 1 presents the evolution of the documents collected for the period between 2010 and June 2021, after applying the parameters defined in the Scopus database, and looking for the title/abstract/ keywords “gender diversity” and “financial risk”, which relation we want to analyze, leading us to a total database of 96 documents, proving that this is a new topic in the financial research.

金融风险管理代考

金融代写|金融风险管理代写Financial Risk Management代考|BRIEF LITERATURE REVIEW ON FINANCIAL RISK AND GENDER DIVERSITY

FR 通常被称为公司的现金流量将被证明不足以履行其义务的可能性,并且与亏损的可能性有关,这可能导致利益相关方损失资本。FR 有几种类型,如财务困境风险 (Altman, 1968)、市场风险 (Salomons \& Grootveld, 2003)、操作风险 (Girling, 2013)、披露风险 (Linsley \& Shrives, 2006)、模型风险 ( Jokhadze \& Schmidt, 2020) 和信用风险 (Putri, Bunga \& Rochman, 2021)。文献中报道了许多解释公司风险的因素。所报告的影响管理决策以及公司风险的因素之一是 GD。最近研究的其他因素包括经济政策的不确定性(Wen et al., 2021)、政策和企业融资(Lee et al., 2021)、

事实上,先前的研究发现证据表明,女性在公司管理决策方面具有不同的特征,因为她们对市场条件、创造力和公众形象(Smith 等,2006)、沟通和倾听技巧(Julizaerma \& Sori, 2012)和决策过程(Bart \& McQueen,2013)。此外,辛格等人。(2008) 认为女性更有可能为董事会带来国际多元化。Huse 和 Solberg(2006 年)认为女性比男性为董事会会议做好了准备,Adams 和 Ferreira(2007 年)得出结论认为她们的出席记录更好。从心理学的角度来看,Barber 和 Odean (O001) 认为男性比女性更缺乏自信,Olsen 和 Cox (On01) 认为女性比男性更厌恶风险。考克斯(2001) 表明男性倾向于做出风险更大的财务决策。然而,Olsen 和 Cox (2001) 也得出结论,女性比男性更容易发生情感冲突。因此,我们预计 GD 会影响公司的 FR。

有相当多的证据表明管理决策中的性别差异会影响公司的FR,例如Jianakoplos 和Bernasek (1998),Byrnes 等。(1999)、Croson 和 Gneezy (2009)、Ahern 和 Dittmar (2012)、Huang 和 Kisgen (2013)、Berger 等人。(2014),伦纳德等人。(2014), Faccio 等人。(2016)、Filippin 和 Crosetto (2016)、Sila 等人。(2016)、Jeong 和 Harrison (2017)、Bernile 等人。(2018)、L’Haridon 和 Vieder (2019)、Li 和 Zeng (2019)、Bufarwa 等人。(2020)、Hurley 和 Choudhary (2020) 以及 Saeed 等人。(2021 年)。

在美国的背景下,Huang 和 Kisgen (2013) 认为女性高管职位与杠杆之间存在负相关。在同一行中,Faccio 等人。(2016 年)报告称,拥有女性 CEO 的公司的杠杆水平较低。与此同时,Hurley 和 Choudhary (2020) 表明,女性 CFO 对公司财务风险的影响是混合的,具体取决于所使用的风险衡量指标。然而,有证据表明,增加女性董事会成员的比例会降低公司的风险。Li 和 Zeng(2019 年)认为,女性 CEO 与股价崩盘风险之间的关系微不足道,而这对女性 CFO 来说是负面的。

金融代写|金融风险管理代写Financial Risk Management代考|GENERAL BIBLIOMETRIC ANALYSIS ON FINANCIAL RISK

文献计量分析是一种更容易研究研究标准和与研究和研究环境相关的变量之间的关系的方法。在这项研究中,它应用了探索性、描述性和书目研究方法,通过关键词“金融风险”进行内容分析。检索是在 2021 年 6 月下旬进行的。作者考虑了 2021 年 1 月至 2021 年 6 月期间,因为对 GD 和 FR 之间关系的研究是最近的,并且与其他年份相比,2021 年的出版物数量可观。如果作者想要最近的分析期,他们会集中在 2010-2021 年(六月)期间进行章节研究。即便如此,只要在 Scopus 数据库中搜索标题/摘要/关键词“金融风险”,发现从 2010 年到 2021 年 6 月发布的 15,979 份文件(所有类型)。关于分析期间集中在关键词“性别多样性”和“金融风险”的分析,作者以 96 份文件的最终样本结束。该研究主要集中在 Scopus 上,因为通过将其与 WoS 等其他来源的研究结果相似,就可获得并发表在索引期刊上的主要文件而言。

样本最后一年(2021 年)的 6 个月是发表文献较多的时期(20 篇),代表20.8%在分析期间发表的文章。2010 年至 2020 年期间(11 年)代表79.2%的出版物(76),这表明它是一个最近的研究课题。事实上,第一篇发表的论文涉及GD在 Scopus 中注册的 FR 是从 2001 年开始的。获取的数据基于 Scopus 中的多个来源(https://www.scopus.com/search/),这是一个拥有大量文章的数据库。该平台的数据采集过程分为几个参数:数据库的选择、关键词的定义、文章的识别、期刊的识别、文章的分类。接下来进行和介绍的研究将遵循其中一些参数。

图 1 展示了 2010 年至 2021 年 6 月期间收集的文件的演变,在应用 Scopus 数据库中定义的参数后,并寻找标题/摘要/关键词“性别多样性”和“金融风险”,我们想分析一下,我们总共有96个文档的数据库,证明这是金融研究中的一个新课题。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。统计代写|python代写代考

随机过程代考

在概率论概念中,随机过程是随机变量的集合。 若一随机系统的样本点是随机函数,则称此函数为样本函数,这一随机系统全部样本函数的集合是一个随机过程。 实际应用中,样本函数的一般定义在时间域或者空间域。 随机过程的实例如股票和汇率的波动、语音信号、视频信号、体温的变化,随机运动如布朗运动、随机徘徊等等。

贝叶斯方法代考

贝叶斯统计概念及数据分析表示使用概率陈述回答有关未知参数的研究问题以及统计范式。后验分布包括关于参数的先验分布,和基于观测数据提供关于参数的信息似然模型。根据选择的先验分布和似然模型,后验分布可以解析或近似,例如,马尔科夫链蒙特卡罗 (MCMC) 方法之一。贝叶斯统计概念及数据分析使用后验分布来形成模型参数的各种摘要,包括点估计,如后验平均值、中位数、百分位数和称为可信区间的区间估计。此外,所有关于模型参数的统计检验都可以表示为基于估计后验分布的概率报表。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

statistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

机器学习代写

随着AI的大潮到来,Machine Learning逐渐成为一个新的学习热点。同时与传统CS相比,Machine Learning在其他领域也有着广泛的应用,因此这门学科成为不仅折磨CS专业同学的“小恶魔”,也是折磨生物、化学、统计等其他学科留学生的“大魔王”。学习Machine learning的一大绊脚石在于使用语言众多,跨学科范围广,所以学习起来尤其困难。但是不管你在学习Machine Learning时遇到任何难题,StudyGate专业导师团队都能为你轻松解决。

多元统计分析代考

基础数据: $N$ 个样本, $P$ 个变量数的单样本,组成的横列的数据表

变量定性: 分类和顺序;变量定量:数值

数学公式的角度分为: 因变量与自变量

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。