如果你也在 怎样代写投资组合Portfolio Theory 这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。投资组合Portfolio Theory是金融投资的集合,如股票、债券、商品、现金和现金等价物,包括封闭式基金和交易所交易基金(ETF)。人们普遍认为,股票、债券和现金构成了投资组合的核心。

投资组合Portfolio Theory是资产的集合,可以包括股票、债券、共同基金和交易所交易基金等投资。投资组合更像是一个概念,而不是一个物理空间,特别是在数字投资的时代,但把你的所有资产放在一个比喻的屋顶下可能会有帮助。

statistics-lab™ 为您的留学生涯保驾护航 在代写投资组合Investment Portfolio方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写投资组合Investment Portfolio方面经验极为丰富,各种代写投资组合Investment Portfolio相关的作业也就用不着说。

金融代写|投资组合代写Investment Portfolio代考|IRRATIONAL PEOPLE, IRRATIONAL MARKETS?

As goals-based investors aggregate, it seems clear that they will have an effect on market pricing. People are not isolated and, hard as it may be to remember these days, markets are comprised of real people. If these people were entering markets not for the fun of it but because they had specific objectives, that would carry some interesting consequences for the pricing mechanism. In this section, I would like to explore some interesting outcomes of market pricing if people are behaving in ways consistent with goals-based utility theory.

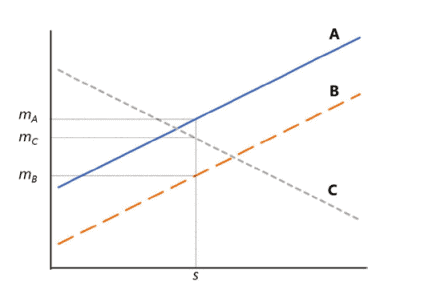

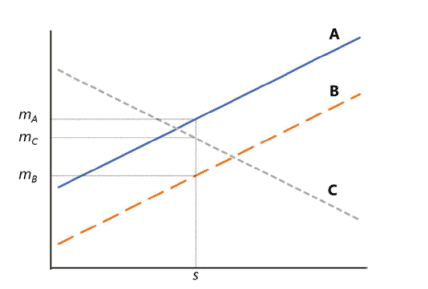

As we have explored, investors will seek to maximize the probability of attaining a goal. However, when considering something like pricing dynamics, it may be easier to simply analyze a line of indifference-that is, the points at which utility stays the same if we vary the other inputs. We assume that investors enter capital markets attempting to get a probability of goal achievement of at least $\alpha$, but greater than $\alpha$ is obviously preferred.

This treats the probability of goal achievement as a risk-aversion metric, which is essentially what it is. So, we can set up our form like this:

$$

v(A) \alpha=v(A) \phi(w, W, t),

$$

where $\alpha$ is the minimum probability our investor is willing to accept to achieve the goal, $w$ is the initial amount of wealth dedicated to the goal, $W$ is the amount of wealth required to achieve the goal, and $t$ is the time horizon within which the goal must be accomplished. Using the logistic cumulative distribution function, our equation becomes

From here, we can solve for $m$, or the minimum acceptable return, given some acceptable level of $\alpha$ :

$$

m \geq\left(\frac{W}{w}\right)^{\frac{1}{t}}-1+s \ln \left(\frac{1}{1-\alpha}-1\right)

$$

金融代写|投资组合代写Investment Portfolio代考|The Future Structure of Wealth Management Firms

Investment portfolios must be informed by goals, and goals, in turn, are influenced by the choice of investments.

Unfortunately, the current structure of wealth management firms is not conducive to delivering true goals-based solutions. While financial planning has now long been part of most wealth management practices, to execute the plan, firms build model portfolios-large boxes that can only ever approximate client needs. Of course, to date this has been the only way to scale a practice. It is not possible to run thousands of different portfolios, each with a separate objective and investment universe without a considerable investment of man-hours. Goals-based portfolio theory brings a need for better plan implementation. Those differences between account objectives and the differences between clients, though ignored by monolithic model portfolios, are fundamental to the proper execution of a goals-based plan.

