统计代写|金融统计代写financial statistics代考|Bubbles and crises

如果你也在 怎样代写金融统计financial statistics这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。

金融统计,是将经济物理学应用于金融市场。它没有采用金融学的规范性根基,而是采用实证主义框架。

statistics-lab™ 为您的留学生涯保驾护航 在代写金融统计financial statistics方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在代写金融统计financial statistics代写方面经验极为丰富,各种代写金融统计financial statistics相关的作业也就用不着说。

我们提供的金融统计financial statistics及其相关学科的代写,服务范围广, 其中包括但不限于:

- Statistical Inference 统计推断

- Statistical Computing 统计计算

- Advanced Probability Theory 高等概率论

- Advanced Mathematical Statistics 高等数理统计学

- (Generalized) Linear Models 广义线性模型

- Statistical Machine Learning 统计机器学习

- Longitudinal Data Analysis 纵向数据分析

- Foundations of Data Science 数据科学基础

统计代写|金融统计代写financial statistics代考|The Augmented Dickey–Fuller test

It is well known in the unit root literature that the limit distribution of the ADF statistic depends on both the null hypothesis and the precise regression model specification. ${ }^{c}$ Appropriate choices of both therefore have a material impact in practical implementation.

The null hypothesis $\left(H_{0}\right)$ of the PSY test captures normal market behaviors and states that asset prices follow a martingale process with a mild drift function such that (Phillips et al., 2014)

$$

y_{t}=g_{T}+y_{t-1}+u_{t},

$$

where $g_{T}=k T^{-\gamma}$ (with constant $k, \gamma>1 / 2$, and sample size $T$ ) captures any mild drift that may be present in prices but which is of smaller order than the martingale component and is therefore asymptotically negligible.

The regression model chosen for the PSY procedure is

$$

\Delta y_{t}=\mu+\rho y_{t-1}+\sum_{j=1}^{p} \phi_{j} \Delta y_{t-j}+v_{t},

$$

where for implementation purposes the regression error $v_{t}$ is assumed to satisfy $v_{t}^{i . i . d} \sim\left(0, \sigma^{2}\right)$. The $p$ lag terms of $\Delta y_{t}$ are included to take care of potential serial correlation. The lag order $p$ is often selected by information criteria. The regression model includes an intercept but no time trend and nests the null hypothesis as a special case with $\mu=g_{T}$ and $\rho=0$. The ADF statistic is simply the $t$-ratio of the least squares estimate of the coefficient $\rho$.

The i.i.d error condition may be replaced with a martingale difference sequence (mds) condition in (2). More general specifications on the error $u_{t}$ in the generating mechanism (1), such as those in Assumption 1 below, may be employed and are accommodated by allowing the regression lag order $p \rightarrow \infty$ as $T \rightarrow \infty$ in (2). Nonparametric adjustments for serial correlation may also be used, such as those developed in Phillips (1987) and Phillips and Perron (1988).

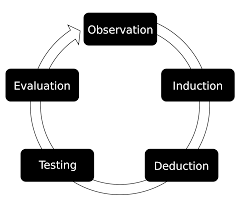

统计代写|金融统计代写financial statistics代考|The Recursive Evolving Algorithm

The recursive evolving algorithm of PSY enables real-time identification of bubbles and crises while allowing for the presence of multiple structural breaks within the sample period. Phillips et al. (2015a,b) show that this algorithm is superior to the forward expanding and rolling window algorithms in bubble identification, especially when the sample period contains multiple bubbles.

For the convenience of exposition, we use the standard “fraction of the total sample” notation for observations. Thus if $t=\lfloor T r\rfloor$ is the integer part of $T r$, then observation $t$ is represented fractionally as observation $r$ and then the total sample runs over values of $r$ from 0 to 1 . Suppose the observation of interest is $r^{\dagger}$. The PSY procedure calculates the ADF statistic recursively from a backward expanding sample sequence. Let $r_{1}$ and $r_{2}$ be the start and end points of the regression sample. The ADF statistic calculated from this sample is denoted by $A D F_{r_{1}}^{r_{2}}$. We fix the end point of all samples on the observation of interest such that $r_{2}=r^{\dagger}$ and allow the start point $r_{1}$ to vary within its feasible range, i.e., $\left[0, r^{\dagger}-r_{0}\right]$, where $r_{0}$ is the minimum window required to initiate the regression. The recommended setting of $r_{0}$ for practical implementation is $r_{0}=0.01$ $+1.8 / \sqrt{T}$. The PSY statistic is the supremum taken over the values of all the ADF statistics in the entire recursion, which is represented mathematically as

