如果你也在 怎样代写金融衍生品Financial Derivatives 这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。金融衍生品Financial Derivatives是金融工具的三大类之一,另外两类是股权(即股票或股份)和债权(即债券和抵押贷款)。历史上最古老的衍生品例子,由亚里士多德证明,被认为是古希腊哲学家泰勒斯签订的橄榄合同交易,他在交换中获利。1936年被取缔的桶装水商店是一个较近的历史例子。

金融衍生品Financial Derivatives在金融领域,衍生品是一种合同,其价值来自于一个基础实体的表现。衍生品可用于多种目的,包括对价格变动进行保险(套期保值),为投机增加价格变动的风险,或进入其他难以交易的资产或市场。一些更常见的衍生品包括远期、期货、期权、掉期,以及这些的变体,如合成抵押债务和信用违约掉期。大多数衍生品在场外(场外)或芝加哥商品交易所等交易所进行交易,而大多数保险合同已经发展成为一个独立的行业。在美国,在2007-2009年的金融危机之后,将衍生品转移到交易所进行交易的压力越来越大。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融衍生品Financial derivatives方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融衍生品Financial derivatives代写方面经验极为丰富,各种代写金融衍生品Financial derivatives相关的作业也就用不着说。

金融代写|金融衍生品代写Financial derivatives代考|STRUCTURED PRODUCTS AND AN APPLICATION TO DERIVATIVE CONTRACTS

Given a basic understanding of derivative contracts and how derivative contracts are related, consider structured products with an application to derivative securities. Structured products are financial instruments that combine cash assets and/or derivatives to provide a risk/reward profile not otherwise available or only available at high cost in the cash market.

Structured products are often the securities that result from the securitization process and have been successfully created with portfolios of mortgage, automobile, and boat loans as well as credit derivatives. Securitization is the process by which mortgages issued by a financial institution are converted into mortgagebacked securities sold to investors or a firm’s accounts receivable portfolio is converted into asset-backed notes, for example. Investors in securitized loans face default and prepayment risk, among other risks, passed through by original loan issuer. Usually investors are offered multiple classes-called tranches-of notes that differ in their priority of payment rights to best match the investor’s risk-bearing preferences. Depending on the securitization structure, investors may choose between super-senior notes (first to be repaid, last to default), mezzanine notes (second to be repaid, second to default), and equity or capital notes (last to be repaid, first to default). Each tranche earns a different return based on the structured risk.

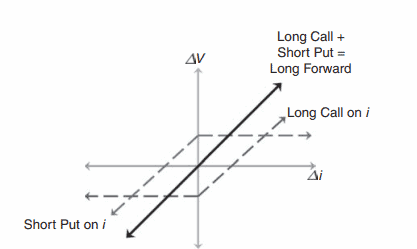

Of course, the correspondence of corporate securities and option contracts is familiar to students of derivatives. ${ }^4$ A zero-coupon bond issued by a firm without other debt can be viewed by the bondholder as a riskless bond plus a written put option (default premium) on the value of the firm’s assets. The put option is owned by shareholders and the firm can be “put” to the bondholders in exchange for a release of indebtedness. With multiple tranches in a structured product, junior debt claims are paid only after senior debt claims. The super-senior tranche, for example, can still be viewed as a riskless bond plus a written put option. The mezzanine and capital note claims can be viewed as bullish spreads (put options both purchased and sold) on the value of the issuing firm’s assets. Note that the correspondence between option contracts and corporate securities applies to all default-risky debt instruments.

金融代写|金融衍生品代写Financial derivatives代考|STANDARDIZATION VERSUS CUSTOMIZED PRODUCTS: DIFFERENCES IN STRUCTURE AND APPROACH

Exchanges and OTC derivatives dealers are aggressively innovative. Futures and options exchanges focus on designing products that appeal to many users, and their offering of standardized products has created efficiencies in information aggregation and the provision of liquidity. By providing a market that brings together buyers and sellers for its products, exchanges help users to minimize search and negotiation costs (Carlton 1984, p. 241). Futures exchanges are organized to facilitate liquidity by setting contract features that encourage competing intermediaries to provide immediacy, which attracts buyers and sellers whose demand for contracts to contend with the “price risks of volatility” leads them to trade frequently (Grossman and Miller 1988, p. 619).

The liquidity that characterizes exchange-traded derivatives stems primarily from their standardized features and a market structure that channels trading interest into homogeneous contracts. Futures contracts, for example, specify the quantity or the minimum size of the position, the minimum price variation or “tick” size, daily settlement and mark-to-market procedures, and the expiration date at which the underlying asset will be delivered or the contract expires and final payments are made. While some precision in hedging may be lost in the form of basis or correlation risk when the standard product does not precisely match the underlying risk to be hedged, transactions and search costs are reduced as fewer elements of the transaction need to be negotiated.