Therefore, we need to update the structure and skill set of the wealth management firm.

To best understand the needed changes, we need to first understand the client experience. Goals-based investing puts the client at the absolute center of everything we do, so to properly understand the changes needed it is best to first understand our center of gravity. Let’s walk through the client experience from the point of first contact to the accomplishment of a goal.

A prospective client comes to the firm. Clients, of course, do not come to an advisor looking for goals; they have plenty of those. Clients come to the advisor looking for ways to accomplish their goals. The first meeting, in addition to the usual rapport-building, should be focused on understanding the panoply of goals: their relative importance, time horizons, funding requirements, and all else that has been discussed in this book so far. A clear understanding of the client’s current financial picture is also important. As a general rule, investment recommendations have no place being discussed in a first meeting. Certainly prospective clients will want some understanding of the firm’s opinions of markets and investment solutions offering, and some brief discussion on the firm’s points of difference is all sensible. But there is no way for an advisor to properly know what investment solutions are needed by the client without first doing the work of financial planning. Investments, in a goals-based framework, are simply tools to get a job done. How can we reach for the correct tool when we do not yet know what job needs doing?

After the initial discussion, the advisor takes the client’s data and builds a financial plan. Of course, the nature of the client and the listed goals will determine how detailed this financial plan needs to be (I am not fond of the 127-page financial plan, simpler is better in my view). Much of the plan is calculating the relative value of goals, calculating the allocation of current wealth and future savings across goals, the determination of optimal investment allocations for each subaccount, the determination of taxes on the various account types, and so on. The role of the financial planner is to map the plan of attack-it is, perhaps, the most important role in the firm. Errors at this stage will compound into later stages, becoming magnified and possibly catastrophic to the client. Financial planning done well is of paramount importance.

投资组合代考

金融代写|投资组合代写Investment Portfolio代考|IRRATIONAL PEOPLE, IRRATIONAL MARKETS?

随着以目标为导向的投资者聚集起来,似乎很明显,他们将对市场定价产生影响。人们并不是孤立的,尽管现在可能很难记住,市场是由真实的人组成的。如果这些人进入市场不是为了好玩,而是因为他们有特定的目标,这将给定价机制带来一些有趣的后果。在本节中,我想探讨一些有趣的市场定价结果,如果人们的行为方式与基于目标的效用理论相一致。

正如我们所探讨的,投资者将寻求实现目标的可能性最大化。然而,在考虑诸如定价动态之类的问题时,简单地分析一条无差异线可能更容易——也就是说,如果我们改变其他输入,效用保持不变的点。我们假设投资者进入资本市场试图获得目标实现的概率至少为$\alpha$,但大于$\alpha$显然是首选。

这将目标实现的可能性视为一种风险规避度量,本质上就是这样。所以,我们可以这样设置表单:

$$

v(A) \alpha=v(A) \phi(w, W, t),

$$

其中$\alpha$是我们的投资者愿意接受的实现目标的最小概率,$w$是用于实现目标的初始财富,$W$是实现目标所需的财富,$t$是必须完成目标的时间范围。使用logistic累积分布函数,我们的方程变成

从这里,我们可以解出$m$,或者给定某个可接受水平$\alpha$的最小可接受回报:

$$

m \geq\left(\frac{W}{w}\right)^{\frac{1}{t}}-1+s \ln \left(\frac{1}{1-\alpha}-1\right)

$$

金融代写|投资组合代写Investment Portfolio代考|The Future Structure of Wealth Management Firms

投资组合必须以目标为依据,而目标反过来又受到投资选择的影响。

不幸的是,目前财富管理公司的结构不利于提供真正基于目标的解决方案。虽然长期以来财务规划一直是大多数财富管理业务的一部分,但为了执行计划,公司建立了模型投资组合——这些大盒子只能接近客户的需求。当然,到目前为止,这是扩展实践的唯一方法。如果不投入大量的人力时间,就不可能运行数千个不同的投资组合,每个投资组合都有单独的目标和投资领域。基于目标的投资组合理论需要更好的计划实施。账户目标之间的差异和客户之间的差异,虽然被整体模型投资组合所忽略,但对于正确执行基于目标的计划是至关重要的。