$$

P S Y_{r^{\dagger}}\left(r_{0}\right)=\sup {r{1} \in\left[0, r^{\dagger}-r_{0}\right], r_{2}=r^{\dagger}}\left{A D F_{r_{1}}^{r_{2}}\right} .

$$

The supremum enables the selection of the “optimal” starting point of the regression in the sense of providing the largest ADF statistic.

The PSY test can be conducted for each individual observation of interest ranging from $r_{0}$ to 1 , i.e., for $r^{\dagger} \in\left[r_{0}, 1\right]$. The recursive calculation evolves as the observation of interest moves forward and therefore the procedure is called a recursive evolving algorithm. See Fig. 1 for a graphical illustration of the algorithm. The corresponding PSY statistic sequence is $\left{P S Y_{r^{+}}(r 0)\right}_{r^{*} \in[r 0,1]}$.

统计代写|金融统计代写financial statistics代考|The Rationale

To illustrate the idea of bubble identification, consider the present value asset price formula

$$

P_{t}=\sum_{i=0}^{\infty}\left(\frac{1}{1+r_{f}}\right)^{i} \mathbb{E}{t}\left(D{t+i}\right)+B_{t},

$$

where $P_{t}$ is the price of the asset, $D_{t}$ is the payoff received from the asset, $r_{f}$ is the risk-free interest rate, $\mathbb{E}{t}(\cdot)$ is the conditional expectation operator given information to time $t$, and $B{t}$ is the bubble component. The bubble component satisfies the submartingale property (Diba and Grossman, 1988)

$$

\mathbb{E}{t}\left(B{t+1}\right)=\left(1+r_{f}\right) B_{t} .

$$

In the absence of a bubble, the degree of nonstationarity of the asset price is controlled entirely by the dividend series and hence is believed from empirical evidence to be at most $I(1)$. On the other hand, asset prices will be explosive in the presence of a bubble component in formula (7) whenever the initialization $B_{0}>0$ in (8).

Asset price dynamics over the expansionary phase of a bubble period may be modeled in terms of a mildly explosive process (Phillips et al., 2011; Phillips and Magdalinos, 2007; Phillips and Yu, 2009) of the form

$$

\log P_{t}=\delta_{T} \log P_{t-1}+u_{t},

$$

where the autoregressive coefficient $\delta_{T}=1+c T^{-\eta}$ mildly exceeds unity (with $c>0$ and $\eta \in(0,1))$ and yet still lies in its general vicinity. Detection of a bubble process in the data is therefore equivalent to distinguishing a martingale process of asset prices from a mildly explosive process. This can be achieved by the PSY procedure with null and alternative hypotheses specified as

$$

\begin{aligned}

&H_{0}: \mu=g_{T} \text { and } \rho=0, \

&H_{A}: \mu=0 \text { and } \rho>0 .

\end{aligned}

$$

金融统计代写

统计代写|金融统计代写financial statistics代考|The Augmented Dickey–Fuller test

在单位根文献中众所周知,ADF 统计量的极限分布取决于原假设和精确的回归模型规范。CAppropriate choices of both therefore have a material impact in practical implementation.

零假设(H0)的 PSY 测试捕捉正常的市场行为,并指出资产价格遵循具有温和漂移函数的鞅过程,这样 (Phillips et al., 2014)

是吨=G吨+是吨−1+在吨,

在哪里G吨=ķ吨−C(与常数ķ,C>1/2, 和样本量吨) 捕捉价格中可能存在的任何轻微漂移,但其阶次小于鞅分量,因此渐近可忽略不计。

为 PSY 程序选择的回归模型是

Δ是吨=μ+ρ是吨−1+∑j=1pφjΔ是吨−j+在吨,

出于实施目的,回归误差在哪里在吨假设满足在吨一世.一世.d∼(0,σ2). 这p滞后项Δ是吨包括在内以处理潜在的序列相关性。滞后顺序p通常是由信息标准选择的。回归模型包括截距但没有时间趋势,并将原假设嵌套为特殊情况μ=G吨和ρ=0. ADF 统计量就是吨- 系数的最小二乘估计的比率ρ.