Exchanges are characterized by strong network economies in that liquidity attracts order flow, and this, in turn, leads to greater liquidity and still lower costs. The information inherent in trades and the competition it engenders increases the efficiency of prices and further lowers the cost of trading, giving rise to economies of scale and scope. Pirrong (2008) observes that exchanges achieve these economies in the execution function, when orders to buy and sell are matched and priced in the exchange auction process, and in the clearing function, when the price and contractual obligations are confirmed and deliveries and payments are processed. As exchanges have shifted from a model in which all transactions had to pass through intermediaries on a trading floor to a fully electronic market in which everything from order entry to final settlement is processed digitally, they have been able to expand their product line and realize economies of scope and scale in liquidity and processing (Domowitz 1995).

金融衍生品代写

金融代写|金融衍生品代写Financial derivatives代考|STRUCTURED PRODUCTS AND AN APPLICATION TO DERIVATIVE CONTRACTS

在对衍生品合约和衍生品合约之间的关系有了基本的了解后,考虑将结构性产品应用于衍生品证券。结构性产品是一种金融工具,它将现金资产和/或衍生品组合在一起,以提供在现金市场上无法获得或只能以高成本获得的风险/回报情况。

结构性产品通常是证券化过程中产生的证券,并且已经成功地与抵押贷款,汽车和船舶贷款以及信用衍生品的投资组合一起创建。证券化是指将金融机构发行的抵押贷款转换为出售给投资者的抵押贷款支持证券,或将公司的应收账款组合转换为资产支持票据的过程。在证券化贷款中,投资者面临的风险包括违约和提前还款风险,这些风险由原贷款发放机构传递。通常情况下,投资者会被提供多个类别的票据,这些票据在支付权的优先级上有所不同,以最好地匹配投资者的风险偏好。根据证券化结构的不同,投资者可以在超优先票据(第一个偿还,最后一个违约)、夹层票据(第二个偿还,第二个违约)和股本或资本票据(最后一个偿还,第一个违约)之间进行选择。根据结构性风险的不同,每一部分都有不同的回报。

当然,公司证券和期权合约的对应关系对于衍生品专业的学生来说是很熟悉的。无其他债务的公司发行的零息债券可以被债券持有人视为无风险债券加上公司资产价值的书面看跌期权(违约溢价)。看跌期权由股东所有,公司可以向债券持有人“看跌”,以换取债务的免除。在一个结构性产品中有多个级别,初级债务索赔只在高级债务索赔之后支付。例如,超优先级债券仍然可以被视为无风险债券加上书面看跌期权。夹层债券和资本票据债权可以被视为发行公司资产价值的看涨价差(买入和卖出的看跌期权)。请注意,期权合约和公司证券之间的对应关系适用于所有违约风险债务工具。

金融代写|金融衍生品代写Financial derivatives代考|STANDARDIZATION VERSUS CUSTOMIZED PRODUCTS: DIFFERENCES IN STRUCTURE AND APPROACH

交易所和场外衍生品交易商积极创新。期货和期权交易所专注于设计吸引许多用户的产品,它们提供的标准化产品提高了信息聚合和流动性提供的效率。通过提供一个将买家和卖家聚集在一起购买其产品的市场,交易所帮助用户将搜索和谈判成本降至最低(Carlton 1984, p. 241)。期货交易所的组织是为了促进流动性,通过设定合约特征,鼓励竞争的中介机构提供即时性,这吸引了买家和卖家,他们对合约的需求是为了应对“波动的价格风险”,导致他们频繁交易(Grossman和Miller 1988, p. 619)。

交易所交易衍生品的流动性主要源于它们的标准化特征和将交易兴趣引入同质合约的市场结构。例如,期货合约规定了头寸的数量或最小规模、最小价格变动或“点”大小、每日结算和按市值计价的程序,以及标的资产交割或合约到期和最终付款的到期日。虽然当标准产品不能精确匹配待对冲的基础风险时,套期保值可能会以基差或关联风险的形式失去一些准确性,但由于交易中需要协商的要素减少,交易和搜索成本减少。

交易所的特点是强大的网络经济,流动性吸引订单流,而这反过来又导致更大的流动性和更低的成本。交易中固有的信息及其引发的竞争提高了价格效率,进一步降低了交易成本,从而产生了规模经济和范围经济。Pirrong(2008)观察到,交易所在执行功能上实现了这些经济,即在交易所拍卖过程中买卖订单匹配并定价,在清算功能上实现了这些经济,即价格和合同义务得到确认,交割和支付得到处理。由于交易所已经从所有交易都必须通过交易大厅的中介机构的模式转变为一个完全电子化的市场,从订单输入到最终结算都是数字化处理的,他们已经能够扩大他们的产品线,并在流动性和处理方面实现范围和规模经济(Domowitz 1995)。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。