因此,我们需要更新财富管理公司的结构和技能。

为了最好地理解所需的更改,我们需要首先了解客户体验。基于目标的投资将客户置于我们所做的一切的绝对中心,因此,为了正确理解所需的变化,最好首先了解我们的重心。让我们回顾一下从第一次接触到完成目标的客户体验。

一位潜在客户来到公司。当然,客户不是来找顾问寻找目标的;他们有很多。客户向顾问寻求实现目标的方法。第一次会议,除了通常的建立关系之外,应该集中于理解目标的整体:它们的相对重要性,时间范围,资金需求,以及本书迄今为止讨论过的所有其他内容。清楚地了解客户当前的财务状况也很重要。一般来说,投资建议不应该在第一次会议上讨论。当然,潜在客户希望了解公司对市场和投资解决方案的看法,对公司的不同之处进行一些简短的讨论是明智的。但是,如果不先做财务规划工作,顾问就不可能正确地知道客户需要什么样的投资解决方案。在以目标为基础的框架下,投资只是完成工作的工具。当我们还不知道需要做什么工作时,我们怎么能找到正确的工具呢?

在最初的讨论之后,顾问获取客户的数据并建立一个财务计划。当然,客户的性质和列出的目标将决定这个财务计划需要有多详细(我不喜欢127页的财务计划,在我看来越简单越好)。该计划的大部分内容是计算目标的相对价值,计算当前财富和未来储蓄在目标之间的分配,确定每个子账户的最佳投资分配,确定各种账户类型的税收,等等。财务规划师的角色是绘制攻击计划,这可能是公司中最重要的角色。这一阶段的错误将在以后的阶段中复杂化,变得更大,对客户来说可能是灾难性的。做好财务规划是至关重要的。

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。统计代写|python代写代考

随机过程代考

在概率论概念中,随机过程是随机变量的集合。 若一随机系统的样本点是随机函数,则称此函数为样本函数,这一随机系统全部样本函数的集合是一个随机过程。 实际应用中,样本函数的一般定义在时间域或者空间域。 随机过程的实例如股票和汇率的波动、语音信号、视频信号、体温的变化,随机运动如布朗运动、随机徘徊等等。

贝叶斯方法代考

贝叶斯统计概念及数据分析表示使用概率陈述回答有关未知参数的研究问题以及统计范式。后验分布包括关于参数的先验分布,和基于观测数据提供关于参数的信息似然模型。根据选择的先验分布和似然模型,后验分布可以解析或近似,例如,马尔科夫链蒙特卡罗 (MCMC) 方法之一。贝叶斯统计概念及数据分析使用后验分布来形成模型参数的各种摘要,包括点估计,如后验平均值、中位数、百分位数和称为可信区间的区间估计。此外,所有关于模型参数的统计检验都可以表示为基于估计后验分布的概率报表。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

statistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

机器学习代写

随着AI的大潮到来,Machine Learning逐渐成为一个新的学习热点。同时与传统CS相比,Machine Learning在其他领域也有着广泛的应用,因此这门学科成为不仅折磨CS专业同学的“小恶魔”,也是折磨生物、化学、统计等其他学科留学生的“大魔王”。学习Machine learning的一大绊脚石在于使用语言众多,跨学科范围广,所以学习起来尤其困难。但是不管你在学习Machine Learning时遇到任何难题,StudyGate专业导师团队都能为你轻松解决。

多元统计分析代考

基础数据: $N$ 个样本, $P$ 个变量数的单样本,组成的横列的数据表

变量定性: 分类和顺序;变量定量:数值

数学公式的角度分为: 因变量与自变量

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。