iid 错误条件可以替换为 (2) 中的鞅差序列 (mds) 条件。有关错误的更一般规范在吨在生成机制 (1) 中,例如下面的假设 1 中的那些,可以通过允许回归滞后顺序来使用和适应p→∞作为吨→∞在 (2) 中。也可以使用序列相关的非参数调整,例如 Phillips (1987) 和 Phillips and Perron (1988) 开发的那些。

统计代写|金融统计代写financial statistics代考|The Recursive Evolving Algorithm

PSY 的递归演化算法能够实时识别泡沫和危机,同时允许在样本期间存在多个结构中断。菲利普斯等人。(2015a,b)表明该算法在气泡识别方面优于前向扩展和滚动窗口算法,尤其是在样本周期包含多个气泡时。

为方便说明,我们使用标准的“总样本分数”表示法进行观察。因此,如果吨=⌊吨r⌋是整数部分吨r, 然后观察吨分数表示为观察r然后总样本超过r从 0 到 1 。假设感兴趣的观察是r†. PSY 过程从向后扩展的样本序列递归地计算 ADF 统计量。让r1和r2是回归样本的起点和终点。从该样本计算的 ADF 统计量表示为一种DFr1r2. 我们将所有样本的终点固定在感兴趣的观察上,使得r2=r†并允许起点r1在其可行范围内变化,即[0,r†−r0], 在哪里r0是启动回归所需的最小窗口。推荐的设置r0实际实施是r0=0.01 +1.8/吨. PSY统计量是整个递归过程中所有ADF统计量取值的上确界,数学上表示为

P S Y_{r^{\dagger}}\left(r_{0}\right)=\sup {r{1} \in\left[0, r^{\dagger}-r_{0}\right], r_{2}=r^{\dagger}}\left{A D F_{r_{1}}^{r_{2}}\right} 。P S Y_{r^{\dagger}}\left(r_{0}\right)=\sup {r{1} \in\left[0, r^{\dagger}-r_{0}\right], r_{2}=r^{\dagger}}\left{A D F_{r_{1}}^{r_{2}}\right} 。

在提供最大 ADF 统计量的意义上,上确界能够选择回归的“最佳”起点。

PSY 测试可以针对每个感兴趣的观察进行,范围从r0为 1 ,即,对于r†∈[r0,1]. 递归计算随着感兴趣的观察向前移动而进化,因此该过程称为递归进化算法。有关该算法的图解说明,请参见图 1。对应的 PSY 统计序列为\left{P S Y_{r^{+}}(r 0)\right}_{r^{*} \in[r 0,1]}\left{P S Y_{r^{+}}(r 0)\right}_{r^{*} \in[r 0,1]}.

统计代写|金融统计代写financial statistics代考|The Rationale

为了说明泡沫识别的概念,考虑现值资产价格公式

磷吨=∑一世=0∞(11+rF)一世和吨(D吨+一世)+乙吨,

在哪里磷吨是资产的价格,D吨是从资产中获得的收益,rF是无风险利率,和吨(⋅)是给定时间信息的条件期望算子吨, 和乙吨是气泡成分。气泡成分满足亚鞅性质(Diba 和 Grossman,1988)

和吨(乙吨+1)=(1+rF)乙吨.

在没有泡沫的情况下,资产价格的非平稳程度完全由股利序列控制,因此根据经验证据认为最多为一世(1). 另一方面,每当初始化时,在公式(7)中存在泡沫成分的情况下,资产价格将是爆炸性的乙0>0在 (8) 中。

泡沫时期扩张阶段的资产价格动态可以用以下形式的温和爆炸过程来建模(Phillips 等,2011;Phillips 和 Magdalinos,2007;Phillips 和 Yu,2009)

日志磷吨=d吨日志磷吨−1+在吨,

其中自回归系数d吨=1+C吨−这稍微超过统一(与C>0和这∈(0,1))但仍位于其大体附近。因此,检测数据中的泡沫过程等同于区分资产价格的鞅过程和轻度爆炸过程。这可以通过 PSY 过程来实现,其中零假设和替代假设指定为

H0:μ=G吨 和 ρ=0, H一种:μ=0 和 ρ>0.

