如果你也在 怎样代写金融衍生品Financial Derivatives 这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。金融衍生品Financial Derivatives对于广大公众来说,长期以来一直是所有金融工具中最神秘、最不为人所知的。虽然一些金融衍生品相当简单,但不可否认的是,其他衍生品相当复杂,需要大量的数学和统计知识才能完全理解。

金融衍生品Financial Derivatives通常被视为过于复杂而难以理解的金融工具,个人投资者往往会回避。与此同时,市场专业人士指出,金融衍生品交易目前约占整个另类资产市场的40%。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融衍生品Financial derivatives方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融衍生品Financial derivatives代写方面经验极为丰富,各种代写金融衍生品Financial derivatives相关的作业也就用不着说。

金融代写|金融衍生品代写Financial derivatives代考|EQUITY SWAPS

The equity swap market has emerged from the need for more tailored derivatives. Equity swaps, as the term suggests, involve two parties that swap payments based on the notional value specified as some portfolio of equities. The most basic equity swaps involve fixed-for-floating payments based on the underlying notional value.

An investor (typically an institution) with exposure to equities in a portfolio is exposed to the risk of the stock market dropping in value. To hedge this risk using equity swaps, the institution could utilize an equity swap promising to pay the (variable) return on a broad stock index such as the S\&P 500 in return for a fixed percentage payment based on the notional value of the underlying portfolio of stocks. The resultant cash flows provide a fixed rate of return to the institution that protects the portfolio from falling stock prices. Note, for instance, that falling stock prices generate negative “payments” on the variable component of the swap; that is, the institution’s counterparty makes both the fixed payment promised in the swap agreement and the payment to compensate for the lost value in the underlying portfolio. Of course, this hedging strategy involves the loss of upside gains from the stock market as well-part of the price paid for hedge protection.

As with most swap agreements, terms of the contract can be tailored to individual needs in the marketplace. Instead of a fixed-for-variable swap, participants might elect to exchange the return on larger stocks, such as the S\&P 100 index, for the return on smaller stocks, such as the Russell 2000 index. This strategy could capture the spread between large and small stock returns. Although payments commonly are arranged at quarterly intervals, contract terms can be varied to meet the cash flow objectives of each counterparty.

One permutation of an equity index swap involves a single-stock swap contract wherein one party promises the return on a single firm in exchange for a fixed rate of return. These so-called single-name swaps introduce counterparty credit risk into equity investments (as do most all swap agreements). In the case of single-name swaps, however, this risk presents a significant impediment to the development of this market. For example, during the fall of 2008, when short sales were banned on many individual stocks, market participants could have skirted the ban using equity swaps. Despite the availability of these vehicles, very few took advantage of this chance, largely due to counterparty credit risk considerations.

金融代写|金融衍生品代写Financial derivatives代考|FUTURE OF EQUITY DERIVATIVES

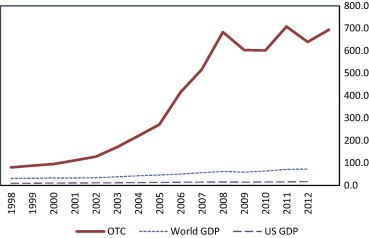

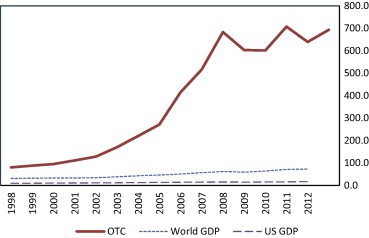

Assets under management for global hedge funds increased to $\$ 2.650$ trillion in 2007, according to HedgeFund Intelligence (2007). This represents a rise of 27 percent over the previous year. The Bank for International Settlements indicates that turnover of equity-linked exchange-traded derivatives rose by almost 33 percent in 2007 (BIS 2008b). U.S. equity options trading volume increased almost 50 percent during 2007 as well, according to the Options Clearing Corporation (the U.S.based clearing corporation (2008). Since the credit crisis of 2008, many investment categories have seen dramatic declines in both price levels and trading volume. Notably, while liquidity in OTC-traded products has fallen drastically during 2008, exchange-traded products have seen record levels of volume and trading activity as large institutions seek the relatively safe haven of central clearing on organized exchanges.

Part of the liquidity problem lies in the design of equity derivative instruments themselves. The nonlinear payoffs that are generated by options contracts, for instance, make it difficult to hedge large portfolios without regular adjustments. These regular adjustments presume adequate liquidity over the holding period of the option, exposing traders to liquidity risk not only at the time of purchase but throughout the life of the option. Further uncertainty exists even if individual assets initially are hedged appropriately because the correlations of assets within a portfolio can and do change over time. As a result, substantial correlation risk can also affect the bottom line for many banks.