统计代写请认准statistics-lab™. statistics-lab™为您的留学生涯保驾护航。

金融工程代写

金融工程是使用数学技术来解决金融问题。金融工程使用计算机科学、统计学、经济学和应用数学领域的工具和知识来解决当前的金融问题,以及设计新的和创新的金融产品。

非参数统计代写

非参数统计指的是一种统计方法,其中不假设数据来自于由少数参数决定的规定模型;这种模型的例子包括正态分布模型和线性回归模型。

广义线性模型代考

广义线性模型(GLM)归属统计学领域,是一种应用灵活的线性回归模型。该模型允许因变量的偏差分布有除了正态分布之外的其它分布。

术语 广义线性模型(GLM)通常是指给定连续和/或分类预测因素的连续响应变量的常规线性回归模型。它包括多元线性回归,以及方差分析和方差分析(仅含固定效应)。

有限元方法代写

有限元方法(FEM)是一种流行的方法,用于数值解决工程和数学建模中出现的微分方程。典型的问题领域包括结构分析、传热、流体流动、质量运输和电磁势等传统领域。

有限元是一种通用的数值方法,用于解决两个或三个空间变量的偏微分方程(即一些边界值问题)。为了解决一个问题,有限元将一个大系统细分为更小、更简单的部分,称为有限元。这是通过在空间维度上的特定空间离散化来实现的,它是通过构建对象的网格来实现的:用于求解的数值域,它有有限数量的点。边界值问题的有限元方法表述最终导致一个代数方程组。该方法在域上对未知函数进行逼近。[1] 然后将模拟这些有限元的简单方程组合成一个更大的方程系统,以模拟整个问题。然后,有限元通过变化微积分使相关的误差函数最小化来逼近一个解决方案。

tatistics-lab作为专业的留学生服务机构,多年来已为美国、英国、加拿大、澳洲等留学热门地的学生提供专业的学术服务,包括但不限于Essay代写,Assignment代写,Dissertation代写,Report代写,小组作业代写,Proposal代写,Paper代写,Presentation代写,计算机作业代写,论文修改和润色,网课代做,exam代考等等。写作范围涵盖高中,本科,研究生等海外留学全阶段,辐射金融,经济学,会计学,审计学,管理学等全球99%专业科目。写作团队既有专业英语母语作者,也有海外名校硕博留学生,每位写作老师都拥有过硬的语言能力,专业的学科背景和学术写作经验。我们承诺100%原创,100%专业,100%准时,100%满意。

随机分析代写

随机微积分是数学的一个分支,对随机过程进行操作。它允许为随机过程的积分定义一个关于随机过程的一致的积分理论。这个领域是由日本数学家伊藤清在第二次世界大战期间创建并开始的。

时间序列分析代写

随机过程,是依赖于参数的一组随机变量的全体,参数通常是时间。 随机变量是随机现象的数量表现,其时间序列是一组按照时间发生先后顺序进行排列的数据点序列。通常一组时间序列的时间间隔为一恒定值(如1秒,5分钟,12小时,7天,1年),因此时间序列可以作为离散时间数据进行分析处理。研究时间序列数据的意义在于现实中,往往需要研究某个事物其随时间发展变化的规律。这就需要通过研究该事物过去发展的历史记录,以得到其自身发展的规律。

回归分析代写

多元回归分析渐进(Multiple Regression Analysis Asymptotics)属于计量经济学领域,主要是一种数学上的统计分析方法,可以分析复杂情况下各影响因素的数学关系,在自然科学、社会和经济学等多个领域内应用广泛。

MATLAB代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。

![4. Machine Learning-Based Volatility Prediction - Machine Learning for Financial Risk Management with Python [Book]](data:image/svg+xml,%3Csvg%20xmlns='http://www.w3.org/2000/svg'%20viewBox='0%200%20539%20338'%3E%3C/svg%3E)