The worldwide spread of derivatives contracts has also presented challenges to regulators and legal authorities. The Options Industry Council survey in 2006 indicated that 15 to 20 percent of U.S. options trading volume originated from Europe, creating the need for international cooperation. The CFTC has taken a leadership role in the International Organization of Securities Commissions and has established dozens of memorandums of understanding with other countries to share expertise and data and coordinate on regulatory affairs. The SEC is similarly working on rule changes to make it easier for foreign derivatives exchanges to market their products in the United States.

金融衍生品代写

金融代写|金融衍生品代写Financial derivatives代考|EQUITY SWAPS

股票掉期市场是由于对更有针对性的衍生品的需求而出现的。顾名思义,股权互换涉及双方根据指定为某种股权投资组合的名义价值互换支付。最基本的股权互换涉及基于潜在名义价值的固定换浮动支付。

在投资组合中持有股票的投资者(通常是机构)面临股票市场价值下跌的风险。为了利用股权掉期来对冲这种风险,机构可以利用股权掉期,承诺根据标准普尔500指数等广泛股票指数支付(可变)回报,以换取基于标的股票投资组合名义价值的固定百分比支付。由此产生的现金流为机构提供了固定的回报率,从而保护投资组合免受股价下跌的影响。例如,请注意,股价下跌会对掉期的可变部分产生负“支付”;也就是说,该机构的交易对手既支付掉期协议中承诺的固定款项,又支付补偿标的投资组合价值损失的款项。当然,这种对冲策略也会损失股票市场的上行收益,这也是对冲保护所付出的部分代价。

与大多数掉期协议一样,合约的条款可以根据市场的个人需求进行调整。参与者可能会选择用大型股票(如标普100指数)的回报来交换小型股票(如罗素2000指数),而不是固定换变量。这种策略可以捕捉到股票大收益和小收益之间的价差。虽然付款通常是按季度安排的,但合同条款可以根据每个交易对手的现金流量目标而变化。

股票指数掉期的一种排列涉及单一股票掉期合同,其中一方承诺单一公司的回报以换取固定的回报率。这些所谓的单名掉期将交易对手信用风险引入了股权投资(就像大多数掉期协议一样)。然而,就单名互换而言,这种风险对该市场的发展构成了重大障碍。例如,在2008年秋季,当许多个股被禁止做空时,市场参与者本可以利用股票互换绕开禁令。尽管有这些工具,但很少有人利用这个机会,这主要是出于对交易对手信用风险的考虑。

金融代写|金融衍生品代写Financial derivatives代考|FUTURE OF EQUITY DERIVATIVES

根据HedgeFund Intelligence(2007)的数据,2007年全球对冲基金管理的资产增加到2.650万亿美元。这比前一年增长了27%。国际清算银行指出,2007年与股票挂钩的交易所交易衍生品的营业额增长了近33% (BIS 2008b)。根据期权清算公司(美国清算公司,2008年)的数据,美国股票期权交易量在2007年也增长了近50%。自2008年信贷危机以来,许多投资类别的价格水平和交易量都出现了大幅下降。值得注意的是,虽然场外交易产品的流动性在2008年大幅下降,但由于大型机构寻求在有组织的交易所进行相对安全的中央清算,交易所交易产品的交易量和交易活动达到了创纪录的水平。

流动性问题的部分原因在于股权衍生工具本身的设计。例如,期权合约产生的非线性收益,使得不定期调整就很难对冲大型投资组合。这些定期调整假设在期权持有期间有足够的流动性,使交易者不仅在购买时,而且在期权的整个生命周期内都面临流动性风险。进一步的不确定性存在,即使个别资产最初被适当地对冲,因为投资组合中资产的相关性可以而且确实会随着时间的推移而改变。因此,大量相关风险也会影响许多银行的底线。

衍生品合约的全球蔓延也给监管机构和法律当局带来了挑战。期权行业委员会2006年的调查显示,美国15% – 20%的期权交易量来自欧洲,因此需要国际合作。CFTC在国际证券委员会组织(International Organization of Securities Commissions)中发挥领导作用,并与其他国家签署了数十份谅解备忘录,以分享专业知识和数据,并在监管事务上进行协调。美国证券交易委员会也同样致力于修改规则,使外国衍生品交易所更容易在美国销售其产品。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。